Sadly for all, oil did not fall after Libya stopped exports:

Advertisement

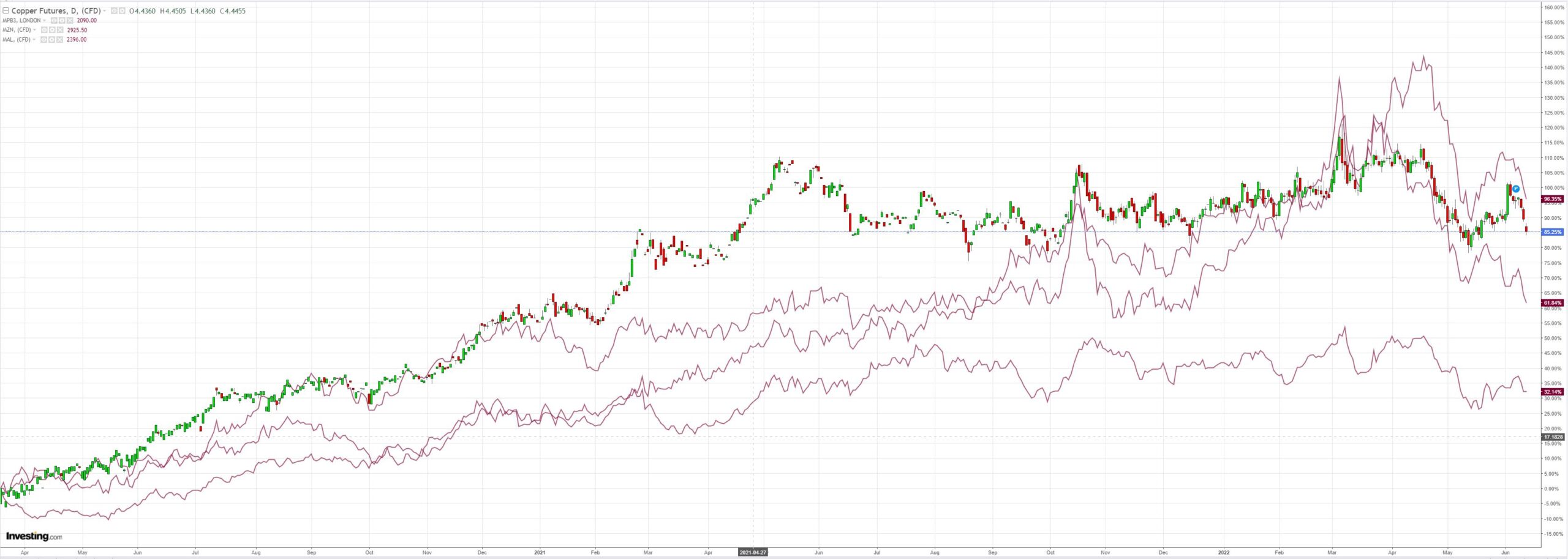

Miners were axed:

As metals diverge from energy given the looming recession:

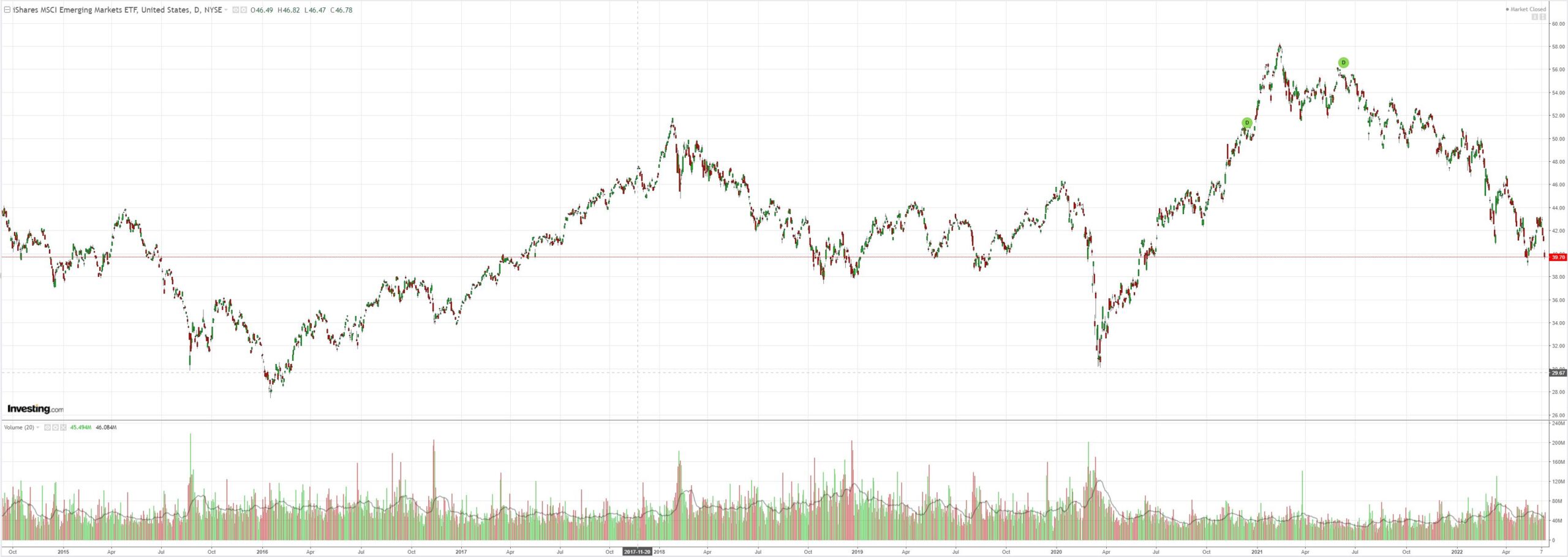

EM stocks were slaughtered:

Advertisement

Global junk is in a new GFC:

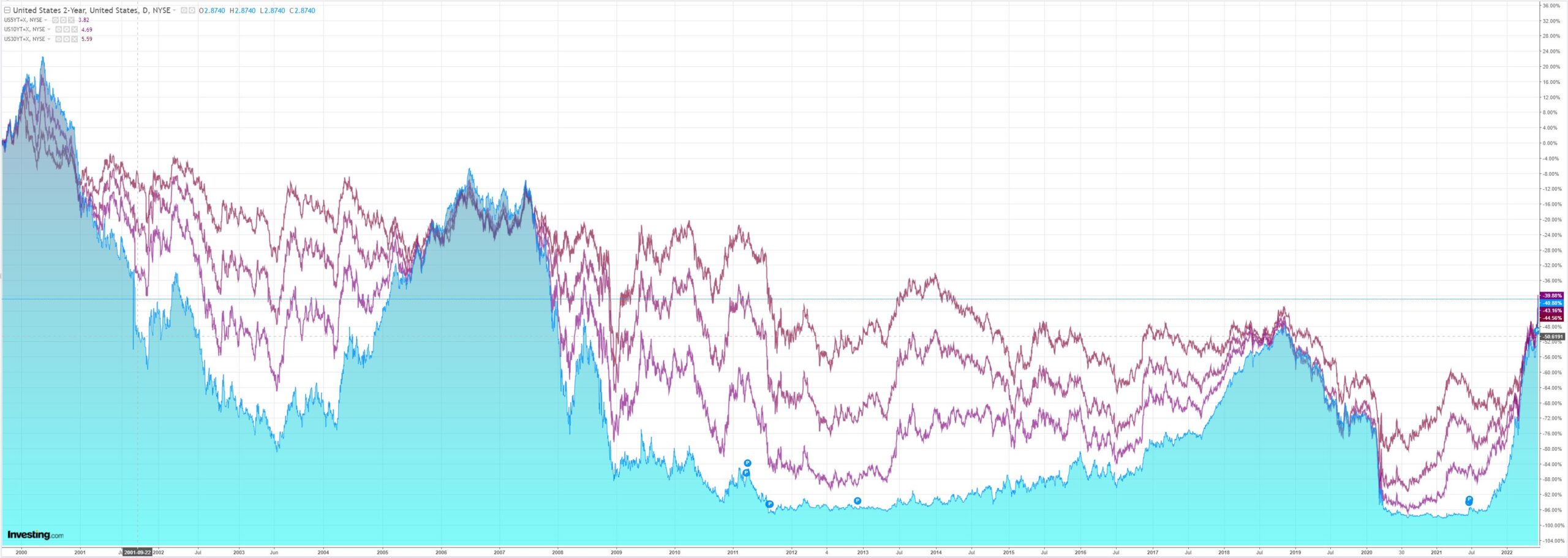

US yields jackknifed as markets imagine all kinds of Fed hawkishness:

Advertisement

Stocks crashed:

Westpac has the wrap:

Event Wrap

UK production data for April was weak across the board. GDP fell 0.3%m/m (est. +0.1%m/m, prior unchanged at -0.1%m/m), ONS noting that this was the first month since Jan. 2021 that all component sectors contracted. Industrial production fell 0.6%m/m (est. +0.3%m/m), manufacturing -1.0%m/m (est. +0.2%m/m), construction -0.4%m/m (est. -0.5%m/m), and services -0.3%m/m (est. +0.1%m/m).

Event Outlook

Aust: The May NAB business survey will provide insight into how the Federal Election result and the RBA’s first rate hike was received.

NZ: Supply and staff shortages will be adding further upward pressure to food prices in May (Westpac f/c: 0.8%).

Japan: The final estimate for April’s industrial production is due.

Eur/UK: The ZEW survey of expectations should continue to reflect the weakness in European confidence in June. Meanwhile, the UK’s ILO unemployment rate is expected to push further below pre-pandemic levels in April (market f/c: 3.6%).

US: Ongoing supply issues are expected to keep producer prices elevated in the near-term (market f/c: 0.8%), which in turn will continue to impact small business optimism in the NFIB’s May survey (market f/c: 93.0).

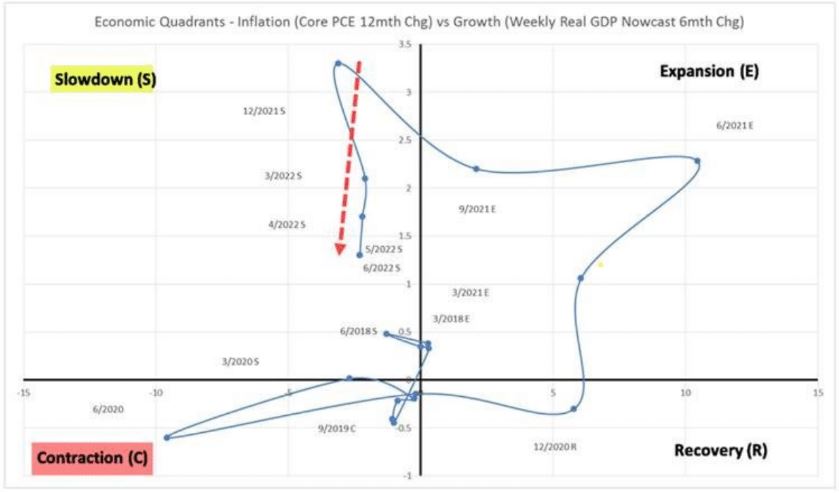

Nomura sums it up:

Advertisement

This past Friday’s blistering US CPI upside shocker, alongside the horrific outputs on U Mich -Sentiment and -Inflation Expectations, crystalized the “worst fears confirmed” of a market which simply has nowhere left to hide except for USD and Long Vol, as even Commods are “giving back” today, on repricing of the Central Bank “FCI tightening left tail,” which means “hard landing” Recessionodds again ratcheting higher and pricing a full Fed “cut” btwn Jun23-Dec23.

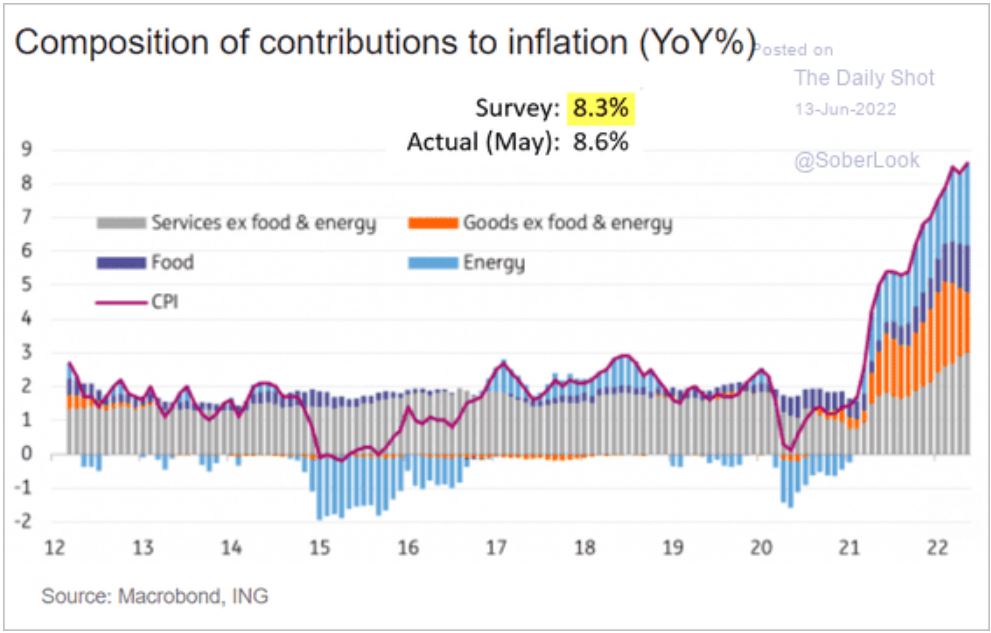

Yep. The Fed has to kill oil and it will take a major recession to do it. It is no more complex than that. Goods are deflating. Services will as housing slows and Labor markets ease. It’s all about energy (which is food) now:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.