Former Reserve Bank of Australia (RBA) governor, Ian Macfarlane, has warned that inflation is unlikely to return to the RBA’s target range of 2% to 3%. He says the inflation rate could potentially peak at around 7% to 8% before eventually settling at around 5%.

Macfarlane adds that further increases in the cash rate are inevitable, and says it could rise above 4%:

“I find it hard to think that it [inflation] will just come back to 2 per cent. I think there’s enough scarcity out there, particularly with such a tight labour market both in the US and here, and with the feeding through of all the supply shocks… I think 3-4-5 per cent is more likely. It could go up to 7 or 8 per cent,” Mr Macfarlane told the Morgan Stanley Australia summit on Wednesday.

“[Interest rates] are obviously going to have to go up a lot more from where they are now. Everyone accepts that.

“The market is expecting… the cash rate to be 3.05 per cent by December… that’s a lot in a short period of time. It could happen. The other way of looking at it is that wherever inflation settles, you want the cash rate to be higher in real terms. If it were to settle at 4 per cent, you’d want it to be higher than 4 per cent.”

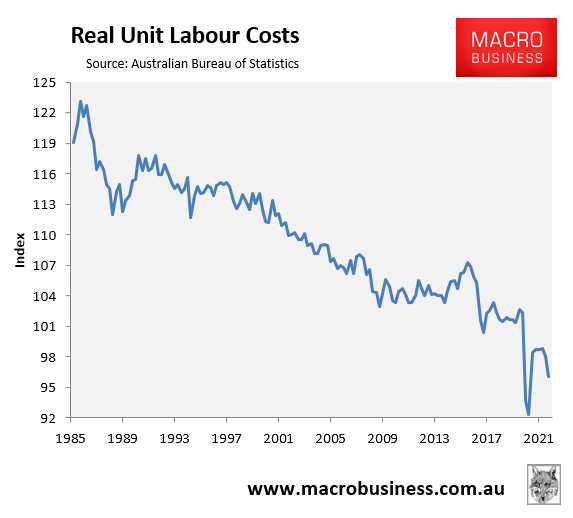

Australia’s inflation is primarily imported (e.g. petrol prices) or weather-related (e.g. $12 lettuces after floods). Hiking interest rates will do nothing to solve these supply shocks, especially given the broadest domestically-driven cause of inflation – wage costs – are hovering near record lows:

Second, in the absence of a wage-price spiral, the only way that inflation can remain stubbornly high (rather than transitory) is if the supply shocks continue to worsen, driving prices ever higher. For example, even if petrol were to remain at $2 a litre, this would not drive further inflation, since the Consumer Price Index (CPI) measures price changes quarter-on-quarter. The inflation would have already been captured in the CPI.

While prices would settle at a higher absolute level, inflation would fall back into target. The price change would effectively be ‘one-off’ – similar to when the GST was introduced in 2000.

Finally, an official cash rate of 4% would imply an average discount variable mortgage rate of around 7.4% – more than double the pandemic low. Average principal and interest mortgage repayments would soar by around 50%, throwing many households into extreme financial stress. Household consumption would collapse, house prices would crash, and the economy would be thrown into a deep recession.

In short, Ian Macfarlane has badly misread the situation.