Mortgage grenade to detonate Aussie recession

As we know, the the Reserve Bank of Australia (RBA) is forecast to aggressively lift interest rates over the coming year. The median economists’ forecast is for the OCR to peak at around 2.5%, which corresponds to RBA governor Phil Lowe’s recent correspondence that he expects to lift the target cash rate to at least 2.5%.

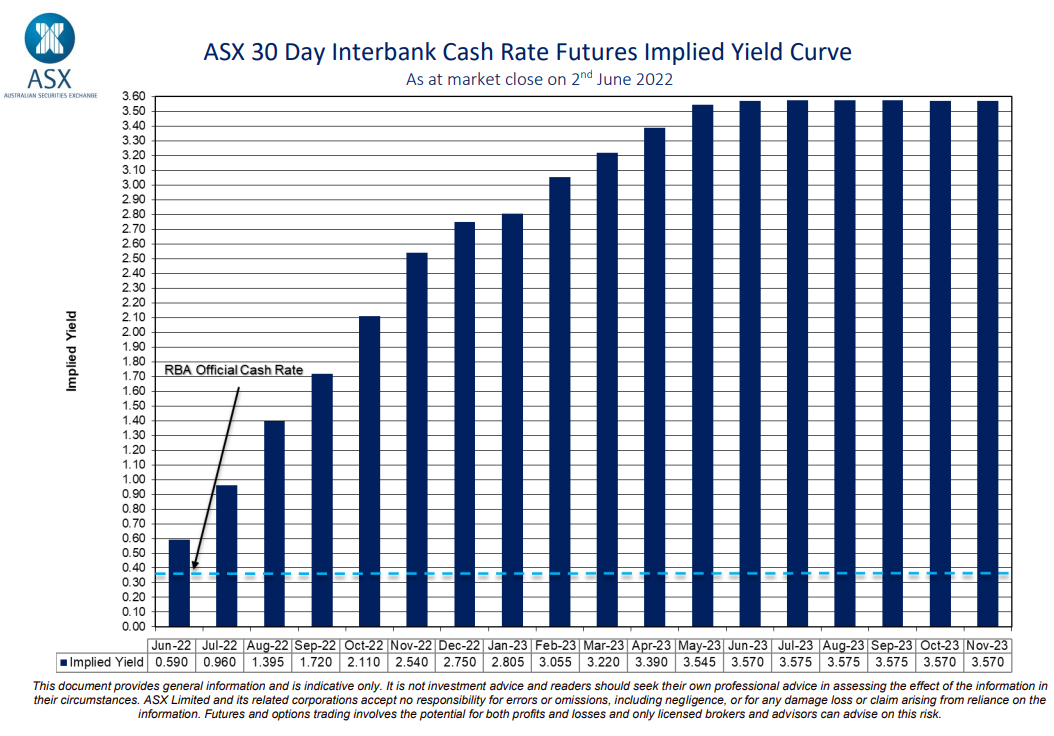

The futures market is even more hawkish, tipping the RBA will lift the OCR to around 3.5 per cent by May 2023:

Forecast interest rate rises would crash household consumption:

Assuming the economists’ or market’s OCR forecasts were fully passed-on to mortgage holders, the average discount variable mortgage rate would soar from its current level of 3.70% to between 5.85% and 6.85% by mid-2023.

This would represent the sharpest proportional increase in mortgage rates in Australia’s history and would devastate household finances, the housing market, and the Australian economy.

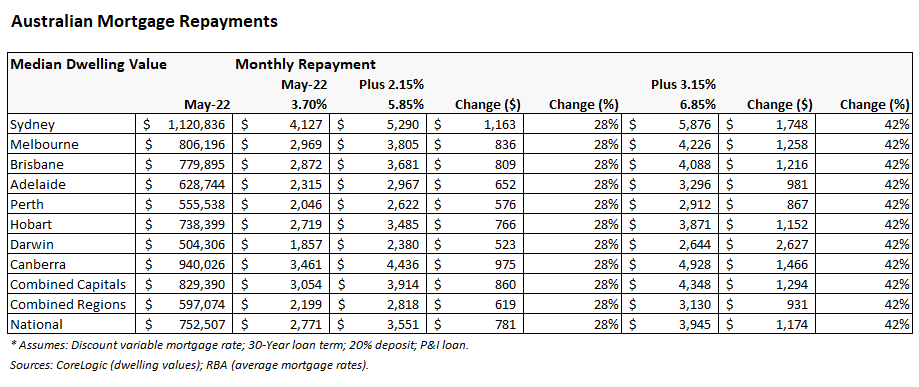

To illustrate why, consider the next table showing the average monthly repayment on the median priced dwelling across Australia, assuming a 30-year principal and interest variable rate mortgage and a 20% deposit:

If the economists’ forecast comes to fruition, and the OCR rises another 2.15% (to 2.5%), then the average monthly mortgage repayment on the median priced Australian home would rise by $781, or 28%. The impact would be greatest in Sydney, where monthly mortgage repayments would jump by $1,163.

If the futures market’s forecast comes true, and the OCR rises another 3.15% (to 3.5%), then the average monthly mortgage repayment on the median priced Australian home would soar by $1,174 (42%), with repayments across Sydney ballooning by $1,748 a month.

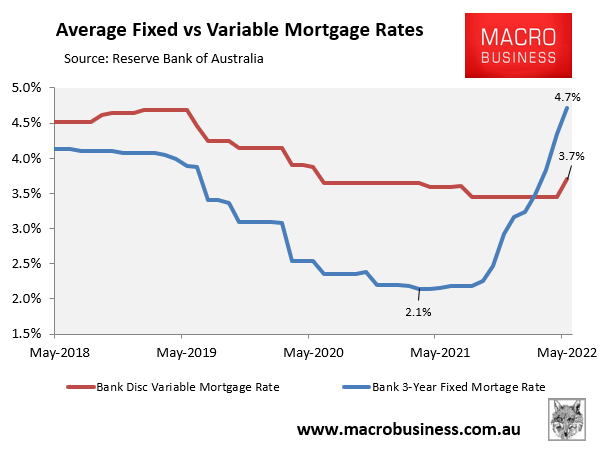

The impact would be even more severe for borrowers that took out a fixed rate mortgage during the height of the pandemic at rock bottom rates below 2.5%.

Under the economists’ OCR forecast, these fixed rate borrowers would face more than a doubling of mortgage rates when it comes to refinance in 2023 and 2024, whereas mortgage rates would triple under the market’s OCR forecast.

With around $500 billion worth of fixed rate mortgage terms due to expire by the end of 2023, thousands of Australian households face the prospect of a devastating mortgage reset shock.

The Australian economy would be thrown into recession:

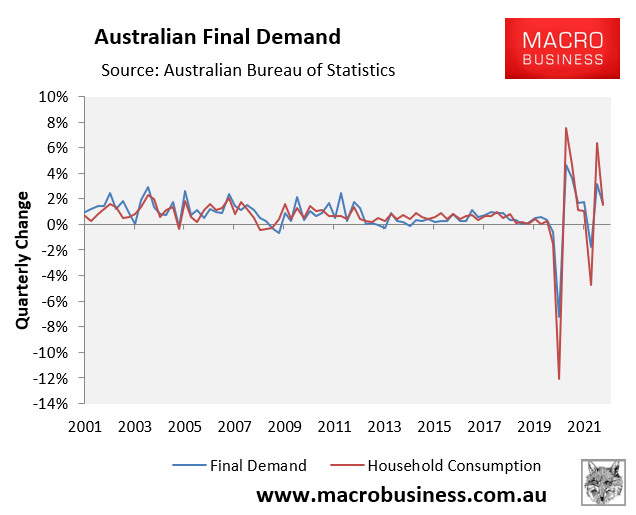

Household consumption is by far the biggest driver of the nation’s economic growth, accounting for around 55% of final demand in a typical quarter. Therefore, where household consumption goes, the economy usually follows:

So, if mortgage repayments rise too sharply, this will mean there are less funds available for spending across the economy, in turn crunching economic growth.

The negative drag on household consumption would also be exacerbated by a sharp fall in house prices, which would make Australians feel poorer.

The bottom line is that RBA must tread very carefully on interest rates. If it tightens as much as forecast, then it risks crashing household consumption, house prices, and the economy.