China is reopening Shanghai and lifting some other lockdowns:

Shanghai will let residents in low-risk areas leave and enter their compounds as the financial hub takes its biggest steps toward lifting a two-month strict lockdown.

The city will resume taxi and ride hailing services while allowing cars onto the road in low-risk areas, the municipal government said in a statement on Monday. Shanghai will also reopen bus, subway and ferry services in an orderly manner from June 1.

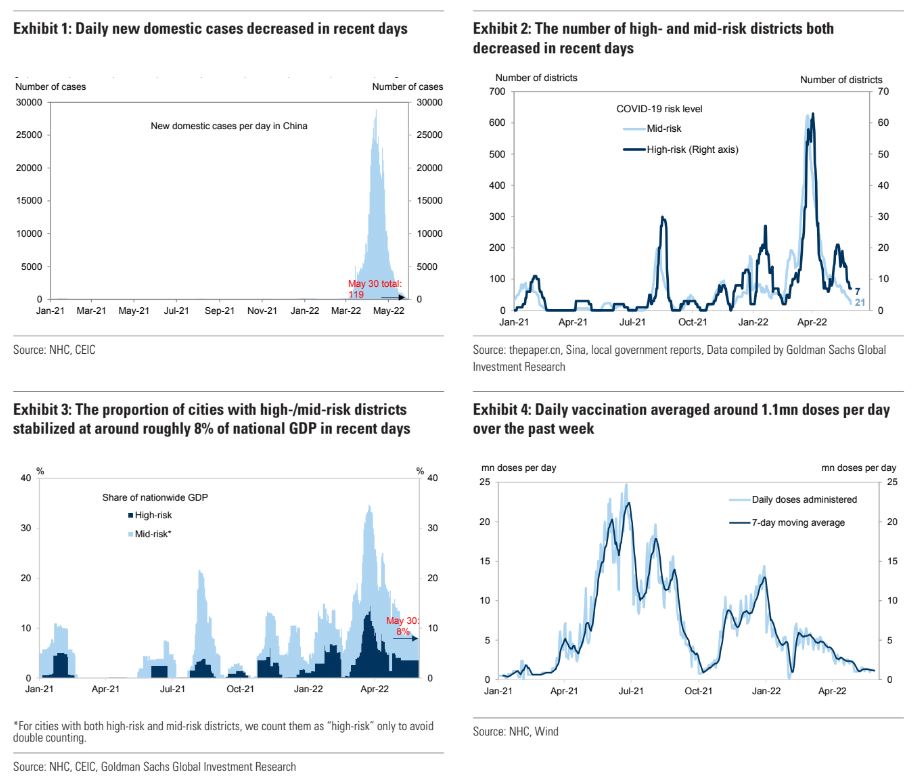

I guess we could say that OMICRON is under control for now but not for long as everything reopens:

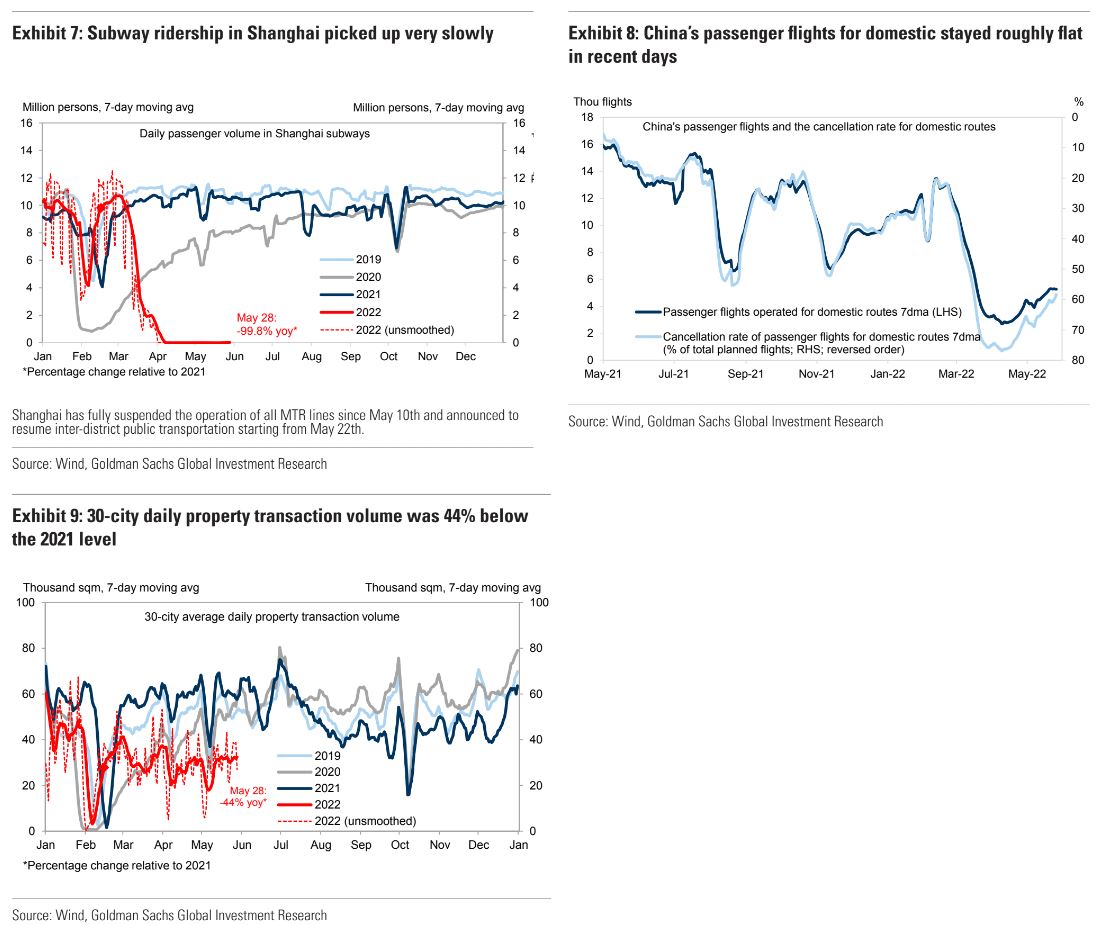

And mobility bounces back:

It appears property sales are off their very worst but you’d be hard-pressed to describe that as a recovery.

According to Goldman, nobody in China is expecting much on that front:

As the Covid situation appears to be improving in China (declining total cases, Shanghai and Beijing gradually relaxing restrictions), we talked with our local clients here in Beijing (still through online meetings) over the past week, and summarize their latest views on the economy and policies. These clients range from asset managers in insurance companies/banks to private equity funds and hedge funds.

1. Growth expectations

Local clients in general hold a bearish view on the economy. While local clients agree activity growth should rebound in June/Q3, barring another major wave of Covid resurgence, they question the magnitude of the growth rebound even after the relaxation of Covid related controls. Local clients worry about scarring effects from anti-pandemic measures and growth slowdown, which include heightened uncertainties around economic and policy outlook, a higher number of bankruptcies and elevated unemployment rates.

In addition, during our conversations, local clients pointed out the clear downward trend of underlying growth momentum – for example the sluggish consumption due to weak income growth and labor market stress and slowing export growth amid weakening global goods demand. While local clients express little doubt on the expected strong rebound of infrastructure investment, they view it as not being enough to offset growth downward pressures. According to local clients, the weak underlying growth stood in contrast with early 2020 during the initial onset of the Covid pandemic: underlying growth momentum was strong back then and Covid control appeared to be the only obstacle to economic growth.

2. Feedback on recent policy easing

Despite reiteration from policymakers on stepping up policy support, local clients think recent easing measures would only bring marginal support to the economy, implying more easing is probably needed to lift sentiment.

Local clients have mixed views on whether the property market could stabilize on the back of policy easing. Arguments against “stabilization” include the potentially much smaller investment demand after policymakers’ repeated guidance that “housing is for living, not for speculation”, as well as the worry on the sustainability of property policy easing, especially in top-tier cities, should property prices start to rise again.

Local clients did not push back on our view that the “Dynamic Zero Covid” policy stance would be maintained till Q2 2023, though they generally preferred not to discuss this topic (in only 1 out of the 10+ client meetings we had did local clients discuss the “Dynamic Zero Covid” policy stance with us), potentially due to its political sensitivity.

Local clients agree with our view that fiscal policy easing would be the main policy lever this year. Among local clients, widely expected additional easing measures include central government special bond issuance, front-loading of government bond issuance from 2023 to 2H 2022, and consumption coupons. A number of local clients also mentioned the possibility of PSL (“Pledged Supplementary Lending”, which has not been used much since 2019) as additional monetary policy support. On the back of weak sentiment and lack of signs on growth stabilization, local clients agree with our view that it might be too early to pay China rates now.

3. Other risks

A few local clients asked about potential spillover effects from global inflation, and together with unfavorable base effect in China, whether this would suggest inflationary pressure being a bigger constraint for China’s policy easing over the next few quarters. US recession risk remains a key concern for local clients, and local clients appear to have higher expectations for the US lowering additional tariffs on Chinese goods on the back of elevated inflationary pressures in the US. Foreign investors’ sentiment towards RMB assets (including bonds and equities) remains a popular discussion topic during our onshore marketing.

In sum, the most frequently asked questions from local clients include whether policymakers could restore corporate and consumer confidence, and relatedly, the magnitude of a potential growth rebound even after the relaxation of Covid control.

Similar to previous months, global growth uncertainty such as US recession risk remains a key concern for local clients. These topics also featured prominently in our recent conversations with offshore clients. However, offshore clients seem to have higher confidence relative to local clients that, should the Covid situation continue to improve from here, we could see growth rebound and even pent-up household demand in late Q2/Q3. Hence, offshore clients appear slightly more optimistic on the economic outlook, though both local and offshore clients expect the full-year GDP growth to be materially below the official government growth target of “around 5.5%” this year.

That seems about right. Get set for the Chinese economic unrecovery as OMICRON refuses to go away, property doesn’t rebound and an export shock arrives from the US in due course.