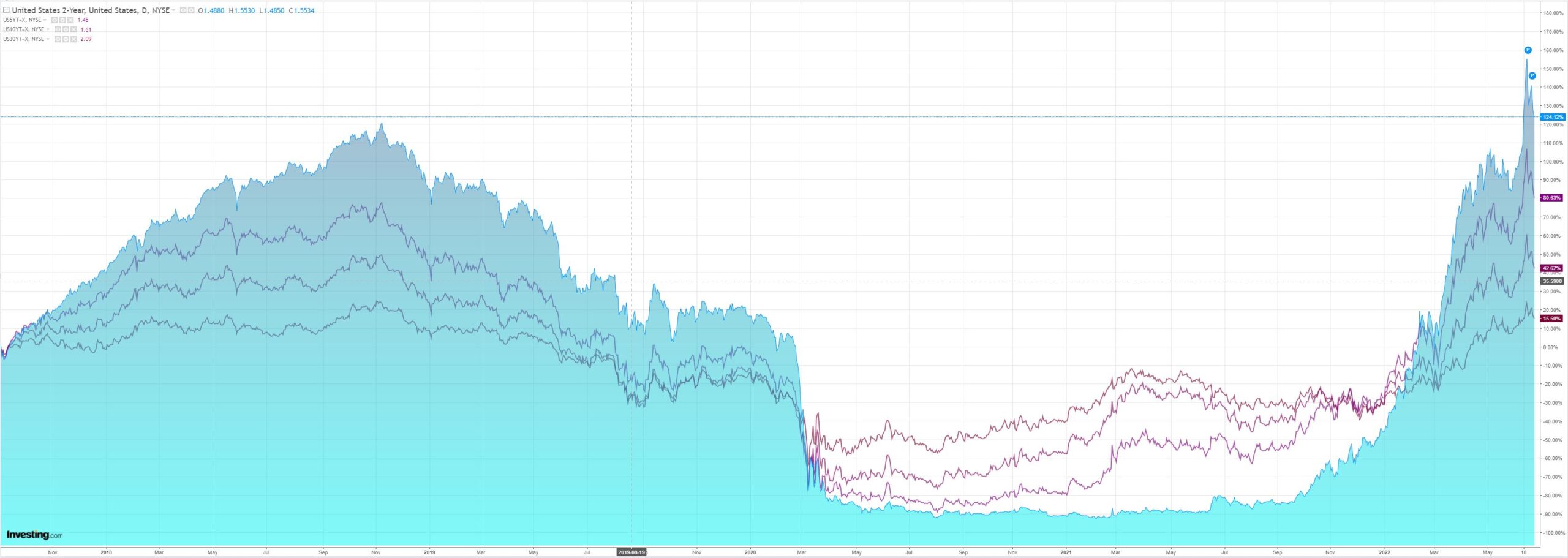

Treasury yields appear to have peaked properly now:

Which lifted growth stocks:

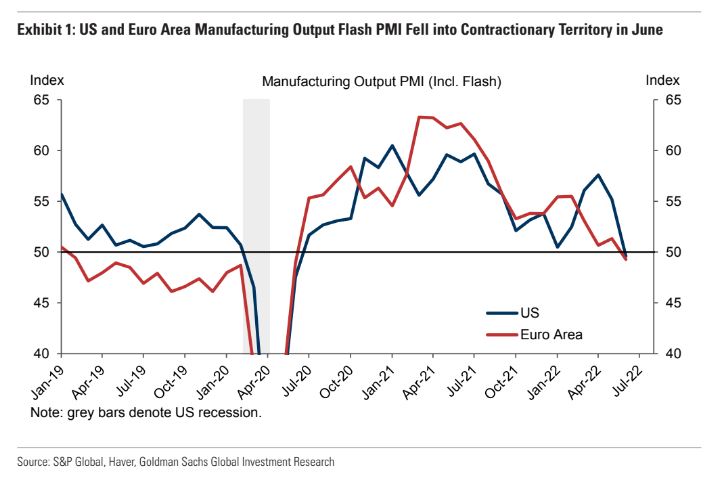

Westpac has the wrap:

Advertisement

Event Wrap

In his second semi-annual Congressional testimony Powell underscored the Fed’s resolve to fight inflation whilst acknowledging the cooling of the US economy but stated that it could avoid recession.

US Flash June PMI surprised to the downside. Manufacturing fell to 52.4 (prior 57.0, est. 56.0) and Services slipped to 51.6 (prior 53.4, est. 53.3).

S&P cited a notable decline in demand causing new orders to contract for the first time since July 2020 and manufacturing production also fell into contraction (at 49.6, lowest in 24 months).The survey did suggest that there are signs that pricing pressures have peaked.

US June Kansas Fed Manufacturing survey slipped to 12, close to the estimate of 13, from prior 223.

US initial (226k) and continuing (1.315mn) claims were lose to estimates and had little market impact.

Eurozone Flash June PMIs were decidedly soft. Manufacturing slipped to 52.0 (est. 53.8, prior 54.6), Services pulled back to 51.9 (est. 55.5, prior 56.1) and Composite slid to 51.9 (est. 54.0, prior 54.8). The fall in activity was to the lowest in 16-months with S&P citing stalling demand as pandemic related pent-up demand fades.

UK Flash June PMIs were less weak, though S&P cite expectations showing as declining. Composite held unchanged at 53.1 (est. 52.4) as services held solidly at 53.4 (prior 53.4, est. 52.9) though manufacturing did dip to 53.4 (est. 53.6, prior 54.6). S&P noted the slide in new orders to 50.8 (prior 53.8) and declining optimism suggest that UK faces “a troubling combination of recession and elevated inflation”.

UK CBI June Sales Survey showed a fall in reported sales to -5 (from -1, est. -3).

UK May Public Sector Net Borrowing of GBP13.2bn was higher than the expected GBP11.5bn, with upside revisions to April (GBP21.1bn, initially GBP17.8bn).

Event Outlook

Aust: RBA Governor Lowe will participate in a panel concerning global monetary policy challenges at Zurich at 9:30pm AEST.

NZ: Matariki public holiday; markets closed.

Japan: Weakness in underlying consumer price pressures is anticipated in May (market f/c: 2.5%yr).

China: The final estimate of the Q1 current account balance should confirm a healthy surplus.

Ger/UK: The German IFO business climate survey will continue to reflect an uncertain outlook (market f/c: 92.8). Russia-Ukraine and inflation headwinds has led GfK consumer confidence to the weakest level in series history dating back to 1980 (market f/c: -40).

US: The final estimate of the June University of Michigan consumer sentiment survey will confirm the collapse in confidence amid historic inflation pressures (market f/c: 51.2). New home sales should be under pressure from rising interest rates and costs in May (market f/c: -0.2%). Meanwhile, the FOMC’s Bullard and Daly are due to speak at separate events.

Sell the recession rumour and buy the fact was the theme of the evening as global PMIs tanked:

The DM composite flash PMI decreased by -1.8pt in June to 51.9 on a steep deceleration in services (-2.9pt to 52.5) and broad-based moderation in manufacturing (-1.6pt to 52.5).

Leading indicators were much worse and there is more ahead.

Advertisement

US (and global recession) is fast moving to the consensus and much earlier than anybody (except yours truly) predicted. The question for markets now is, is it priced?

If it is mild then FX is getting there but equities still have a way to go.

If it is more severe then neither is finished by some distance.

My own view is that the recession will be at the more damaging end of the spectrum given the triple shock of European war and energy, Chinese property and OMICRON, and US bullwhip effects around inflation, rates and inventories.

Advertisement

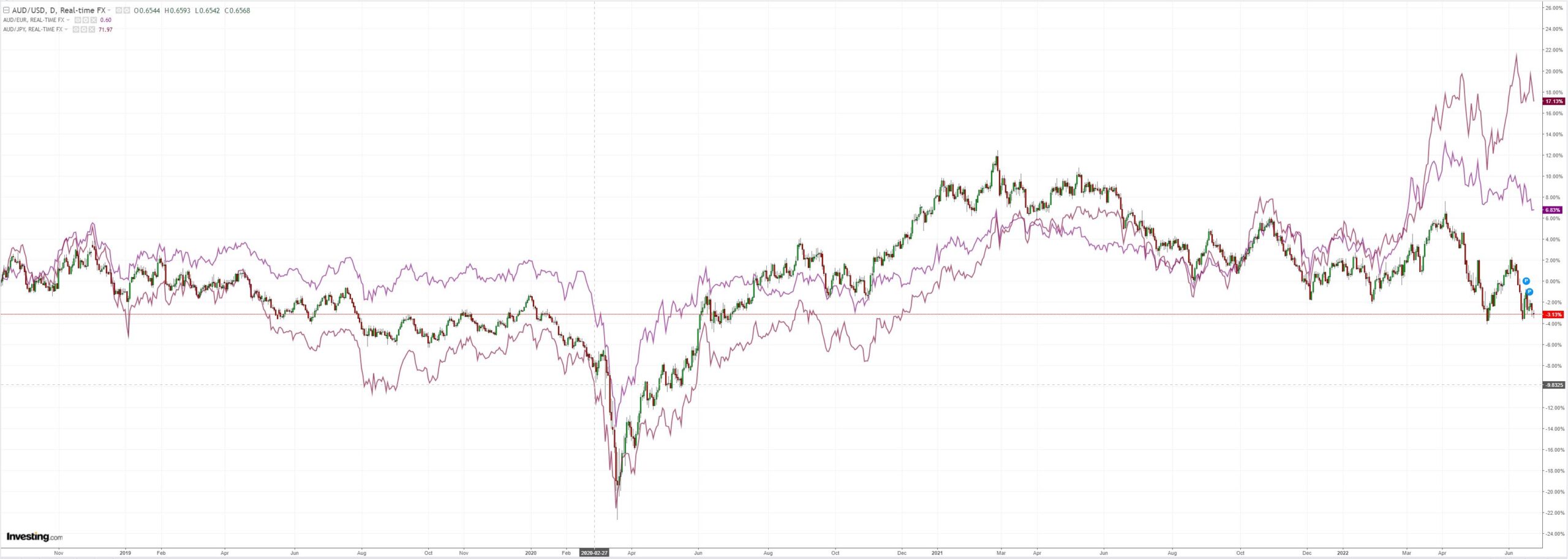

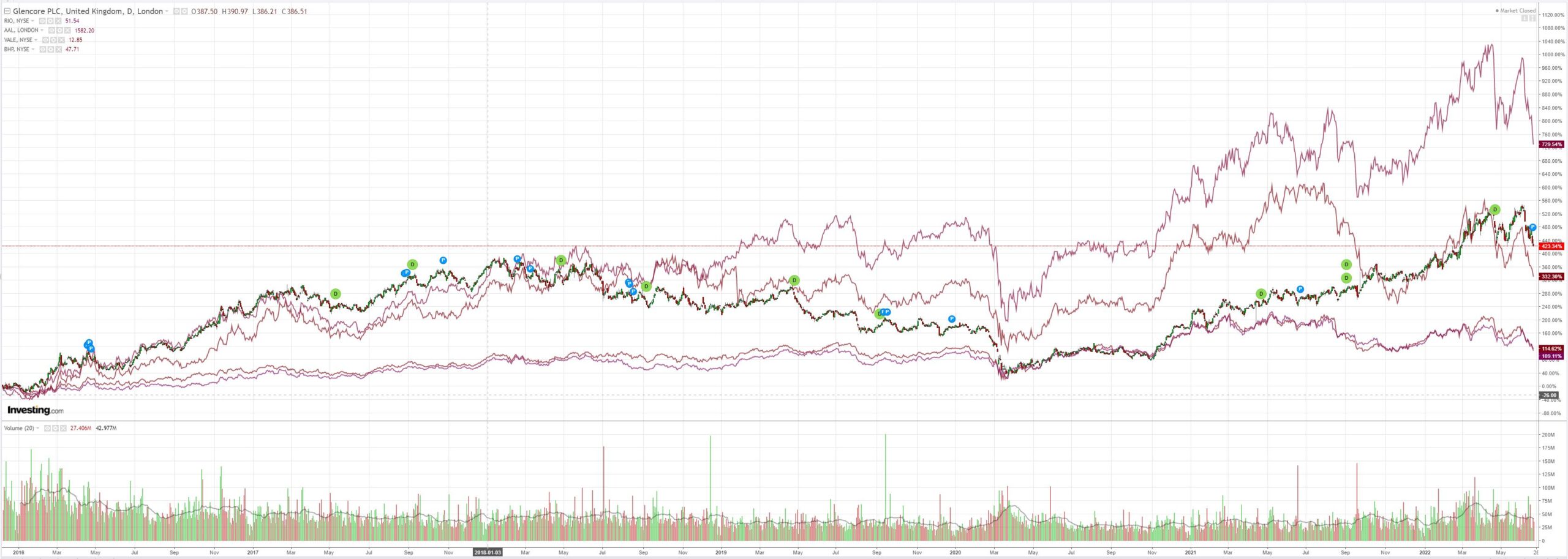

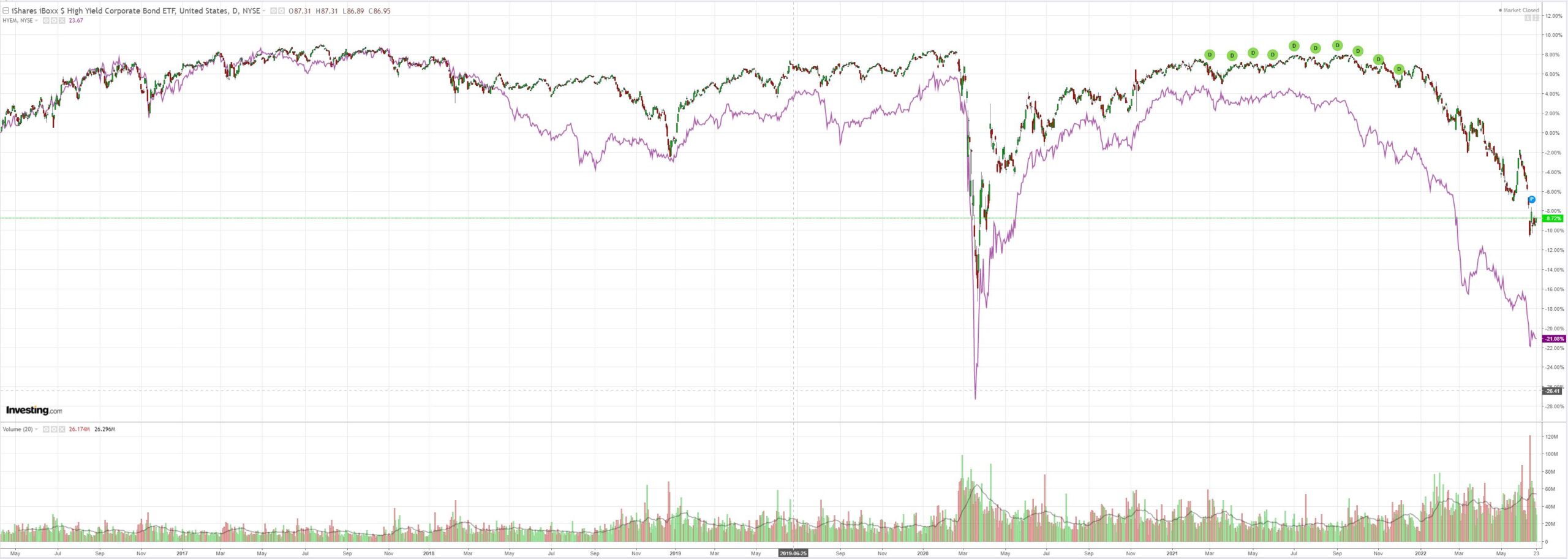

So, I see more downside yet for commodities, equities and AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.