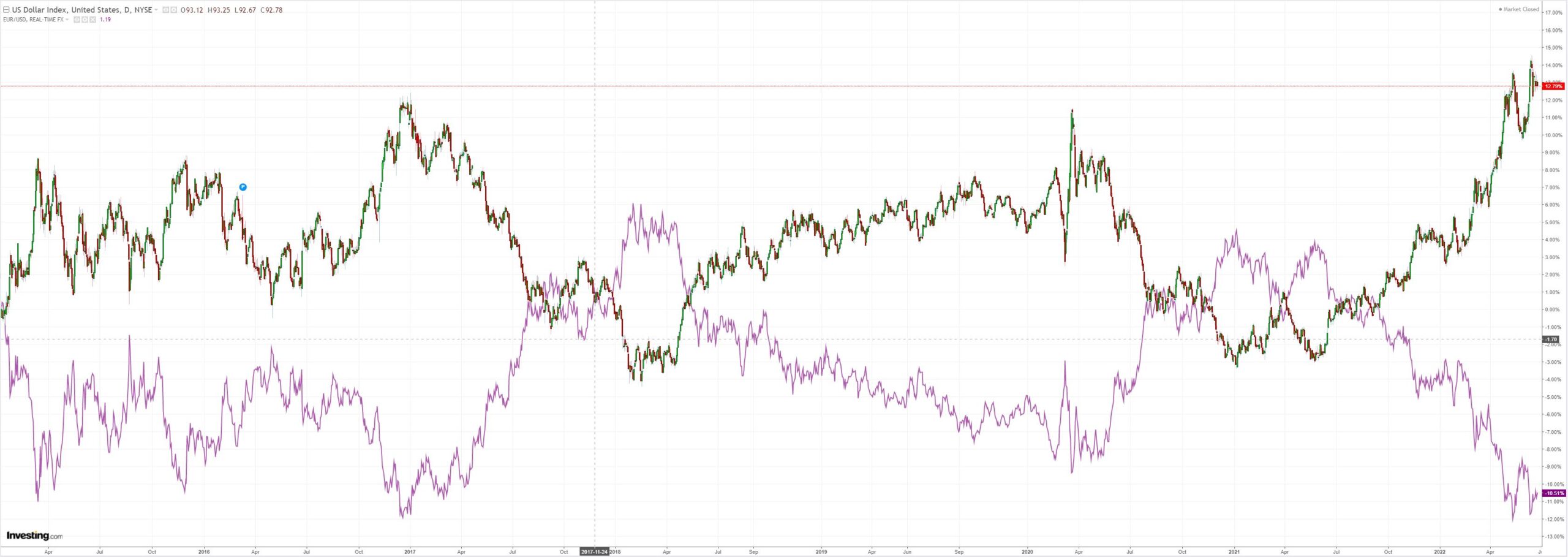

DXY eased on Friday night:

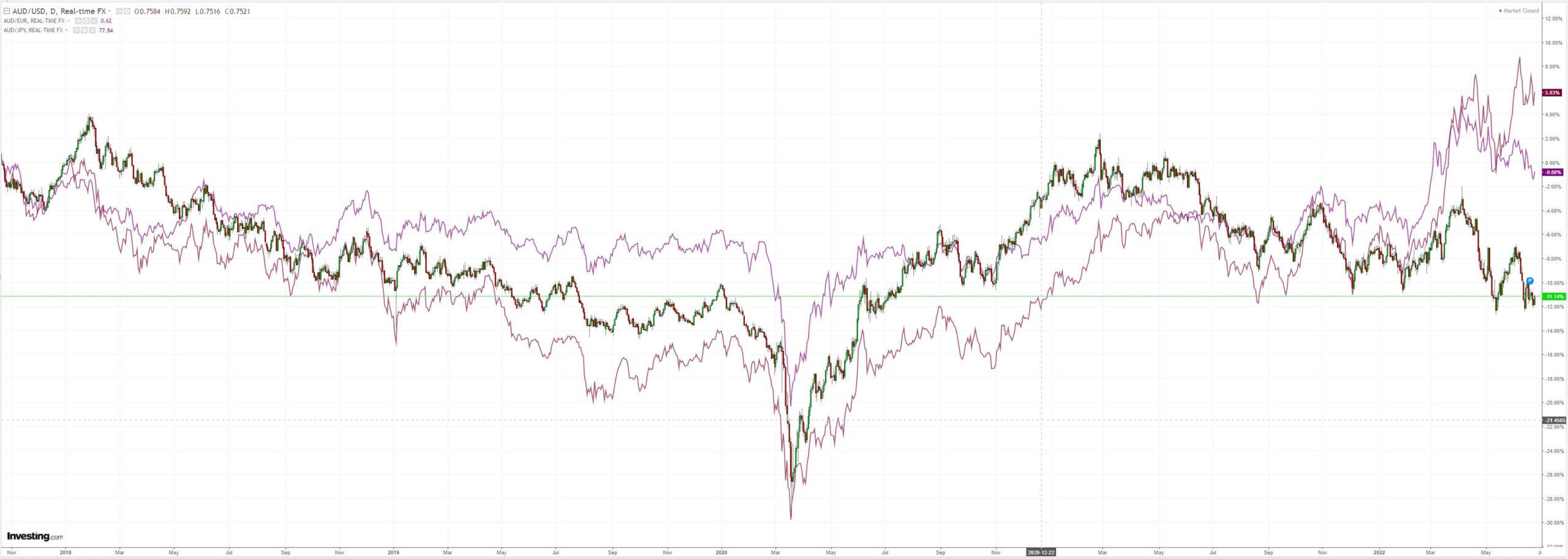

AUD was the drunkest bum at the global party:

Sadly for all, oil took off:

DXY eased on Friday night:

AUD was the drunkest bum at the global party:

Sadly for all, oil took off:

The full text of this article is available to MacroBusiness subscribers