ANZ Bank’s latest property focus has raised the risk of a deeper New Zealand housing market crash, with both prices and construction at risk of heavy falls:

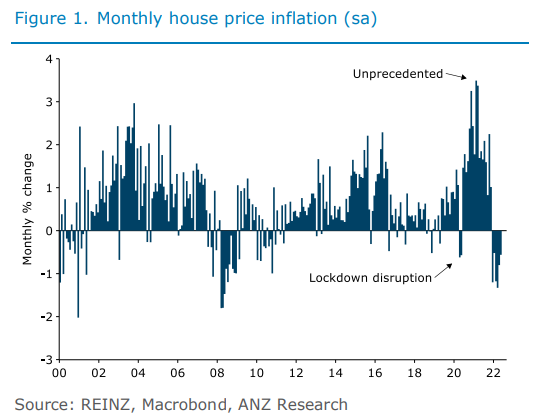

The housing market is continuing to cool, with May prices down 5.5% from their November 2021 peak (ANZ seasonal adjustment)… That’s six months in a row of moderate house price falls – not a crash by any means, but a reflection of the current (cooler) fundamentals of the market…

The available stock of real estate listings is now up 84% on last May’s (very low) lows. And that’s not coming from a surge in new listings. Rather, as sales volumes fall away and auction clearance rates plummet, houses are simply remaining on the market for much longer than we saw during the red-hot 2021 boom…

And while we continue to forecast what we’d call a soft landing for house prices (falling ‘only’ 11% over 2022), risks of a larger fall are there. In particular, sharp increases in global interest rate expectations have flowed through into still-higher mortgage rates in New Zealand – and while getting on top of CPI inflation with higher policy rates is the optimal thing to do from a sustainable economy perspective, house prices are likely to face larger near term declines if upside interest rate risks continue to materialise…

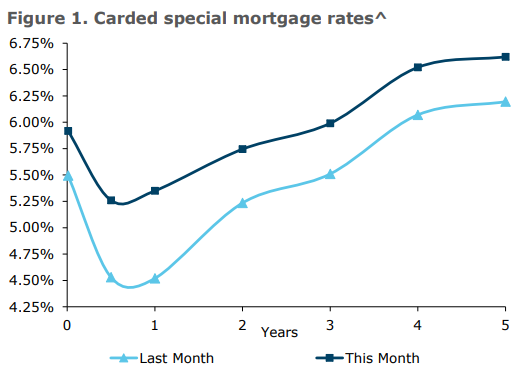

Mortgage rates have risen sharply over the past month. This has taken the average 1-year special rate offered by the major banks up to 5.35%, and the average 5-year rate up to just below 7%. Mortgage rates around these levels were commonplace in the decade before COVID, and aren’t particularly high in a historic comparison, but the pace of increases is unprecedented. The term structure of the mortgage curve remains steeply upward-sloping, making fixing for longer expensive. That’s not new, but we are now at a point where breakevens are so high that one has to expect significant further rises in interest in order for fixing for 2 years or more to be worthwhile. That could happen, but financial markets are already factoring in big increases, and the hurdle for a nasty surprise is now pretty high…

It’s also worth noting that according to RBNZ data, almost 60% of outstanding mortgage borrowing is fixed for less than a year. Households who may have taken advantage of the record-low interest rates over 2021 will find it challenging to maintain the same level of discretionary spend when facing mortgage rates that could be more than double their previous fix. As noted above, we think they’ll manage, and that should provide a floor under how far house prices will fall. But it will be at the expense of household consumption spending (ie GDP growth). That’s a feature, not a bug, of tightening monetary policy…

Bringing it all together, the housing market is cooling convincingly. And risks are building that we could see a more substantial decline than expected…

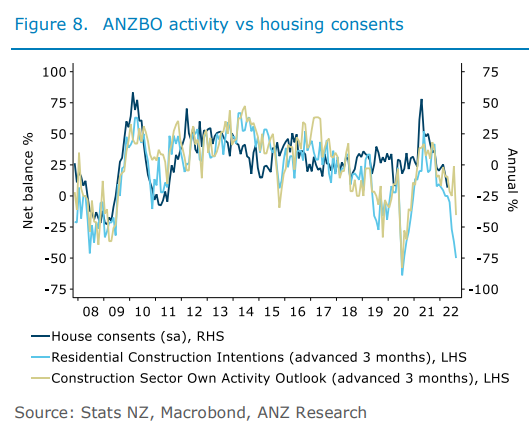

Residential investment is in the firing line as interest rates push higher to combat decades-high inflation, house prices fall, and shortages of both materials and labour continue to add uncertainty in the near term while limiting upside growth potential. In short, the calculus of building has shifted dramatically in the space of a few quarters and the stars are now aligned for an unwind. In fact, some indicators are already pointing sharply south…

Bringing it all together, we think residential construction activity is close to topping out (if it hasn’t already)… Overall, we have pencilled in around a 6% contraction in residential investment activity over 2023, which relative to previous cycles can very much be thought of as a soft landing…

So does negative growth in residential investment signal a looming recession? In short, it’s not a lock, but it certainly raises the risk. History tells us that residential construction activity can contract without pushing headline GDP into negative territory. At the end of the day, whether or not New Zealand enters a recession is very likely to depend on how households hold up through this…

At the end of the day, New Zealand isn’t just one big housing market, but it’s sure felt like it the last couple of years…