Westpac with the index. Bill Evans is behind the times on what constitutes “stimulatory”.

—

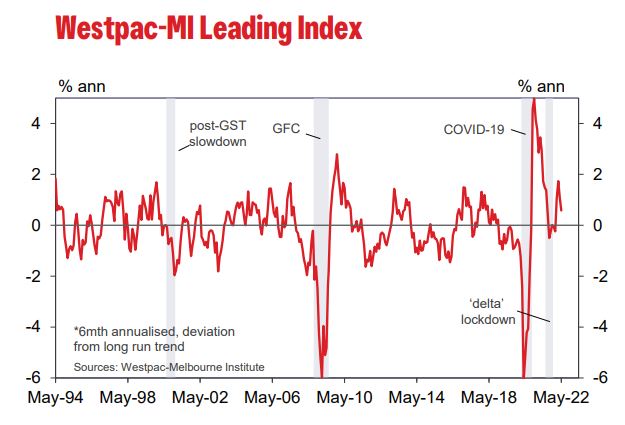

The components of the Index are indicating an important emerging theme around Australia’s growth prospects – a significant shock to consumer confidence. Declining consumer sentiment was a major contributor to the slowdown in May – the Westpac-MI CSI Consumer Expectations Index being one of the nine components. As we reported last week, the headline Westpac-MI Consumer Sentiment Index fell a further 4.5% in June, with the Consumer Expectations Index falling 4.2%.

Despite this, the overall growth rate in the Leading Index is still indicating above trend growth momentum heading into the three to nine month ‘window’.

Westpac concurs that the economy’s momentum will carry through the June and September quarters. Gains will centre on consumer spending which will continue to benefit from post-COVID reopening and support from high household savings rate and strong balance sheets.

The slump in Consumer Sentiment – under the weight of rising interest rates and falling house prices – is likely to take its toll on spending later in the year and into 2023. We expect this to see the growth rate in the economy fall below trend and should be foreshadowed by negative reads for the Leading Index growth rate later this year.

As noted, the Index growth rate is still comfortably in positive, above trend, territory and well up on the end of last year, having risen from -0.07% in December to the current 0.58%. The main components driving the improvement over the first half of 2022 have been a lift in commodity prices in AUD terms (adding 0.29ppts to the index growth rate); a widening yield spread (+0.21ppts); US industrial production (+0.18ppts); and dwelling approvals (+0.16ppts). These have been partially offset by sharp falls in sentiment-based components, the Westpac-MI CSI expectations index taking 0.15ppts off the index growth rate in particular; and a sell-off in equity markets, the S&P/ASX 200 taking 0.05ppts off the index growth rate. While positives have tended to wane in recent months, these two negatives have been intensifying.

The Reserve Bank Board next meets on July 5.

Yesterday the Bank released the Minutes to the June Board meeting. The key theme was that “the level of interest rates was still very low for an economy with a tight labour market and facing a period of higher inflation”.

We expect the Board will decide to follow the 50bp rate increase in June with a further 50bp increase in July.

That would still only have the cash rate at 1.35% – below the 1.5% we saw in the three years from August 2016 to May 2019 when the inflation rate was persistently below the bottom of the 2-3% range.

We also assess that 1.35% is below the neutral setting for policy indicating that even after the 50bp increase we expect for July the cash rate will continue to be stimulatory. Given the tight labour market and rising inflation further monetary tightening can be expected through 2022.