1-in-5 Aussie mortgage holders face stress as interest rates soar

Roy Morgan has modelled the direct impact of the existing 0.75% lift in the Official Cash Rate (OCR) in May and June on Australian mortgage holders, as well as the expected interest rate increases of 0.5% during each of the next two months.

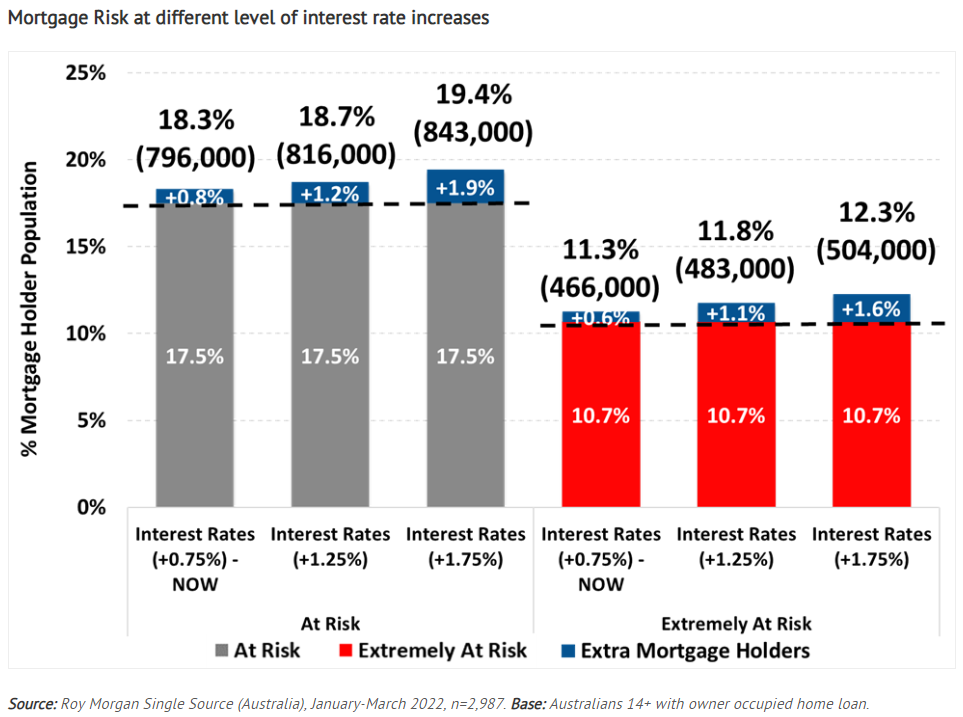

The interest rate increases already made by the RBA mean that 18.3% of mortgage holders, 796,000, would now be classified as ‘At Risk’ – an increase of 34,000 on the original figure of 762,000 (17.5%).

If the RBA increases interest rates by 0.5% in each of the next two months this would mean 19.4% of mortgage holders, 843,000, would then be classified as ‘At Risk’ – an increase of 81,000. This would be the most mortgage holders classified as ‘At Risk’ since the March quarter 2021 just over a year ago.

Roy Morgan considers the risk of ‘mortgage stress’ among Mortgage holders in two ways:

- Mortgage holders are considered ‘At Risk’ if their mortgage repayments are greater than a certain percentage of household income – depending on income and spending.

- Mortgage holders are considered ‘Extremely at Risk’ if even the ‘interest only’ is over a certain proportion of household income.

Commenting on the results, Roy Morgan CEO Michele Levine noted that mortgage stress has been at record lows amid all-time low interest rates and financial support from the Government and banks that protected those with home loans. But that looks set to change as interest rates rise:

“If the RBA does go through with these interest rate increases in the next two months there would be a further increase in the number of mortgage holders considered ‘At Risk’ to nearly one-in-five (19.4%) or 843,000 (an increase of 81,000). This would be the highest number of ‘At Risk’ mortgage holders since early 2021 – and with the prospect of further interest rate increases to come…

“These figures suggest that as long as employment levels remain strong the number of mortgage holders considered ‘At Risk’ will not spike alarmingly over the next few months as interest rates are increased from the record low levels experienced during the last two years.

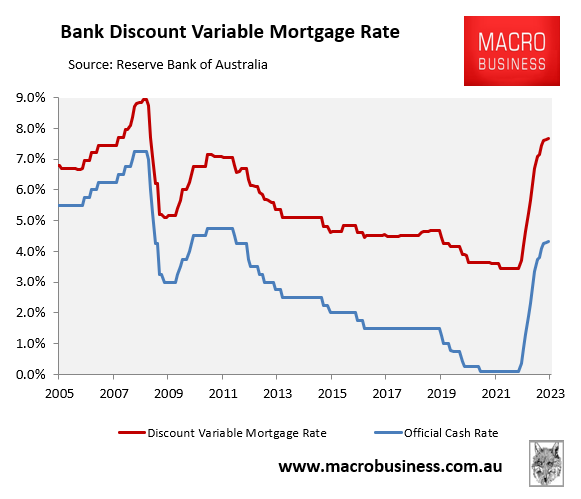

An OCR of 1.85% is manageable. But an OCR of 4.3% by May 2023- as predicted by financial markets – would see mortgage rates more than double from their pandemic low (to 7.7%) and would place enormous stress on borrowers.

Australian mortgage rates to double under futures market’s forecast.

Monthly principal and interest mortgage repayments would rise by around 50%, which would also smash household consumption – the Australian economy’s biggest driver.

Given Australia has the second highest household debt loads in the world, and the majority of borrowers are on variable rate mortgages, we are more sensitive to interest rate changes than anywhere else.