It’s one that readers will be familiar with, even if it’s taken Wall Street a while to catch up. I expect margins to be much worse than this as the everything shortage of 2022 turns to the everything glut of 2023 and pricing power goes bye-bye. Goldman has more.

—

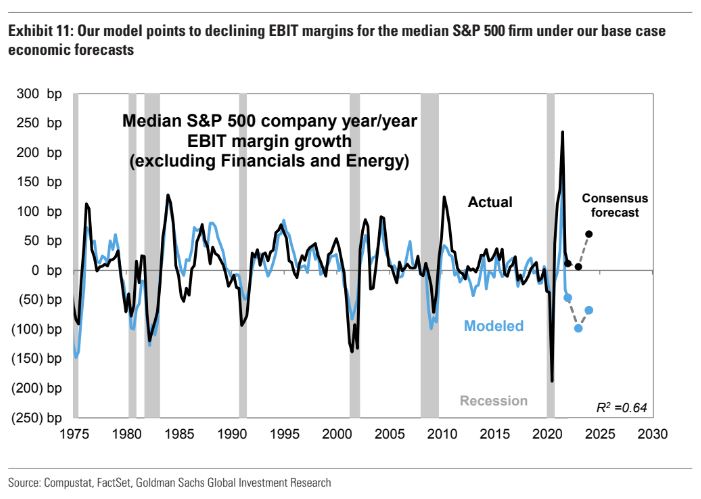

Profit margins for the median S&P 500 company will likely decline next year whether or not the economy falls into recession. Our model points to a 70 bpEBIT margin decline next year for the typical S&P 500 company in our economists’ non-recessionary base case, and a 130 bp compression in a recession scenario. In contrast, analyst estimates show the median stock’s EBIT margin expanding by 60bp next year.

Consensus margin forecasts suggest that earnings estimates are likely too optimistic. Analysts expect companies in nearly every sector will expand margins in 2023 relative to 2021. Consensus estimates are typically revised lower, but our model implies that larger cuts than usual are warranted today. Assuming no change in expected revenues, the margin compression we model would reduce the median stock’s expected 2023 EPS growth from +10% to 0%.

While investors are focused on the possibility of recession, the equity market does not appear to be fully reflecting the downside risks to earnings. The S&P500 decline this year has been driven entirely by falling valuations, which in turn have moved in line with rising interest rates. As a result, the equity risk premium remains close to where it started the year. While rotations within the equity market have signaled expectations of slowing growth, index valuation does not appear to be providing a buffer for the uncertainty around the path of future earnings.

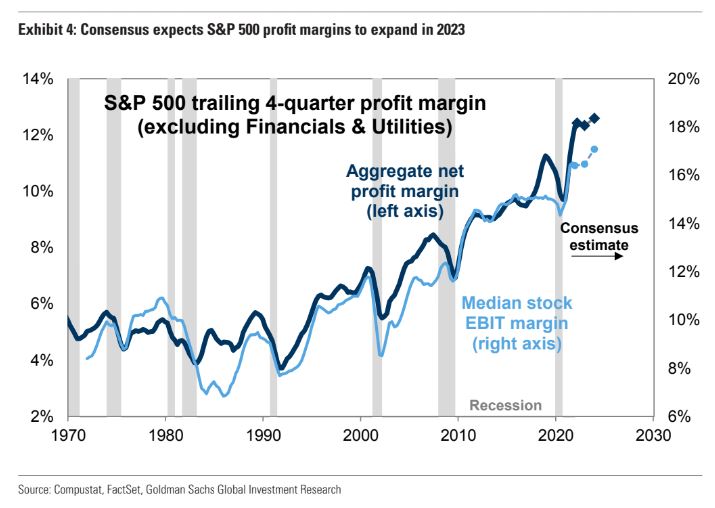

Rising borrow costs will also weigh on profitability, though the Energy sector will be a tailwind for aggregate index margins. For index investors, the largest constituents will also be key: The 10 largest S&P 500 companies account for 19% of aggregate earnings, and net margins for these companies are projected to rise by a median of 30 bp in 2023. As a result, index margin and EPS estimates face less downside risk than those for the median stock. Our base case forecast, assuming no recession, shows aggregate S&P 500 net profit margins remaining flat in 2023. Consensus estimates embed margin expansion of 30 bp.

Downside risk to earnings estimates increases the value of earnings safety. We continue to recommend investors focus on stocks where they can be relatively confident in the forward trajectory of earnings, including firms with stable growth and the Health Care sector, which has grown earnings in each of the last several recessions.