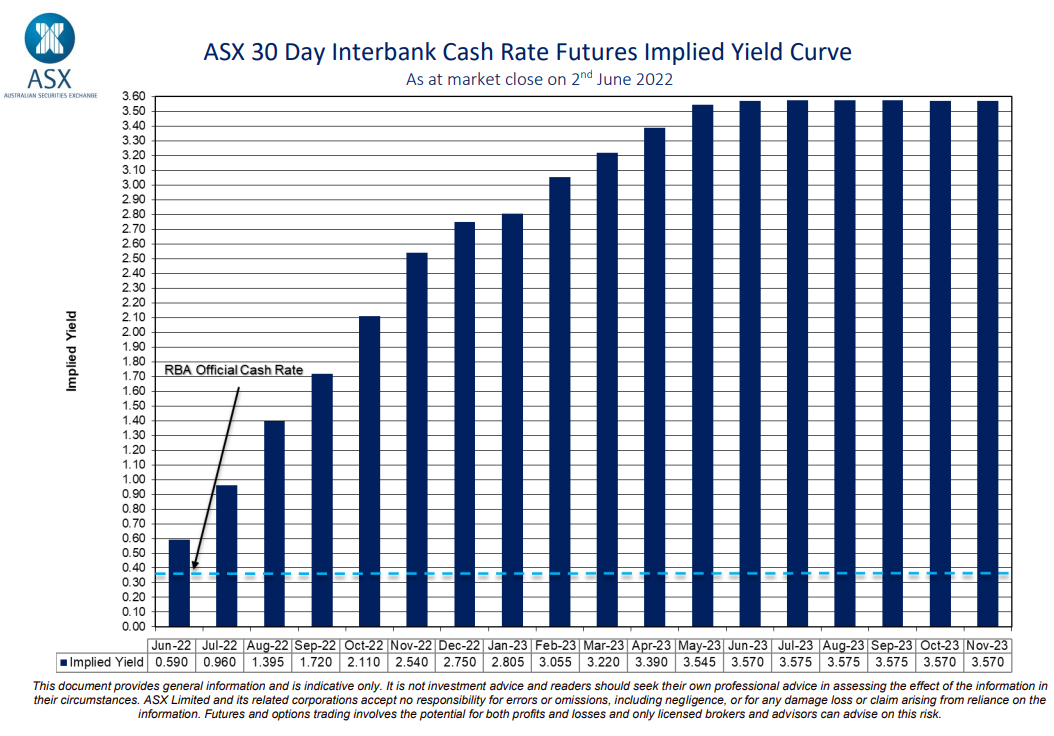

The delusional futures market continues to forecast apocalyptic rises in Australian interest rates.

As shown in the next chart, the market believes that the Official Cash Rate (OCR) will hit 2.75% by December and peak around 3.6% by June 2023:

Steepest rate rise in Australia’s history.

Australia’s economists have also become increasingly hawkish, ramping up their OCR projections:

Capital Economics is forecasting a 25 basis point rise next week, followed by 40 basis points in August, and a rate of 3 per cent by early-2023.

ANZ is one of two big-four banks tipping a 40 basis point increase next week, and is forecasting a cash rate path to about 2.5 per cent by mid-2023, before further rises to above 3 per cent after an assessment by the RBA…

Nomura Australia senior economist Andrew Ticehurst said he was “definitely” in the camp that believed the RBA would need to act faster…

Peter Tulip, chief economist at the Centre for Independent Studies… said the RBA should raise rates “aggressively”…

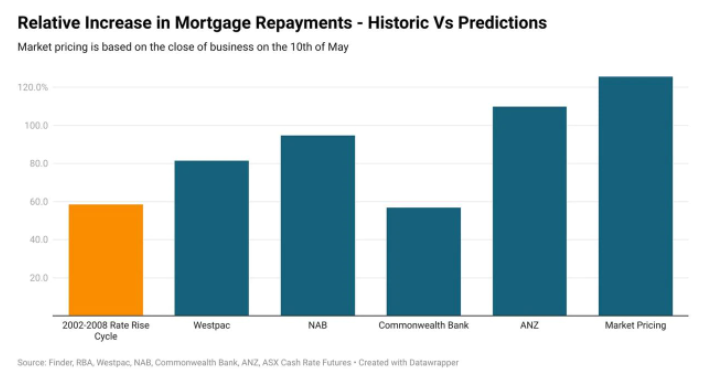

Last month, freelance journalist Tarric Brooker showed that mortgage interest payments would experience their biggest ever rise if the economists’ let alone the market’s OCR projection came to fruition.

Brooker’s analysis was based on the following OCR forecasts:

- CBA: Cash rate to peak at 1.6%

- Westpac: Cash rate to peak at 2.25%

- NAB: Cash rate to peak at 2.6%

- ANZ: Cash rate to peak at 3%

- Futures Market: Cash rate to peak at 3.56%

Every interest rate forecast other than the CBA’s would see Australian mortgage interest repayments rise by more than they did in 2002-2008, which currently holds the record for the steepest rise in repayments:

Most economists and the market forecast a record rise in mortgage interest repayments.

The CBA’s interest rate forecast is the only one grounded in reality. Australians are so indebted that households will struggle to cope with even a 1.6% rise in mortgage rates, let alone the magnitude of hikes projected by the other economists and the market.

The interest rate projections put forward by the median economist and market risk a full blown house price crash, a severe contraction in household consumption spending, and an unnecessary recession for the Australian economy. Are they mad?