The Reserve Bank of Australia (RBA) has released credit growth data for the month of May, which captures the first 0.25% hike in the official cash rate.

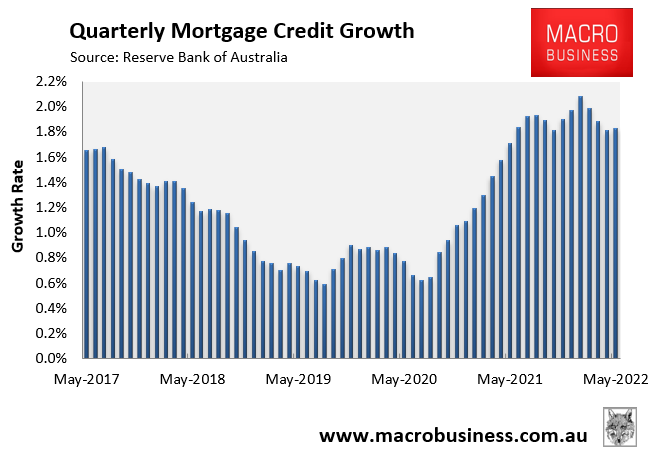

Mortgage credit growth rose by 0.6% over May, with the quarterly rate of growth rebounding slightly to 1.8%:

Rebound despite May’s 0.25% rate hike.

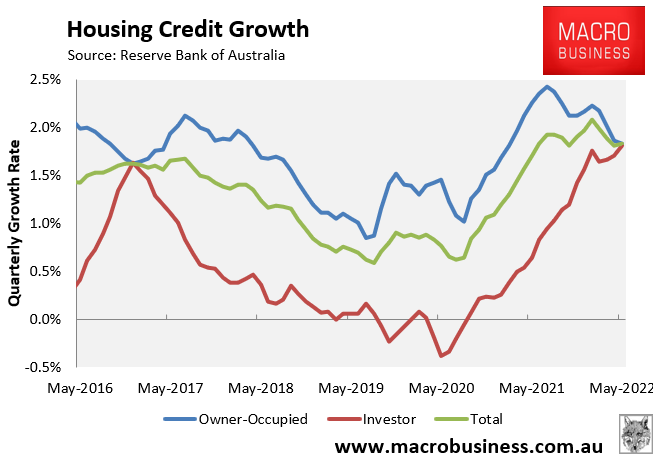

The quarterly rebound was driven by investors, which hit their highest level of mortgage growth since mid-2015:

Investors take over from owner-occupiers in driving mortgage growth.

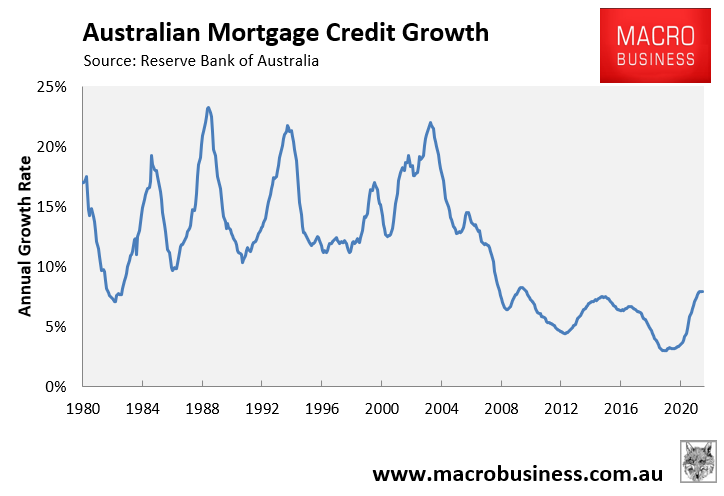

However, annual mortgage growth is topping out at 7.9%, and will likely soon begin to fall:

Annual mortgage credit growth tops out.

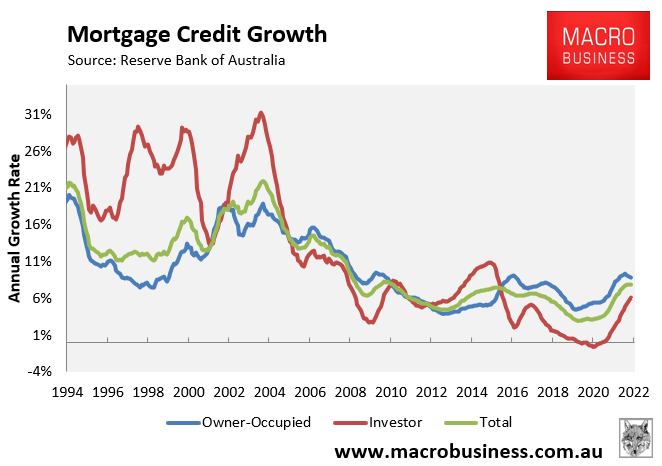

Again, investor mortgage growth is rising, while owner-occupier mortgage growth is on the decline:

Investor mortgage growth rising, owner-occupier mortgage growth falling.

With the RBA tipped to hike interest rates aggressively over the remainder of 2022, expect mortgage growth to fall as buyers wait on the sidelines.