Australia confronts fixed rate mortgage tsunami

RateCity’s Sally Tindall warns that millions of Aussies that locked in ultra low fixed mortgage rates during the pandemic face a massive rise in mortgage repayments when their loan terms expire:

“Borrowers’ fixed rate immunity will only last for so long. When the merry-go-round stops, it’s going to be a shock for many because their new rate will be significantly higher,” [Tindall] said…

The analysis, which covered the big four banks’ half-year results and APRA loan book data, shows about 38 per cent of home loans are currently fixed, in dollar terms, with the peak of people coming off their fixed rates around mid-to-late 2023.

Westpac has the highest proportion of fixed mortgages as 40 per cent, followed by CBA’s 38 per cent, NAB’ 37.4 per cent and ANZ’s 35 per cent.

On a 500,000 principle and interest loan fixed in July 2021 for two years at a rate of 1.94 per cent, the current payment is $2105 per month.

When the fixed rate ends in July 2023, the average revert rate is likely to be about 5.68 per cent, if forecasts for the cash rate are realised, sending monthly repayments to $3042 – an increase of $937 per month.

Tindall’s analysis is conservative based on current interest rate forecasts.

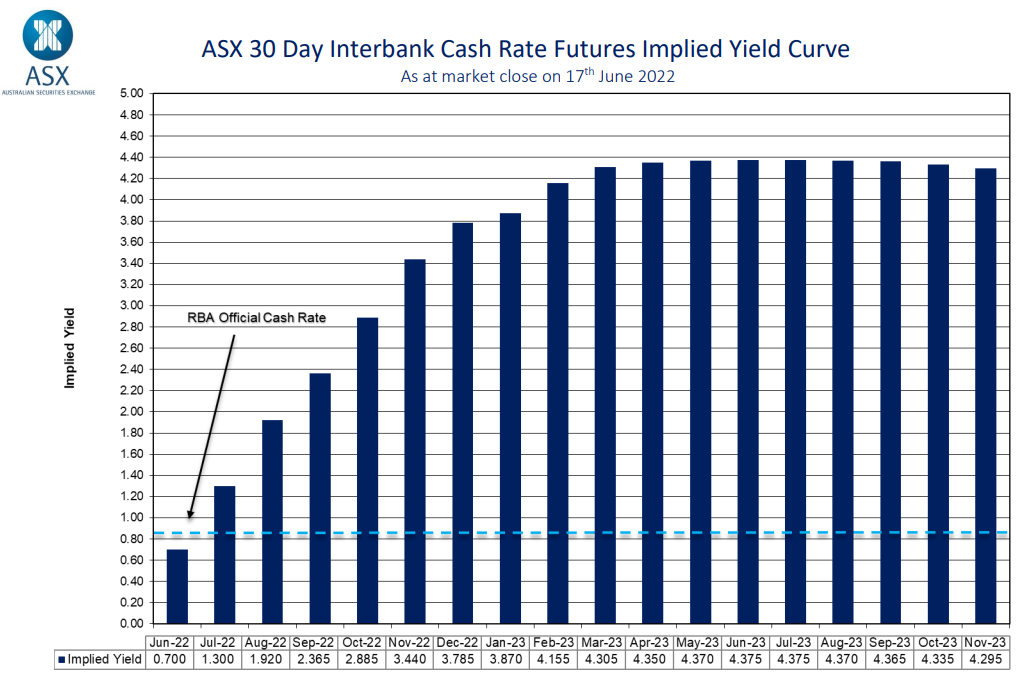

The futures market is tipping that Australia’s official cash rate (OCR) will be at 4.3% by the time that most fixed rate mortgages expire in late 2023:

Market interest rate forecasts are scary.

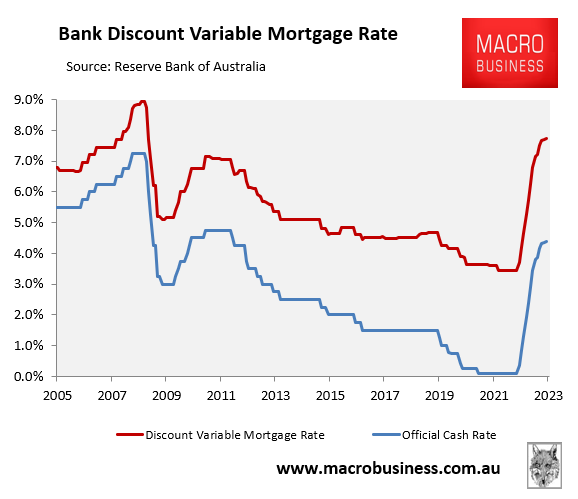

If this forecast comes to fruition, it would drive the average discount variable mortgage rate to around 7.7%, assuming increases in the OCR are passed onto mortgage holders:

Australia’s discount variable mortgage would more than double.

In turn, borrowers that secured ultra-low fixed rate mortgages at below 2.5% would face a tripling in mortgage rates when it comes time to refinance. It would be a bitter pill to swallow, even for those that have built up substantial financial buffers.

Hopefully the market is dead wrong and the RBA stops hiking long before mortgage rates hit 6% or 7%. Otherwise Australia’s housing market will face its biggest price crash in more than 100 years.