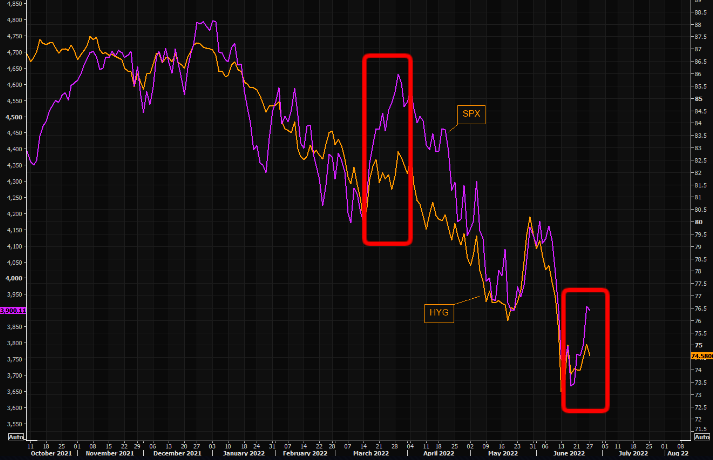

Just another bear market rally. The Market Ear with the note.

—

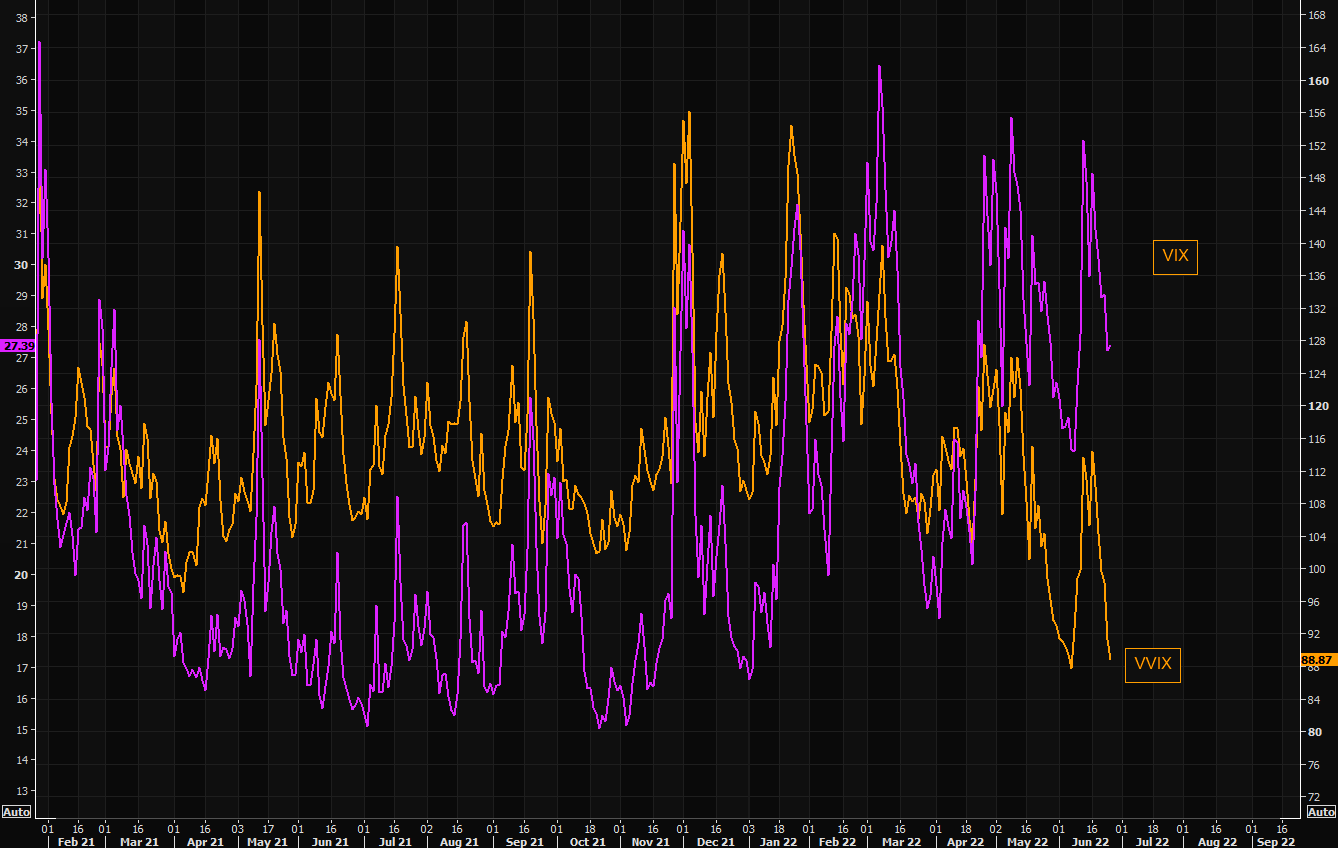

| VVIX – inverse panic |

| Believe it or not but VVIX is pretty much back to recent lows, currently printing 88.88….VIX is down over past sessions, but the gap vs VVIX remains huge. Low VVIX does not mean the VIX must collapse as the low skew affects VVIX a lot. Nevertheless it is worth noting: stress is fading further… |

Refinitiv Refinitiv |

| Put frustration |

| Nothing really new, but the crowd managed “loving” puts as the market made a local low. Most people tend to buy protection when they must, and not when they can. This results in hedges losing value quickly, feeding the loop of “who needs protection bro…it only costs money”. |

Tradingview Tradingview |

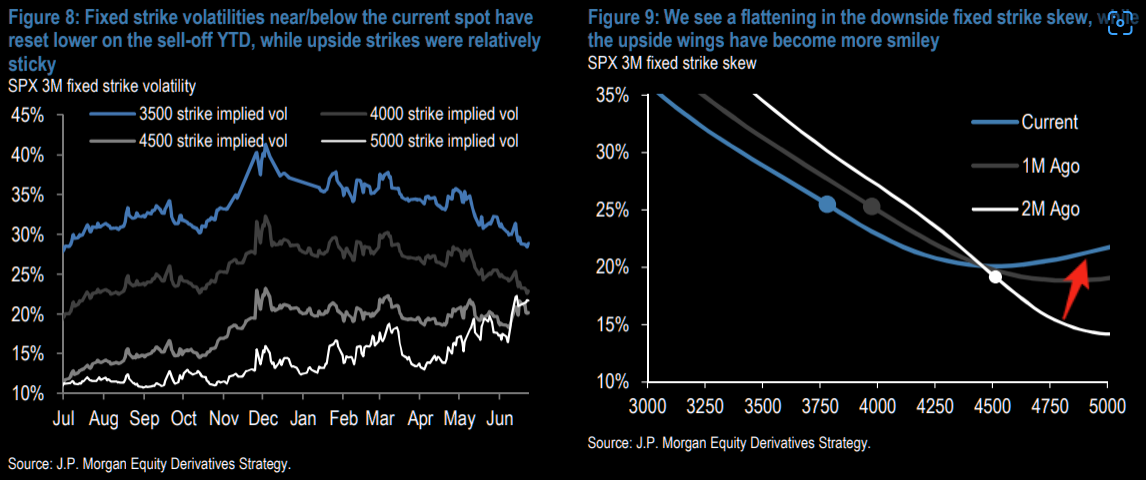

| What risks are options markets showing? |

| By now even the people that don’t trade volatility should be aware of the fact skew has collapsed. JPM shows how skew has flattened, while upside has seen a bid, shifting the curve into a more smiley look. What are the implications and how can you use this? Overwriting longs and using the premium to buy downside protection is relatively cheaper now than in a long time. |

JPM JPM |

| The latest from MS Chief US Equity Strategist, Mike Wilson | |||

| Winning or worried….? “In our view, both the fall in oil and rates are being driven more by the fears of an economic slowdown rather than a real peak in inflation and, therefore, peak Fed hawkishness…we continue to believe any near term rally is nothing more than a bear market bounce with lower lows ahead. …all of the move last week was due to valuations moving higher which seems unusual given the growing concern about earnings. In fact, even taking into account the fall in 10-year yields, the Equity Risk Premium is back to 300bps. In our view, that makes little sense in the context of the likely negative earnings revisions coming in 2Q and still rising risk of recession over the next 6-12 months. As our fair value valuation framework shows, the S&P 500 is now meaningfully mis-priced again for the current PMI and rates backdrop (even with the recent fall in bond yields). …The only question is whether we have a soft landing (base case) in which the S&P 500 bottoms near 3400-3500 or we have a recession (bear case) in which the index falls toward 3000.” (Morgan Stanley Equity strategy)

|