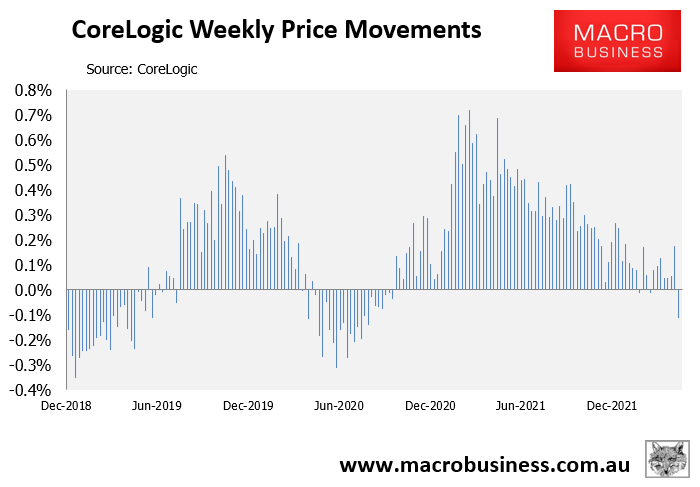

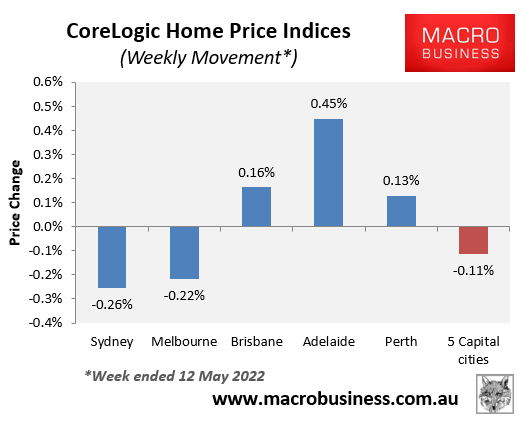

CoreLogic’s daily dwelling values index, which measures price changes across the five main capital city markets, declined by 0.11% in the week ended 12 May:

The decline was driven by Sydney (-0.26%) and Melbourne (-0.22%), which both recorded heavy price falls. By contrast, the other major capitals each recorded price rises, with Adelaide leading:

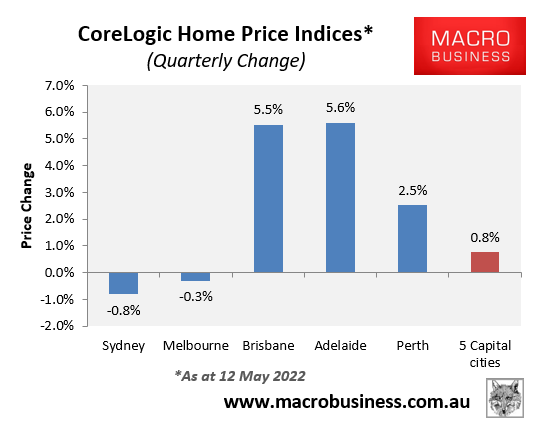

Over the quarter, Sydney (-0.8%) and Melbourne (-0.3%) both recorded falling dwelling values, but were more than offset by solid-to-strong rises across the other major capitals, thereby driving values up 0.8% across the combined 5-city level:

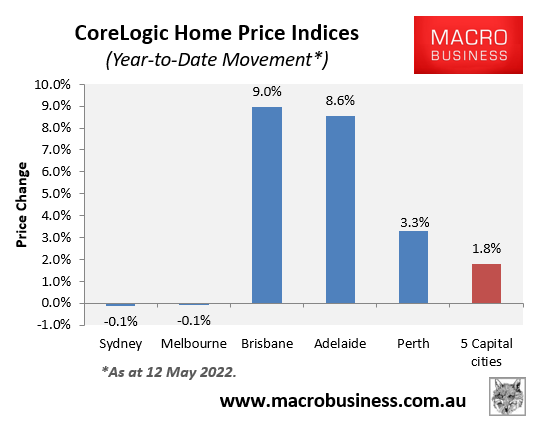

Similarly, since the beginning of the year Sydney and Melbourne dwelling values have fallen by 0.1%, more than offset by strong growth across Brisbane (+9.0%) and Adelaide (+8.6%), and solid growth in Perth (+3.3%):

With interest rates now rising, and Sydney and Melbourne having the nation’s most expensive homes and indebted households, both cities should experience accelerating price falls in the months ahead.

How fast and far prices fall will depend on how aggressively the Reserve Bank hikes interest rates.