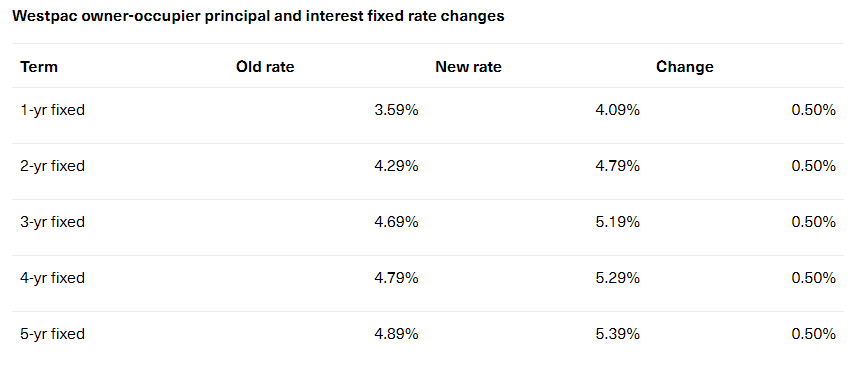

Westpac this week ratchetted up fixed mortgage rates by 0.5% across all loan terms:

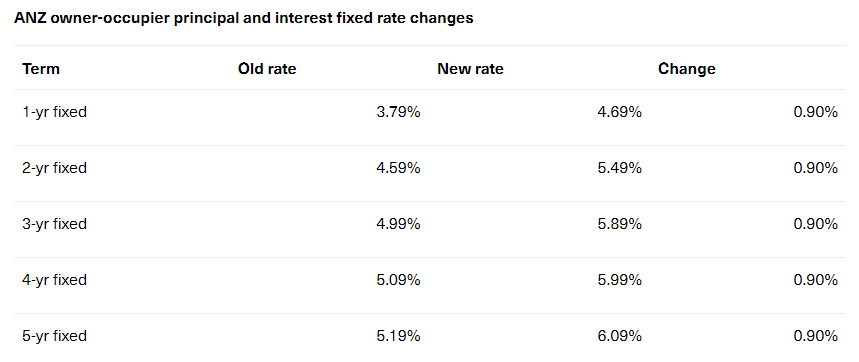

ANZ has been even more aggressive, hiking fixed rates by 0.9%, which has taken rates above 5% for most loan terms:

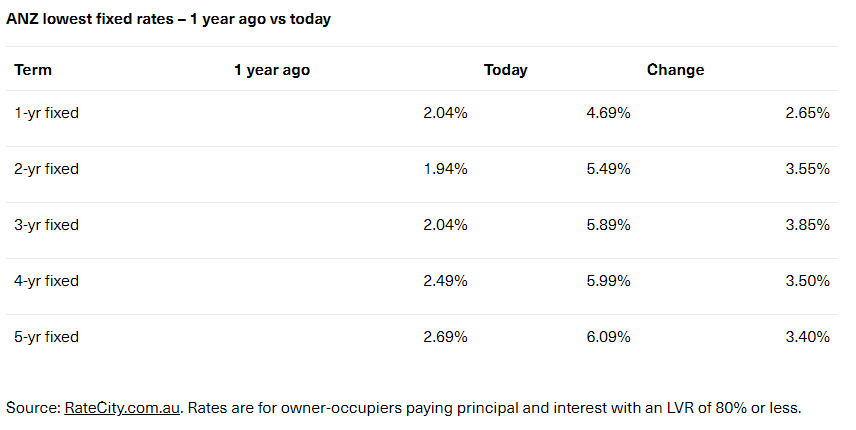

The next table illustrates the sharp lift in fixed rates over the past year, with rates already more than doubling from a year ago:

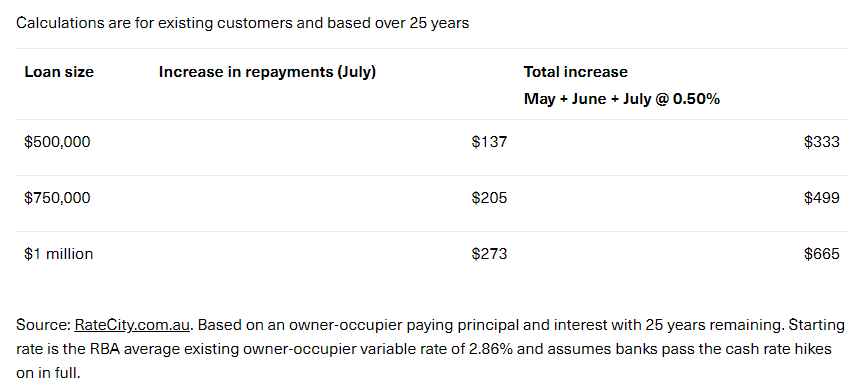

RateCity also notes that if the RBA hikes rates by 0.5% as expected at its next meeting, this will lift monthly variable mortgage repayments by between $333 and $665 on loans between $500,000 and $1 million, compared with repayments before the RBA began its tightening cycle:

Commenting on the results, RateCity’s research director Sally Tindall noted that indebted households are facing financial pain:

“While Governor Lowe has poured cold water on suggestions the cash rate could get to 4 per cent by Christmas, the Board is likely to continue its rapid-fire approach to cash rate hikes over the next six months.

“The RBA is ripping the low-rate band-aid off, and quickly. For many Australians it’s going to sting.

“Variable rate borrowers should prepare themselves for another double hike in July and for the cash rate to rise above 2 per cent by Christmas – potentially well above this mark.

Obviously if the futures market gets its way, and the official cash rate hits 3.25% by Christmas and 3.85% by May 2023, then there is going to be blood on the mortgage streets.