A report released this week by think tank Per Capita shows the rate of Australian home ownership is declining rapidly, especially among those aged under 40.

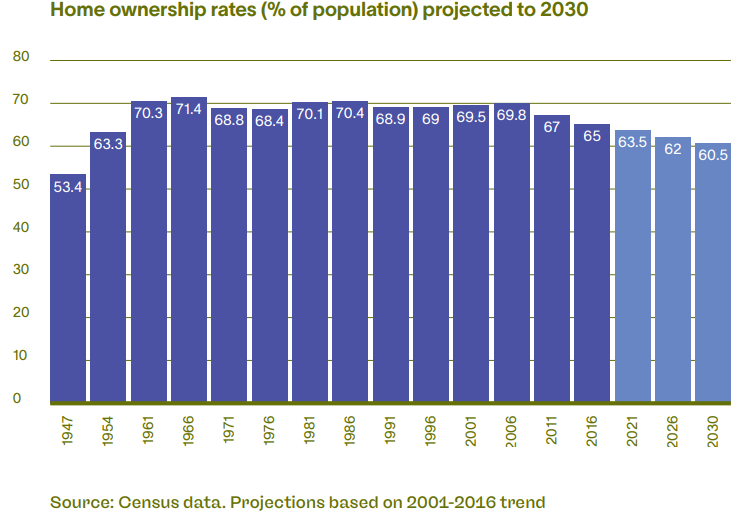

On current trends, Per Capita estimates that fewer than 55% of people born after 1990 will own a house by the age of 40, compared to a historical high of 72%:

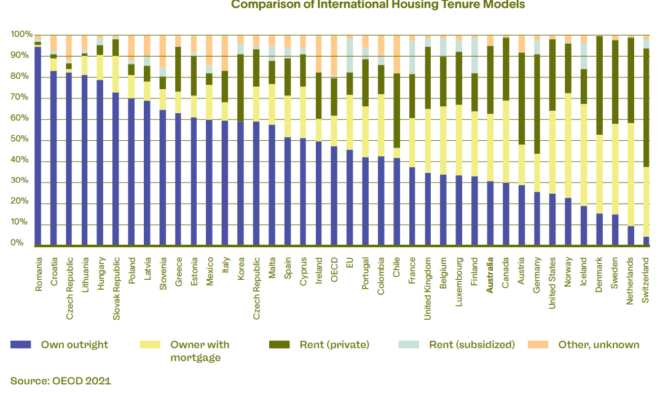

The truth is, secure housing in Australia is increasingly out of reach for a growing proportion of the population – arguably more so than in any comparable country. In fact, Australia is now behind the United Kingdom when it comes to outright home-ownership, and has fallen behind the US for owner-occupied mortgaged households. The proportion of households living in a home they own outright or with a mortgage in Australia is a full 13% below the OECD average, and falling…

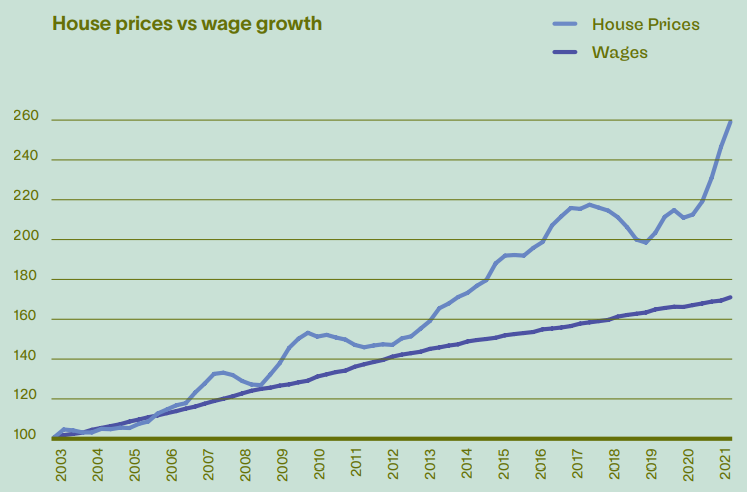

Since the 1990s, house prices have risen from 2.5 times annual household income, to over six times today. Australian households are among the most indebted in the world, mainly due to rising mortgage commitments. Social housing stocks are in decline, with waiting times extending to over five years in some areas, while the private rental market remains one of the least regulated in the world, lacking even a nationally agreed standard for a habitable dwelling…

In recent decades, the twin processes of financialisaton and deregulation have dehumanised the housing market, turning homes into commodified assets. Successive government policy changes have encouraged those with the financial means to invest in residential property, with the promise of rapid returns that are subsidised by the tax-payer…

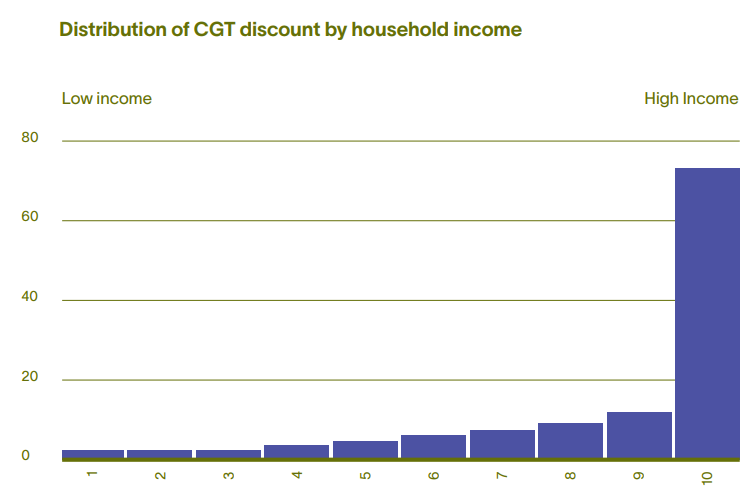

Government policy decisions to tax wages from working people much more heavily than unearned incomes from rising property prices, and concessions granted to existing property owners, have, over the last 25 years, fuelled an exceptional and damaging explosion in property prices. Until recently, this was concentrated in Australia’s capital cities, but the impact of COVID19 and the ensuing changes in workplace practice, asset prices and lifestyle have seen the escalation of housing prices extend to our regional cities and towns.

At the same time as government policies have excessively stimulated property price…

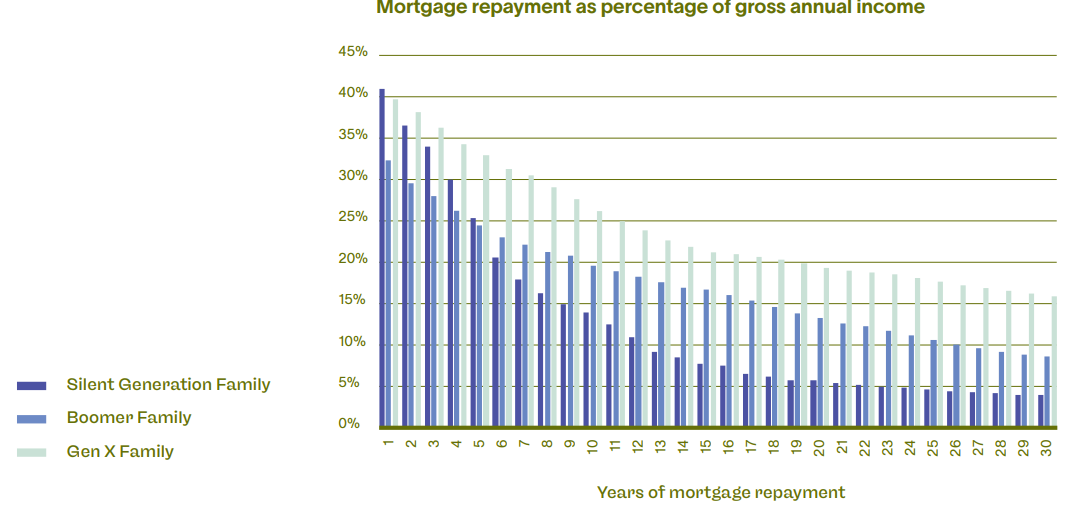

The cost of housing as a proportion of an individuals’ income has been increasing over the past 50 years. Taking three generations as examples, and comparing median mortgage costs to median wages, we show that the lifetime cost of a home purchase shows a quite different picture to that provided by just comparing single year mortgage costs…

We estimate the Gen X family is paying $1425 per month on their mortgage in 2021. If they were on the same repayment trajectory as the Boomer family their monthly bill would be $910, while if they were on the Silent Generation trajectory it would be just $440 a month.

For the individual family, this is a huge loss of income – almost $1,000 a month – that would be far better directed toward education, health or day-to-day living expenses. For the nation, it represents a significant constraint on household consumption, which accounts for more than half of Australia’s

economic activity…

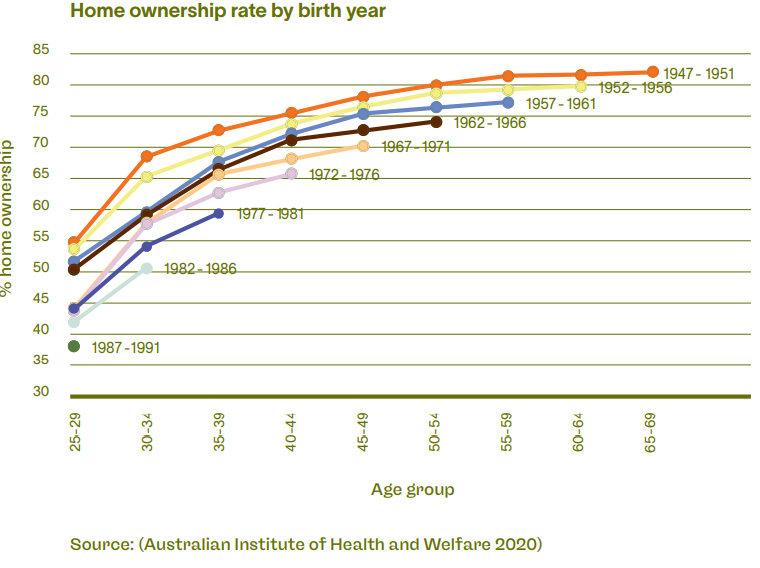

Perhaps the single most distressing and socially challenging contemporary housing issue is the decline in affordability between generations.

People born between 1947-1951 have experienced historically high levels of home ownership, from their 20s, through to their 70s. Following the 1947-51 birth cohort, there has been a decline of around 1.8-2.5% of home ownership every 5 years. For example, 37.4% of people born between 1987-1991 own a home when aged 25-29, down from 54.2% for people born between 1947-51. This trend is consistent across sub-60 age groups.

Based on the current trend we can produce forecasts as to ownership rates for different age groups. It appears that the number of people entering retirement who own their home outright will fall by 5.7% from 81.3% to 75.6% over the next ten years. It is likely that this cohort will experience higher rates of mortgage stress with a higher cost of living associated with paying off the mortgage…

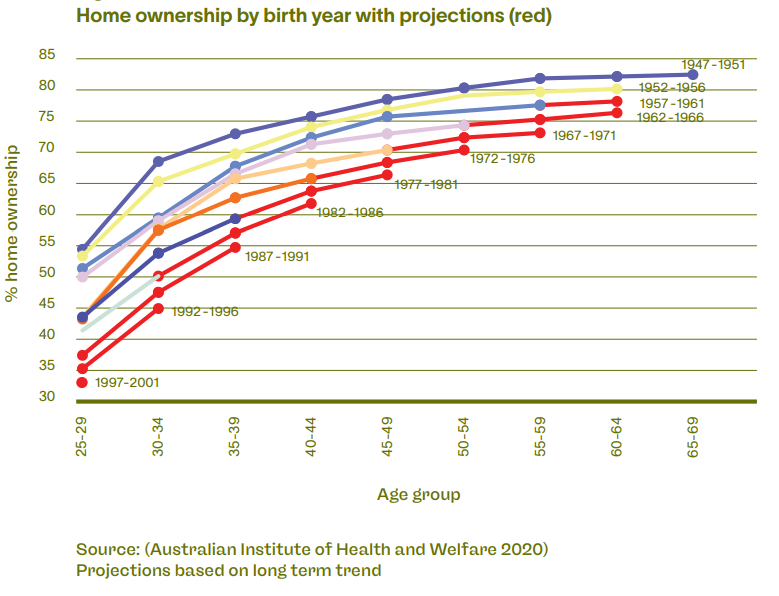

For people born between 1982 and 1991 we can expect, on current trends, to see around 55% owning a home before they are 40, 10% lower than their counterparts born between 1962 and 1971…

Some commentators argue that increasing home values increases overall national wealth. We find that the evidence points in the opposite direction, with money tied up in the housing market doing very little to stimulate more productive parts of the economy. What is worse, increasing house prices redistribute wealth upwards: as Reserve Bank Governor Philip Lowe once said, ‘…it is arguable that the main impact of higher land prices is not really to increase our national wealth, but to change the distribution of that wealth”…

The rapid escalation of property prices in Australia, particularly over the last 20 years, is the result of myriad intersecting factors, affecting both the supply and demand for new homes. Most of these factors are directly influenced by government policy settings…

The crisis in housing affordability in Australia represents a failure of public policy on a number of levels. Federal, state and local governments share the blame for an unsustainable decline in the availability, accessibility and affordability of housing across the nation.

What a fantastic report. Despite decades of demand-side policies like first home owner grants, home ownership has fallen. This suggests that the latest Lib/Lab home buyer bribes rolled-out over the election campaign will make the affordability and home ownership situation even worse.

Advertisement

Per Capita’s statements around Australia’s national wealth are also spot on. Having one of the world’s most expensive housing markets is a curse, not a blessing.

Expensive housing punishes those who have recently entered, or are yet to enter, the housing market. These people are either consigned to a life of debt slavery repaying mega-mortgages, or miss-out altogether.

Would Australia as a whole really be worse-off if the median dwelling price was $365,000 instead of $730,000, mortgage debt was 70% of disposable incomes instead of 140%, and the banking sector was smaller and less profitable?

Advertisement

The answer is a resounding no. Australian households would benefit from lower debt loads, whereas the broader economy would benefit from the productivity-boosting effects of lower land costs, increased business lending (investment), and a more balanced economy.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.