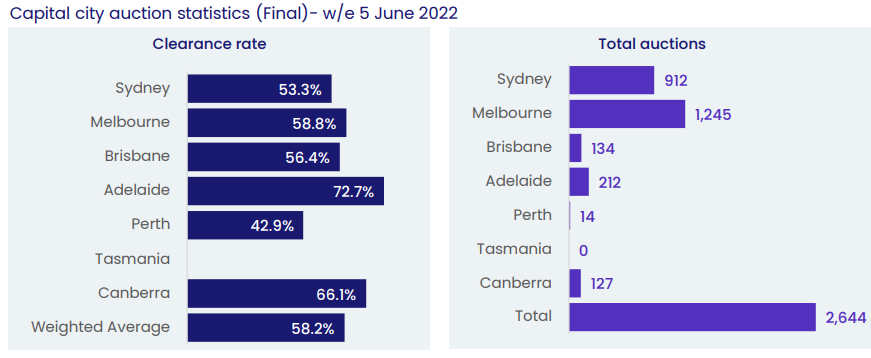

CoreLogic has released its final auction market results for last weekend, with the nation’s clearance rate falling to a fresh 2022 low of 58.2%.

The fall nationally was led by Sydney whose clearance rate plunged to just 53.3% – also a 2022 low. Melbourne’s clearance rate was higher at 58.8%, but also a 2022 low:

According to CoreLogic:

With 58.2% of last week’s auctions recording a successful result, the clearance rate fell 1.1 percentage points. Overtaking the week prior, last week’s clearance rate is now the lowest combined capital clearance rate since late August 2021 (58.0%) when Melbourne, Sydney and Canberra were in lockdown. This time last year 70.6% of auctions held were successful…

Melbourne’s clearance rate fell below 60% this week to 58.8%, down 1.6 percentage points from the week prior (60.4%). Last week’s result overtook the week ending 8th May (59.8%) as Melbourne’s lowest clearance rate of the year to date and lowest rate since Mid-September 2021 (58.5%). Of the 1,081 auctions held this time last year, 64.0% were successful…

Last week’s [Sydney] result was down 3.1 percentage points from the week prior (56.4%) and down 50 basis points from the week ending 15th May (53.8%) which was previously Sydney’s lowest clearance rate of the year. This time last year 75.6% of the 1,164 auctions held in Sydney were successful.

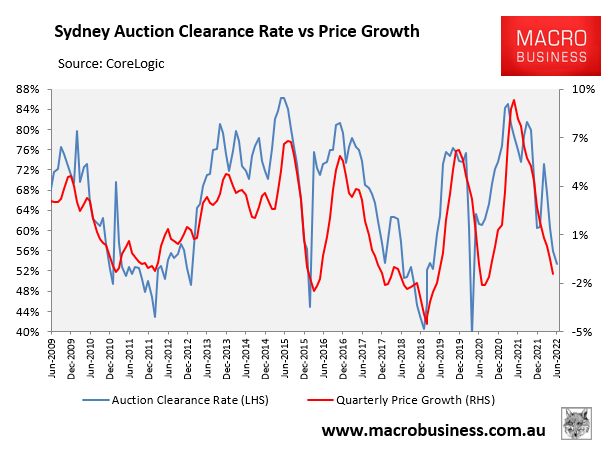

As shown in the next chart, the plunging auction clearance rate is pointing to accelerating price falls across Sydney:

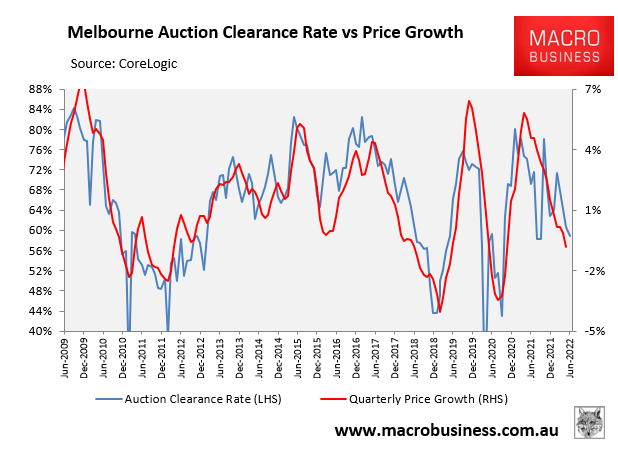

Auction clearances are also pointing to slower price falls for Melbourne:

Buyer demand is clearly evaporating. The Reserve Bank’s aggressive interest rate tightening will obviously make the situation worse.