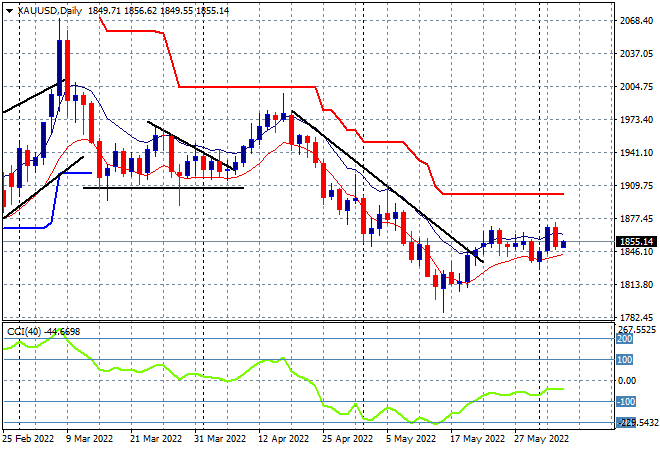

Asian share markets have started the trading week in robust fashion, except for local shares which are already pricing in a rate rise by the RBA tomorrow, plus the ongoing energy crisis. This bounceback from the firmer than expected US non-farm payrolls print from Friday night has seen a small bounce against the resurgent USD with both Euro and Pound Sterling lifting as we head into the London session. Oil prices are holding steady after their big lift on Friday, with Brent crude still hovering above the $120USD per barrel level while gold is trying to stabilise as it remains stuck near the $1850USD per ounce level:

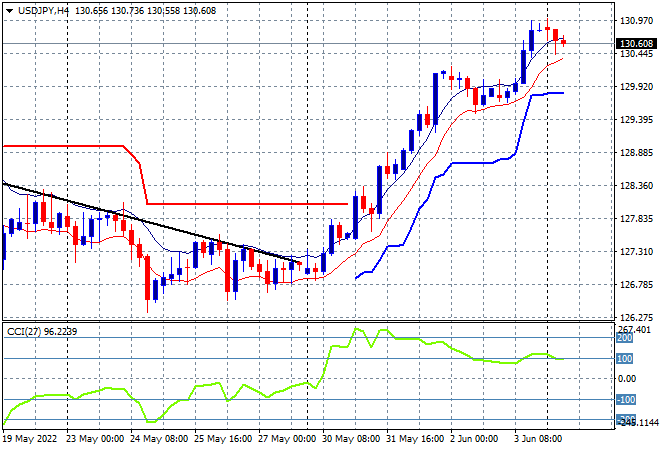

Mainland and other Chinese share markets reopened today with the Shanghai Composite lifting 1.3% to 3236 points while the Hang Seng Index gained nearly 1.7% to finish at 21439 points. Meanwhile Japanese stock markets were also able to lift higher on the back of a weak Yen, with the Nikkei 225 index closing 0.6% higher at 27915 points while the USDJPY pair has held on to its own outsize gains from Friday night, sitting at the 130.60 level:

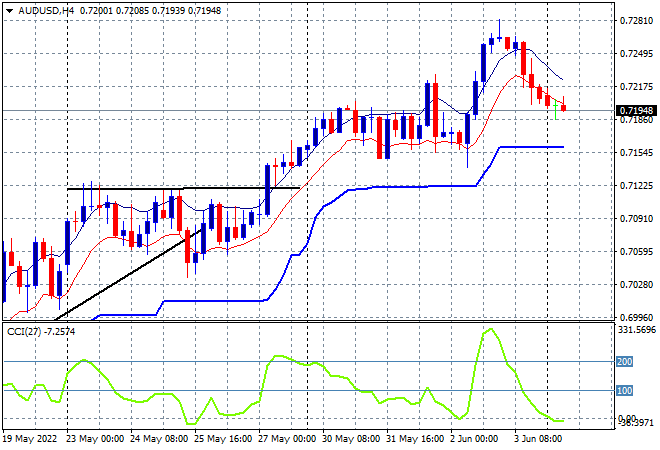

Australian stocks were the odd ones out with the ASX200 losing 0.6% to start the week at 7206 points while the Australian dollar continued the mild dip from Friday night to retrace back below the 72 level against USD but holding on to its weekly uptrend:

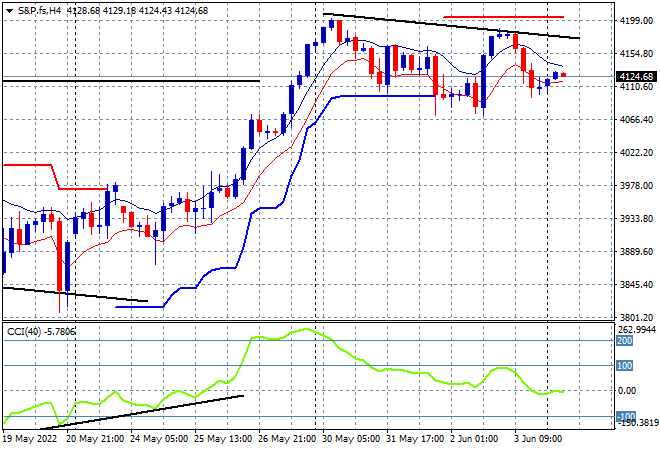

Eurostoxx and Wall Street futures are lifting slightly as we head into the European open with the S&P500 four hourly futures chart showing price still holding on above key support at the 4100 point level. Short term momentum is neutral at best and is showing nascent signs of a rollover so watch out below:

The economic calendar starts the week slowly, with some short term Treasury auctions but not much else.