BofA via ZH.

—

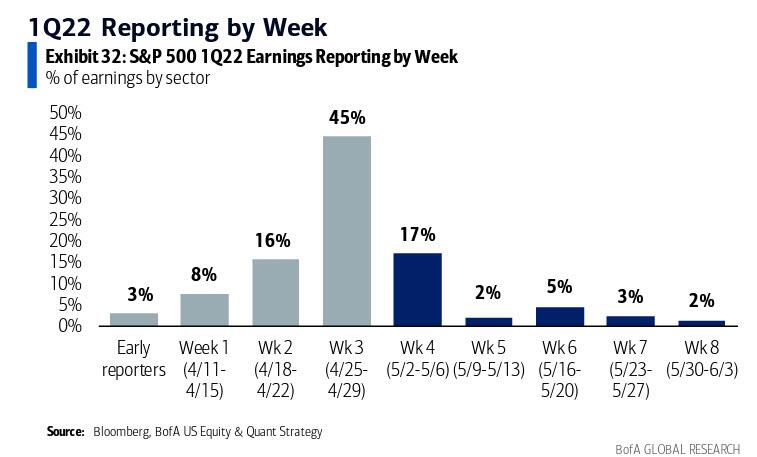

Bank of America’s Savita Subramanian writes in her weekly Eranings Tracker now that week 3 is in the history books…

BofA via ZH.

—

Bank of America’s Savita Subramanian writes in her weekly Eranings Tracker now that week 3 is in the history books…

The full text of this article is available to MacroBusiness subscribers