Wall Street pushed ahead of cautious European stocks overnight, possibly caused by a lower than expected German factory orders print. The USD edged slightly lower against almost everything, but it was all relative as Euro remains relatively depressed while the post RBA rate hike is still keeping the Australian dollar around the 72 cent level. Interest rate and bond markets were fairly unchanged with some roundtripping on 10 year Treasury yields which reverted back below the 3% level again. Commodity prices were also mixed with oil prices remaining at a monthly high, Brent crude sitting just above the $120USD per barrel level while gold got back above the $1850USD per ounce level, but only just.

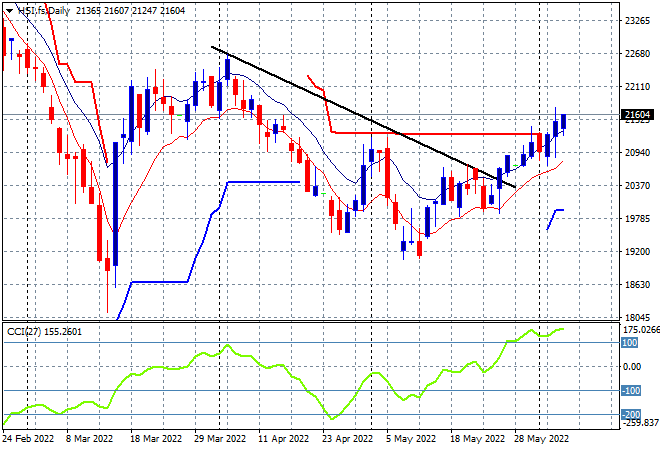

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets basically put in scratch sessions with the Shanghai Composite closing up a handful of points to finish 0.2% higher at 3241 while the Hang Seng Index gave back more than 0.6% to finish down at the 21531 point level. The daily chart is showing price now breaking above trailing daily ATR resistance at the 21000 point level possibly moving towards a more sustainable trend. Daily momentum is still overbought with price action translating into greater highs with the March highs near the 23000 point level the next target:

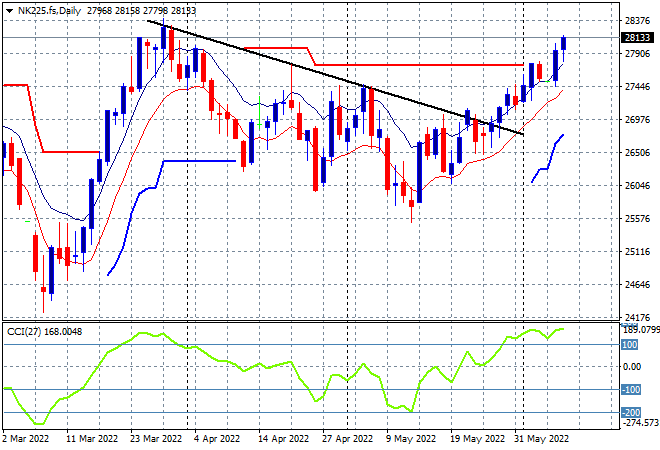

Meanwhile Japanese stock markets are also in wait and see mode, with the Nikkei 225 index closing just 0.1% higher at 27943 points. The daily chart of the Nikkei 225 is showing a strong move now to get back above the previous daily/weekly highs, with the March highs almost in sight. Daily momentum is nicely overbought as a much weaker Yen helps lifts all boats here: