By Gareth Aird, head of Australian economics at CBA:

Key Points:

- The RBA is widely anticipated to raise the cash rate at the July Board meeting.

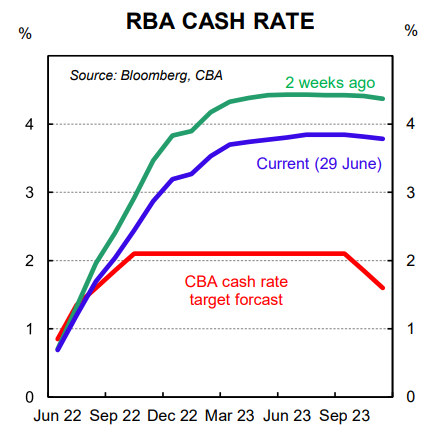

- We expect the RBA to increase the cash rate by 50bp in July, which would take the cash rate target to 1.35%.

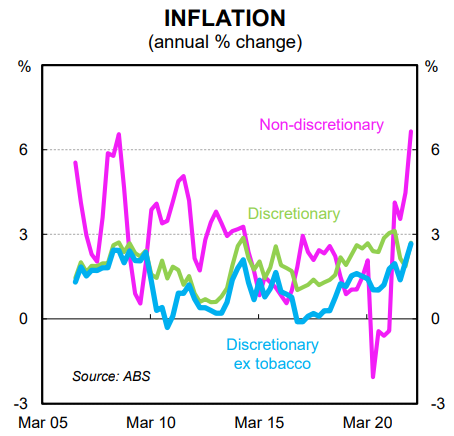

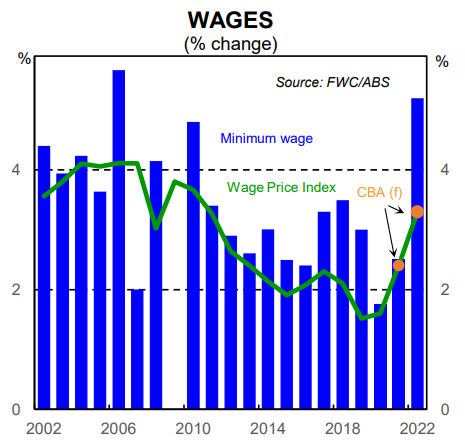

- The Governor will likely refer to the increase in the 2022/23 minimum wage of 5.2% and the RBA’s recent upward revision to their assessment of the near term inflation outlook as justification for a consecutive 50bp rate increase.

A 50bp hike next week seems the most obvious policy choice

The RBA Board meets on Tuesday 5 July. There is universal agreement amongst economists and market participants that the RBA will deliver another rate hike. Indeed the RBA Governor has all but assured financial market participants that the cash rate will be raised in July given his comments at his address to the American Chamber of Commerce in Australia (AMCHAM) on 21 June.

Following his speech the Governor was asked what policy outcome might be expected at the July Board meeting following the “business as usual” 25bp increase in the cash rate in May and the “surprise” 50bp rate rise in June. The Governor replied:

“The Minutes of the Board meeting are coming out later this morning and in those Minutes you’ll see that we discussed the possibility of a 25bp increase or a 50. In the end, we decided on a 50bp increase because of the upward revision to the inflation outlook and the recognition that interest rates were still very, very low for an economy that was experiencing high inflation and had such low unemployment. I would expect that we would have the same discussion again at the next meeting. As I said in my prepared remarks, we’re not on a pre-set path. We’re going to look at the data that we have each month and at the level of interest rates and the inflation outlook, but I expect that next month we’ll be having the same discussion at our Board meeting: 25 or 50.” (our emphasis on bold re what the Governor’s comments imply for the July Board meeting).

The Governor was then asked a follow-up question on whether a 75bp rate hike would be off the table in July to which he replied, “That’s your language. I’m saying that’s what we discussed last time and we will discuss that. That Board meeting is still a couple of weeks to go, so other things can happen, but at the moment I think that will be the decision we’ll be taking – either 25 or 50 – at the next meeting.”

The Minutes from the June Board were interesting as they made a strong case for a 25bp increase in the cash rate in June. And yet the Board opted for a 50bp hike.

The June Board Minutes noted, “The argument for an increase of 25bp was that a sequence of 25bp moves represented a steady approach to withdrawing monetary policy stimulus and that this was appropriate in an uncertain environment …….. While some central banks had been increasing policy rates in 50bp increments, these central banks meet less frequently than the Reserve Bank Board.”

Regular readers will recall that CBA expected a 25bp ‘business as usual’ hike at the June Board meeting for very much the same reasons as the June Board Minutes argued the benefits of moving in 25bp increments.

At the July meeting the RBA Board will therefore make a decision between raising the cash rate by 25bp or 50bp. A 75bp increase would be very much at odds with the Governor’s recent comments that a 25bp or 50bp move would be discussed in July. Equally, policy on hold in July would leave market participants perplexed.

On balance, we favour a 50bp hike in July.

The RBA now appears intent on front loading the tightening cycle despite the Governor stating in his 21 June speech that, “I want to emphasise though that we are not on a pre-set path.”

The market prefers consistency in policy communication and action. That does not mean the market requires forward guidance. Indeed maintaining rigid forward guidance when the facts change is very much want the market does not like.

However, it does not make sense to chop and change between a series of 25bp and 50bp hikes over coming months. Indeed we believe that once the RBA drops back to a ‘business as usual’ 25bp rate hike at any near term monthly Board meeting the probability of then delivering a larger 50bp hike at a future meetings in this tightening cycle would be very low.

Put another way, a potential sequence of rate hikes of 25bp in May, 50bp in June, 25bp in July and 50bp in August would be unwelcome. It is much better to move by 50bp in July and make a judgement around 25bp or 50bp in August based on the evolution of the data and the outlook for both inflation and the economy.

Is CBA dovish or hawkish?

We have found ourselves over the past year in the CBA Australian economics team being labelled at different times as hawkish and dovish.

Over 2021 we argued that the RBA’s inflation forecasts were much too low and the 2024 conditional forward guidance on the cash rate was well off the mark. Our expectation from late 2020 was that Australia’s economic recovery would be V-shaped and we first called a rate hike as most likely in 2022 in mid-2021.

The delta lockdown complicated our thinking on the economy in the short term. But we retained our hawkish tilt on things when earlier this year in February we surprised market participants when we shifted our central scenario for the RBA to commence normalising the cash rate to June 2022, from August 2022 (the timing of that shift appeared counterintuitive given on 11 February 2022 the RBA Governor stated “another couple of CPIs would be good to see” when asked if he would like to see at least one or two more CPIs before concluding inflation is sustainably within the target range).

In recent months though we find ourselves on the more dovish end of the street. In truth our thinking on the economic outlook or the power of rate hikes has not materially shifted.

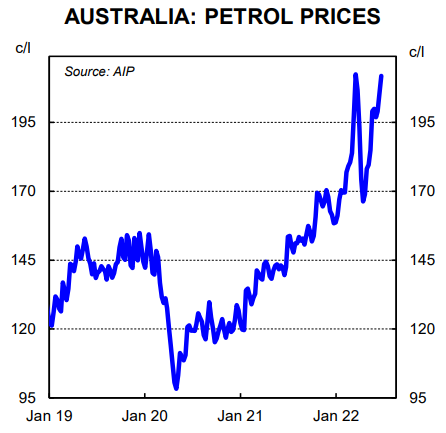

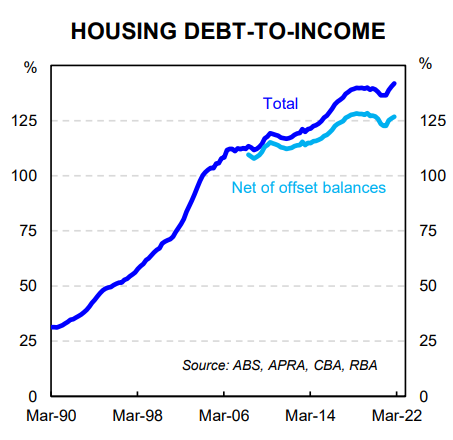

We expected inflation pressures to be significantly strong for the RBA to commence normalising the cash rate following a red-hot Q1 22 CPI (albeit we thought they would wait for the data on labour costs and deliver a first increase in the cash rate in June). The war in Ukraine and floods on the East Coast have intensified near term inflation pressures. But we remain of the view that the neutral rate in Australia is very low given our highly indebted household sector and rate hikes will be powerful. We believe there are early signs in some key economic data that our call for a relatively low terminal rate of 2.1% is the correct one.

It takes time for the activity data to slow following policy tightening and near term inflation prints will remain elevated. But the most interest rate sensitive parts of the economy are already responding to rate hikes.

Home prices have begun their descent and tomorrow (i.e. Friday 1 July) we expect the CoreLogic data to indicate that national home prices fell by ~0.9% in June (Sydney, our biggest market, is forecast to be down 1.5% over the month).

Home prices cannot be divorced from the broader economy and changes in home prices influence the economic outlook. Indeed they are a forward looking indicator (changes in home prices impact wealth, consumer confidence, spending decisions and employment).

Real wages are very much in the red zone and consumer confidence over recent months has moved into a deeply pessimistic territory. That picture is unlikely to turn around anytime soon which means consumer discretionary spending is likely to retreat. There is already some evidence of that occurring in our high frequency credit and debit card spending. Recall that we downgraded our outlook for GDP growth following the RBA’s 50bp rate hike in June.

The economic outlook of course is not all negative and the labour market will continue to perform well over 2022. Wages growth is also expected to continue to lift. But we remain comfortable with our view that the terminal rate will be low this cycle, particularly in light of the speed at which some key data is already reflecting the impact of policy tightening. A 50bp rate hike next week at the July Board meeting will further accelerate the dampening impacts of rate hikes on the economy.