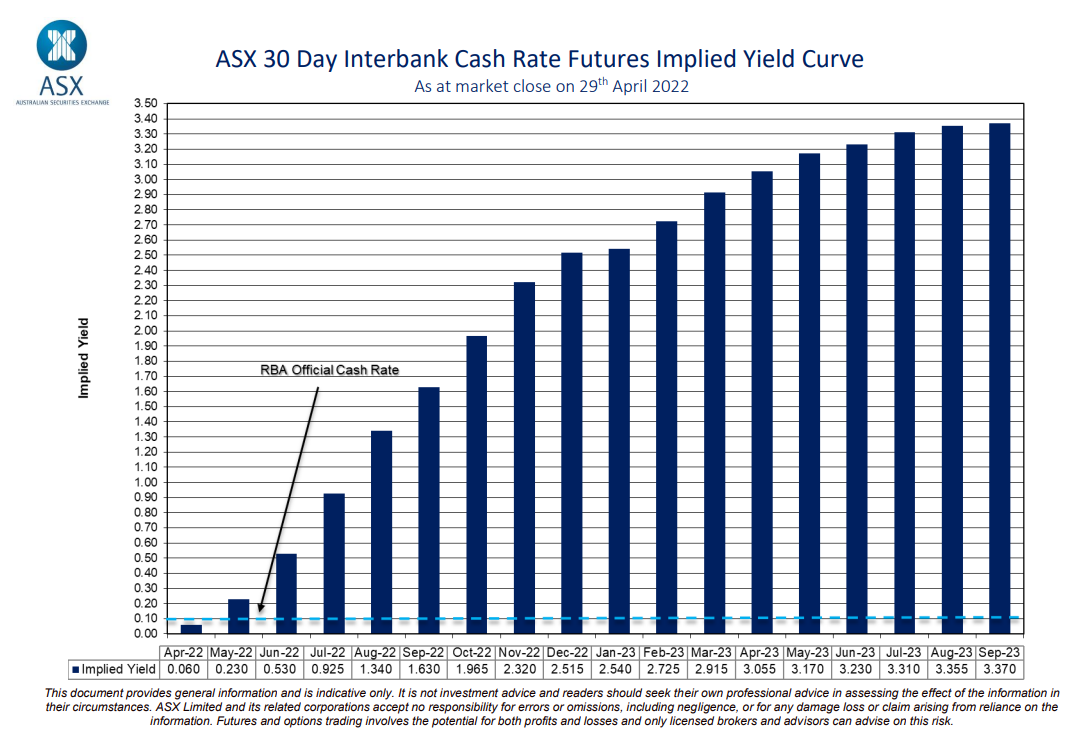

The latest Australian interest rate forecast from the futures market predicts the Reserve Bank of Australia (RBA) will hike the cash rate from its current record low level of 0.10% to 2.5% by year’s end and to around 3.4% by September 2023:

Futures markets are tipping nine interest rate hikes in just seven months.

If the market’s prediction comes to fruition, then Australians would experience the equivalent of around nine 0.25% interest rate hikes in only seven months, with more to come in 2023.

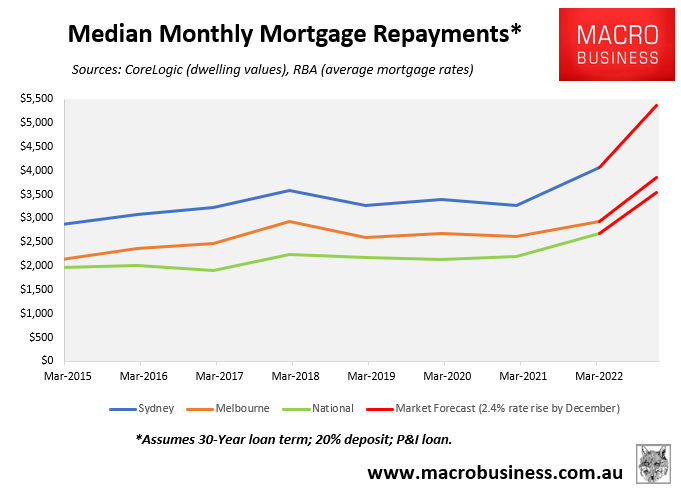

Assuming these forecast increases in the RBA cash rate were passed on in full to Australian mortgage holders, then by the end of 2022, average Australian mortgage repayments would soar by around one-third above current levels.

This would add around $850 to average monthly mortgage repayments on the median priced Australian home and nearly $1,300 a month in Sydney:

Median monthly mortgage repayments would rise by one-third by end-2022.

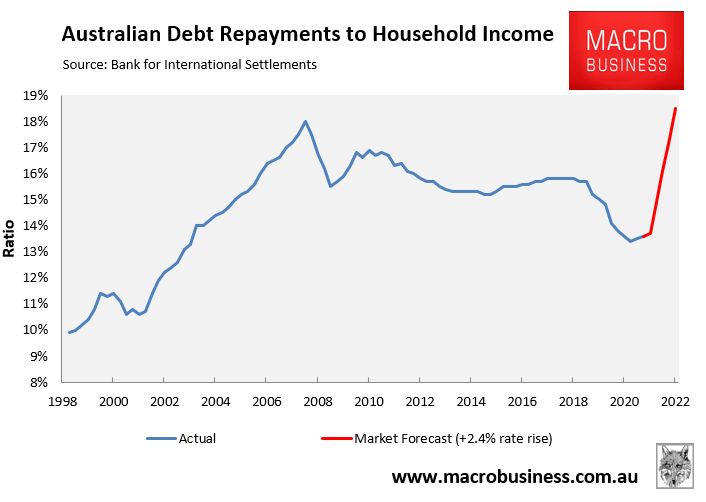

Australia’s Debt Servicing Ratio (DSR) – defined as the percentage of household disposable income going towards principal and interest debt repayments – would also surpass its Global Financial Crisis peak and hit a record high by year’s end:

Australia’s debt service ratio would also rise to a record high by end-2022.

Obviously, we consider the market’s interest rate forecasts to be delusional, given rate rises of this speed and magnitude would very likely crash house prices and throw the Australian economy into an unnecessary and unwanted recession.

Just be glad the interest rate lever rests with the RBA, not the futures markets, given the RBA is likely to take a more measured and responsible approach toward interest rates.