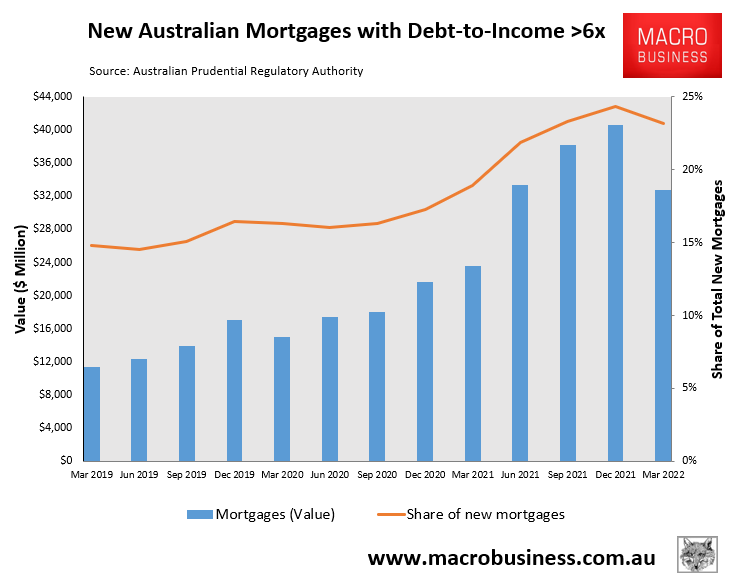

The Australian Prudential Regulatory Authority (APRA) has released its quarterly housing loan exposures, which shows that the percentage of mortgages originated with a debt-to-income (DTI) ratio above six fell to 23.1% over the March quarter, down from the record high 24.3% in the December quarter of 2021:

Nevertheless, the result was still way above the 18.9%, 16.3% and 14.8% of mortgages issued at a DTI above six in March 2021, March 2020 and March 2019 respectively.

Given the persistence of high DTI mortgages in Australia, APRA has issued new guidance to Authorised Deposit-taking Institutions (i.e. banks, building societies and credit unions) requesting they rein-in risky mortgage lending:

In a letter to banks yesterday, the Australian Prudential Regulation Authority outlined new requirements, saying lenders would ″need to have systems in place to limit growth in higher risk residential mortgage lending, such as loans at high debt-to-income multiples or high loan-to-valuation ratios″…

“In the current environment, with high household indebtedness and rising interest rates, it’s essential for banks to prudently and proactively manage risks in residential mortgage lending,” Mr Byres said on Tuesday.

The March quarter was also the first full period in which the impact of APRA’s move to increase the mortgage serviceability buffer from 2.5% to 3% was in place.

Other things equal, these moves by APRA will hasten house price falls by removing mortgage demand from the market.

Cheap and easy access to credit lifted Australian house prices by 35% over the pandemic. Now sharply rising mortgage rates and reduced credit availability should have the opposite effect in driving a serious house price correction.