By Gareth Aird, head of Australian economics at CBA:

Key Points:

- There has been a clear shift in tone and stance from the RBA Board and we now expect the RBA to front load rate hikes.

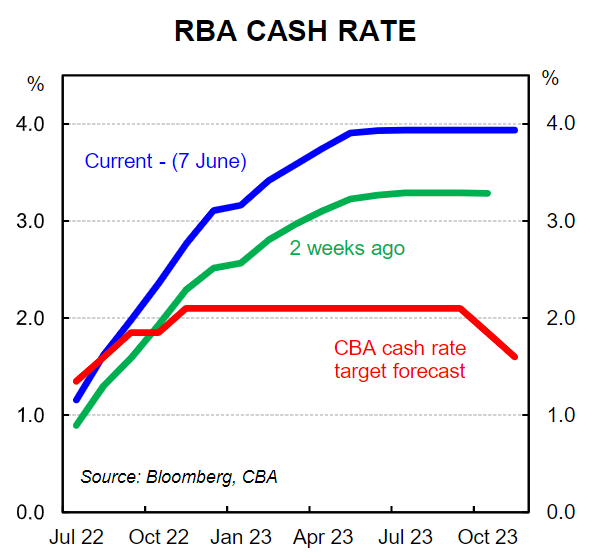

- The cash rate is forecast to reach 2.10% by end-2022 (the risk sits with a cash rate of 2.35%).

- A more aggressive tightening cycle, coupled with higher expected near term inflation has implications for our economic forecasts.

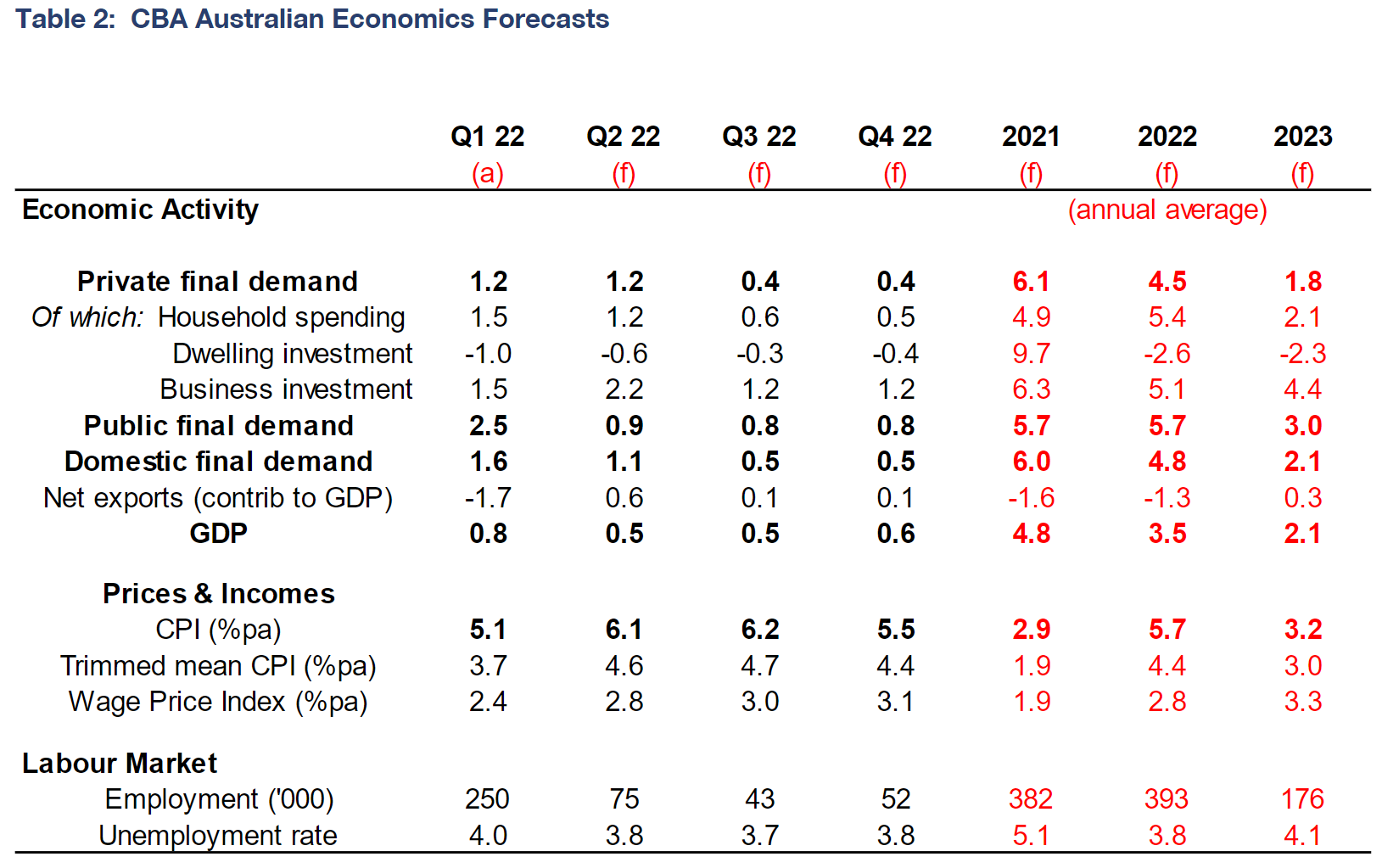

- We make a large downward revision to our GDP forecast to look for growth of 2.3%/yr at Q4 22 and 2.2%/yr at Q4 23.

- GDP growth is forecast to be 3.5% in 2022 (from 4.7% previously) and a below-trend 2.1% in 2023 (from 3.1% previously).

- Headline inflation is forecast to peak at 6¼% over 2022 and to decline to within the 2-3% target band by late 2023.

- The unemployment rate is forecast to stay at a very low 3¾% over 2022, but we anticipate the unemployment rate will edge higher over 2023 to 4½% given we expect below trend growth next year.

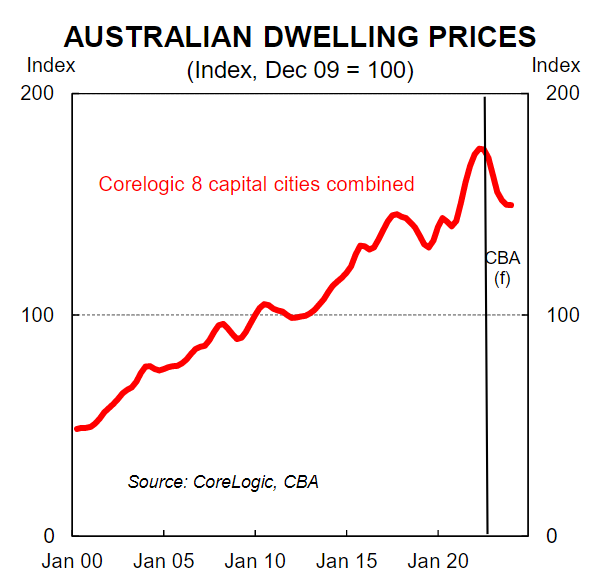

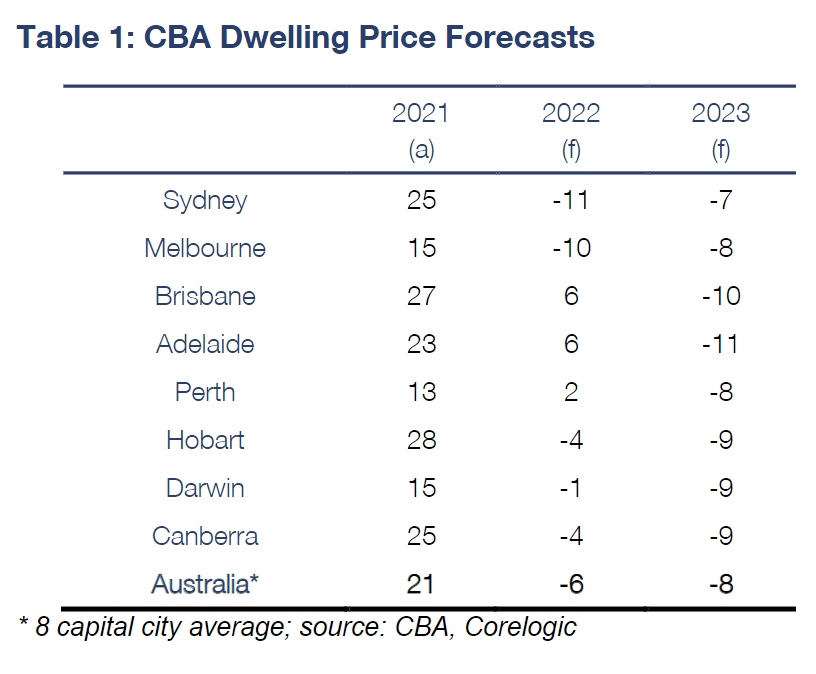

- National home prices are forecast to decline by ~15% by end-2023(peak to trough). Dwelling prices are anticipated to stabilise in late 2023.

- With the RBA now expected to take the cash rate to a contractionary setting we have pencilled in rate cuts for the second half of 2023.

- Fiscal policy still remains incredibly important to the outlook and is a key source of uncertainty.

Overview

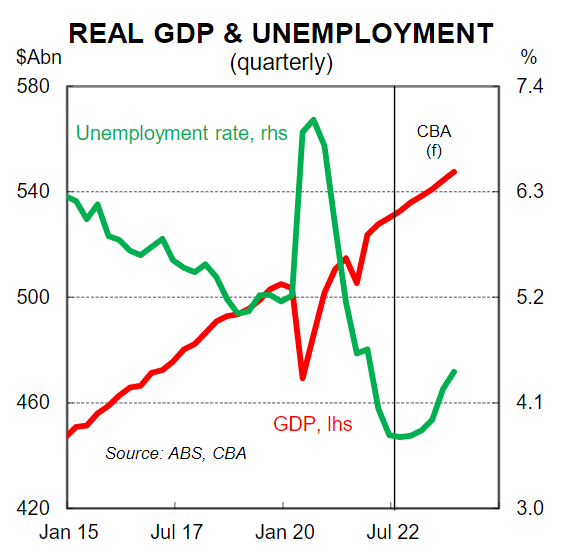

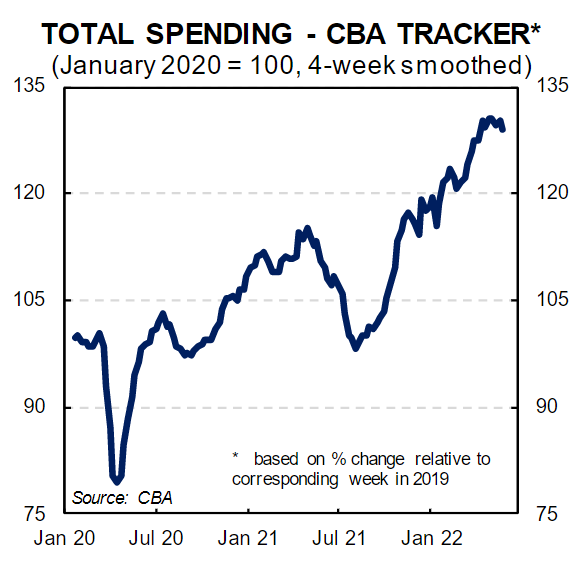

Economic booms cannot run indefinitely. But not all booms are followed by busts. Our expectation is that Australia’s current economic boom has a little further to run and the labour market will remain tight so we don’t foresee a bust. But growth momentum is anticipated to slow materially by late 2022 due to a swift and aggressive RBA tightening cycle. Deeply negative real wages growth will also weigh on the volume of spending over the rest of 2022.

A material slowdown in output is not the same thing as a contraction in production. As such, talk of a recession is premature. The household savings rate remains elevated so there is room for a decline in the savings rate to support consumption over the period ahead. However, we expect growth to moderate to a below-trend pace over 2023. This in turn will pull the current elevated rate of inflation down and we forecast that the unemployment rate will edge higher in late 2023.

The RBA looks very intent on dropping the inflation rate quickly. But this will come at the expense of growth in aggregate demand, particularly household consumption.

The RBA has their work cut out for them on the inflation front as there is very little they can do to run against global factors that have pushed inflation higher, particularly in the energy and food space. Nonetheless, the RBA this week has signalled their intention to normalise policy quickly by raising the cash rate by a larger than usual 50bp while noting that, “the Board is committed to doing what is necessary to ensure that inflation in Australia returns to target over time”.

Our central bank appears to now be first and foremost inflation fighters and their objective of “the economic prosperity and welfare of the people of Australia” has taken a back seat to their desire to drop the rate of inflation.

In this note we discuss our updated central scenario for the Australian economy in the context of our revised RBA call. We also cover our updated forecasts for dwelling prices. Our economic and dwelling price forecasts are very much conditional on the path of the RBA cash rate. Fiscal policy will also play a key role in shaping economic outcomes and is a key source of uncertainty.

The RBA in 2022

The RBA’s decision to raise the cash rate by a larger than usual 50bp at the June Board meeting indicates the Board has made the decision to front load the tightening cycle. As a result, we revised our forecast profile for the cash rate. We now expect a further 50bp rate hike in July followed by 25bp hikes in August, September and November that will see the cash rate target at 2.10% by the end of the 2022 (a level which we consider to be significantly contractionary). The risk is a higher year end cash rate of 2.35% which could occur with a hike of 50bp in August.

Our forecast profile for the cash rate is of course based on what we think the RBA will deliver and not what we believe the RBA should do.

The RBA is not facing a wage-price spiral like is being observed in some other jurisdictions. And we do not think the RBA has to run hard against wages growth by aggressively hiking the cash rate. Our previous profile for the cash rate to be gradually raised to 1.6% by February 2023reflected what we thought the RBA would deliver, which we also assessed to be the right policy path. But ultimately it does not matter what we think, it is about what they do.

Updated economic forecasts

Our revised profile for the cash rate coupled with an upward near term revision to our inflation forecasts means we have made a significant downward revision to our forecast for household consumption.

We now expect real consumer spending to be 3.9%/yr in Q4 22 (from 6.0%/yr previously) and 1.9%/yr in Q4 23 (from 2.7%/yr previously). The savings rate will fall to 7% by end-2023 on our updated forecasts for income and consumption.

The considerable downward revision to real consumer spending largely reflects the significant change in our RBA call. If our updated forecast profile for the cash rate is realised it will result in materially higher mortgage repayments for most households that have a home loan. This will weigh on spending. In addition, higher than anticipated energy prices will put downward pressure on real consumer spending, particularly discretionary consumption for lower income households.

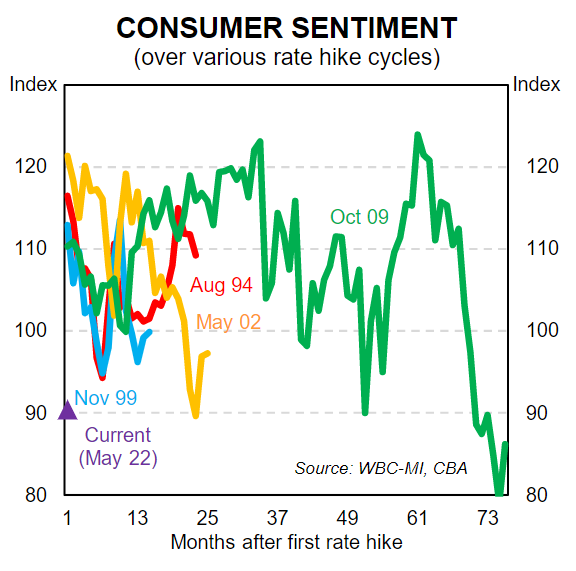

Consumer confidence is already in deeply pessimistic territory and we do not see that picture turning around anytime soon. Finally, a faster correction in the housing market will have a negative impact on spending via the wealth effect (more on home prices below). Turnover in the housing market will also slow which has a negative flow on effect to spending, particularly bigger ticket retail goods.

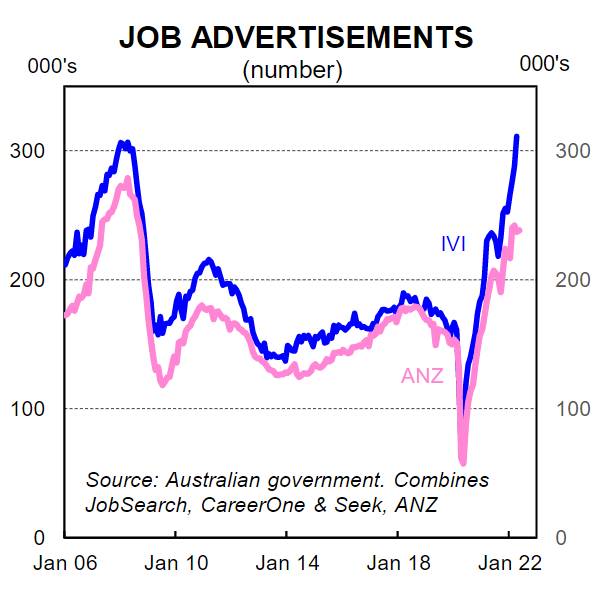

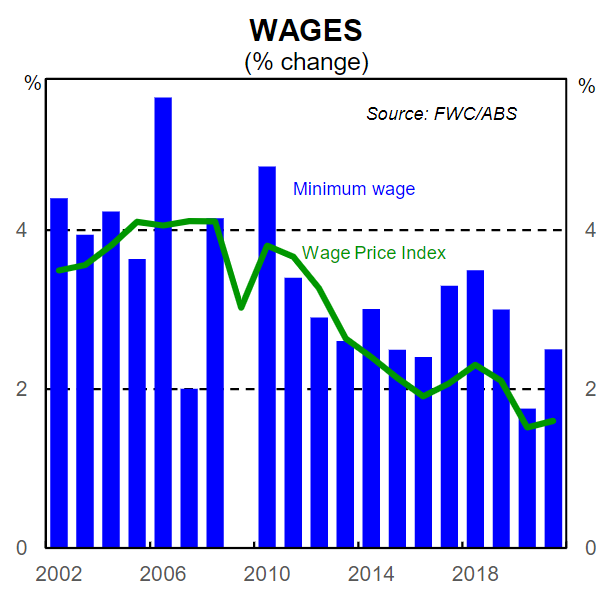

The news is not all one way, however. The labour market is very tight as best evidenced by the very low unemployment rate and the elevated level of job vacancies. Employment is a lagging indicator and the anticipated slowdown in consumer spending will take time to express itself in the labour market. As such, we retain our forecast for the unemployment rate to sit at ~3¾% over 2022. The low level of unemployment and underutilisation will help to drive higher pay rises for workers on individual agreements. In addition, the Fair Work Commission will hand down the annual wage review later this month where a significant lift in the award wage is expected compared with previous years. As a result, we expect wages growth, as measured by the wage price index, to rise to 3¼%/yr by early 2023.

Our large downward revision for real household consumption means we have made a significant revision to our forecast profile for GDP. We now forecast GDP growth to be 2.3%/yr at Q4 22 (from 4.3% previously) and 2.2%/yr at Q4 23 (from 2.6%/yr previously). In annual average terms GDP growth is forecast to be 3.5% in 2022 (from 4.7% previously) and a below-trend 2.1% in 2023 (from 3.1% previously). The anticipated slowdown in GDP growth to a below-trend pace over 2023 will see the unemployment rate grind higher. We expect the unemployment rate to move up over H2 2023 to end the yearat~4½%.

Home price forecasts

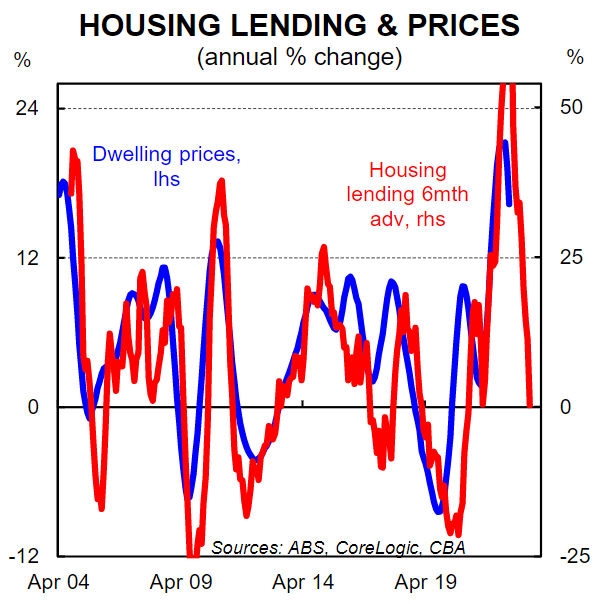

National dwelling prices peaked in April and posted a small decline in May. As is generally the case, the data has been mixed at the capital city level. Home prices have fallen in Sydney and Melbourne for a few months while prices in other parts of the country are still rising. Notwithstanding, we are confident that prices at the national level, as measured by the CoreLogic 8 capital city benchmark, hit their cyclical high in April (on the eve of the RBA’s first rate hike).

In many respects the outlook for dwelling prices is a simple story. The price that someone is willing and able to pay for a home is predominantly influenced by two things –income and borrowing rates. When borrowing rates are lowered for a given level of income people are generally willing to pay more for a home as they can service a larger mortgage. Conversely when mortgage rates rise the amount someone is able and willing to spend on a home falls for a given level of income.

Home prices will move lower from here given the RBA is expected to tighten policy via rate hikes quickly. The extent to which prices contract will depend in large part on the speed and magnitude at which the RBA lifts the cash rate.

Based on our updated forecast for the cash rate we expect home price falls nationally of around ~15% over the next eighteen months. Prices in Sydney and Melbourne are anticipated to decline by more than the other capital cities (see Table 1). The expected falls in home prices are significant. But context is key. Price gains in 2021 nationally were extraordinary. And therefore a contraction in dwelling prices is a natural response to rising interest rates given it was record low interest rates that drove the phenomenal lift in prices in 2021.

Home prices cannot be divorced from the broader economy and changes in home prices influence the economic outlook. Indeed they are a forward looking indicator (changes in home prices impact wealth, consumer confidence, spending decisions and employment). It could be the case that movements in home prices will feed into the RBA’s policy deliberations if prices slide too quickly.

The RBA in 2023

Based on our expectation for the RBA to front load the tightening cycle and take the cash rate to what we deem a contractionary setting of 2.10% by end-2022 we do not expect any further rate hikes in 2023.

Financial conditions will continue to tighten over 2023 even if the RBA does not take the cash rate higher over the year given the large fixed rate home loan expiry schedule. Fixed rate borrowers will be rolling off an average fixed rate mortgage of around 2¼% onto a rate with a 4-handle on it in 2023 based on our forecast profile for the cash rate. This will result in a very big step change in the interest cost on debt (for context, mathematically moving from a mortgage rate of 8% to 16% is the same as 2% to 4% in terms of what happens to the interest cost on debt; it doubles).

Our expectation is that economic momentum will slow significantly under the weight of a contractionary monetary policy setting in 2023. As such we expect to see policy easing on the agenda in H2 2023. We have pencilled in 50bps of rate cuts in H2 2023.

Concluding thoughts

Both the monetary and fiscal authorities are equipped with tools that can solve problems. But in the case of the RBA the cash rate is a very blunt tool to address some of the supply side issues in the domestic and global economies right now that are contributing to higher inflation.

Higher rates will not put downward pressure on the local price of electricity, gas, oil or food. These items are non-discretionary and their price rises hit all households, particularly those at the lower end of the income spectrum. This does not mean that rates shouldn’t be normalised as the labour market is tight and wages growth will rise. But the bigger medium term picture is absolutely paramount and there are other levers that can and should be pulled by policymakers to address some of the supply side issues, particularly around gas and electricity in Australia.