TSLombard with the note.

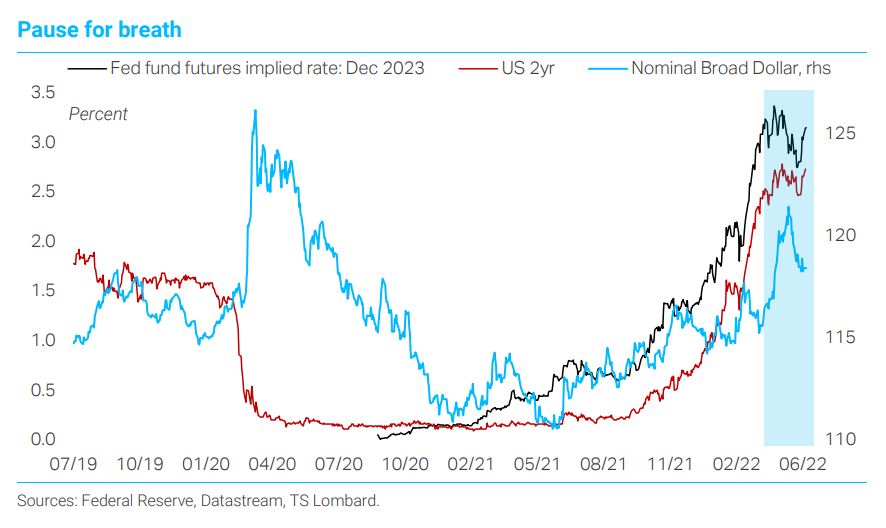

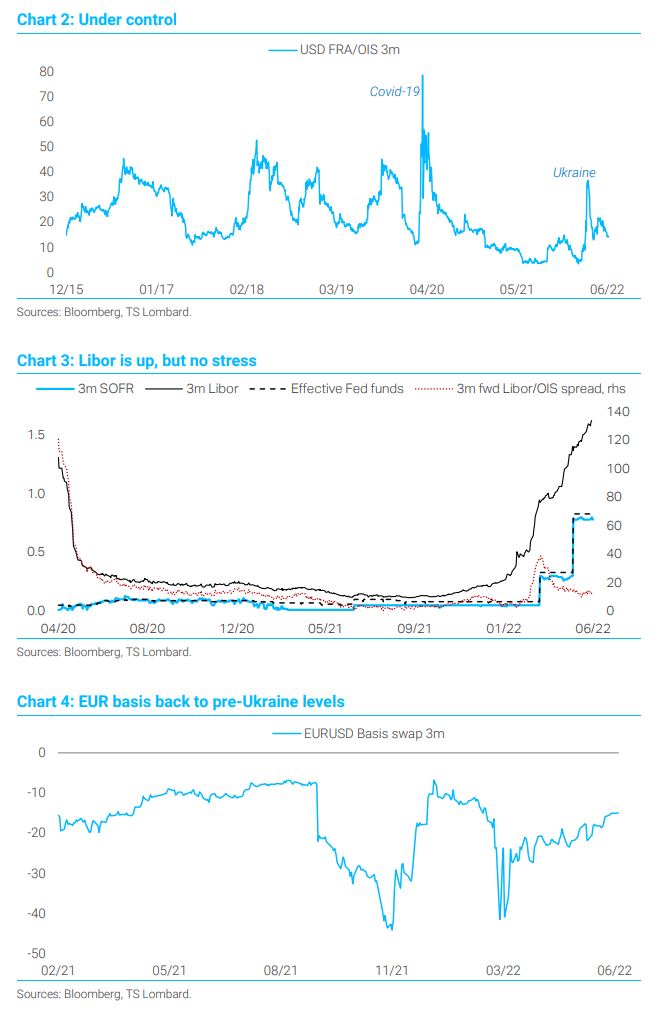

Indicators of market funding stress jumped in response to Russia’s invasion of Ukraine in late February. But they soon retraced back to more normal levels, underscoring the view that central banks have learned from past crises and are prepared to step in without delay to address dislocations in market liquidity. Metrics of perceived risk in the interbank lending market, such as Libor/OIS and FRA/OIS (forward vs overnight indexed swap rate) spreads seem to suggest little cause for concern at this stage (charts 2 & 3). Libor has moved higher with the OIS curve, although its widening spread versus SOFR (which measures the cost of borrowing cash overnight collateralized by Treasury securities) could be interpreted as a sign of growing scarcity in safe collateral – something that is effectively keeping a lid on secured rates (chart 3). Further, the EUR/USD cross currency basis (i.e., the premium embedded in FX swaps) has reverted to pre-Ukraine levels (chart 4). Perhaps the more important development over the last year or so has been broad-based strength in the dollar, which bottomed out in 2021 Q2 and has trended higher since. The pace of appreciation accelerated during spring 2022 in tandem with a hawkish recalibration of market expectations for Fed policy. Following May’s FOMC meeting, these expectations have cooled somewhat and shortterm Treasury yields have rolled over, pulling USD lower (chart 1). Yet this still leaves the dollar exchange rate versus the major DM currencies close to its Covid high set in March 2020.

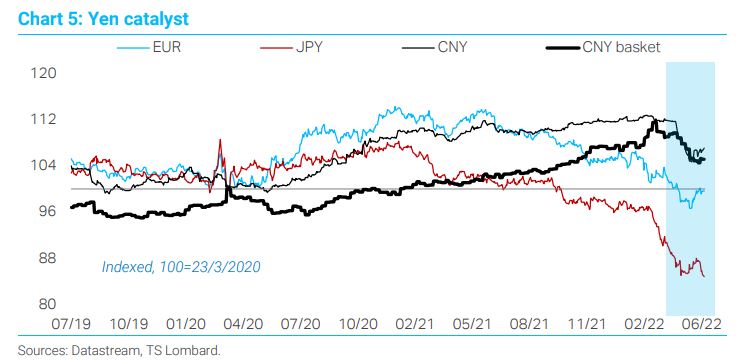

The Japanese yen stands out, down around 13% since March and a fifth weaker versus the dollar since January 2021. Pronounced JPY weakness – the mirror image of the rapid advance in US Treasury yields – arguably acted as a catalyst for the PBoC’s decision to let CNY slide against a backdrop of decelerating Chinese economic activity (chart 5).