Yesterday’s ANZ-Roy Morgan consumer confidence survey posted a massive 6.0% fall, driven by a 9.6% decline amongst people ‘paying off their home loan’, who are growing increasing concerned about rising interest rates.

The concern is greatest amongst the army of households that took out jumbo-sized mortgages in 2021 at record low rates below 2.5%:

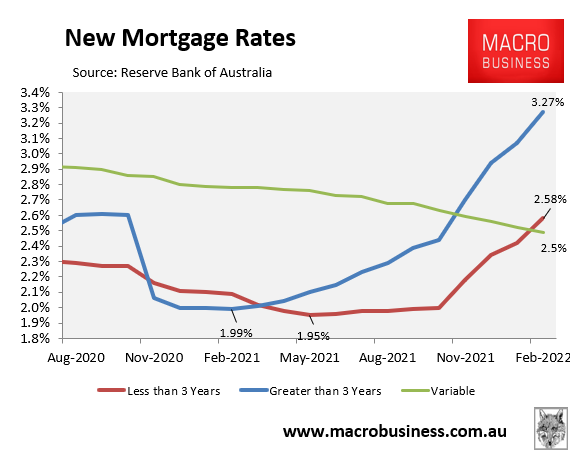

Many households took out mortgages at rates below 2.5% in 2021.

Many of these borrowers are now worried their mortgage repayments could double as the RBA seeks to ‘normalise’ interest rates:

Robyn Lambropoulos is starting to worry about rising interest rates. Ms Lambropoulos and her husband have just welcomed a new baby… she’s bracing for interest rates to rise from their record lows.

“Based on my calculations, I think our mortgage repayments will double as a result,” says Ms Lambropoulos…

Jess, who didn’t want to give her last name, is in a similar situation after also giving birth to a new baby…

“When we took out the loan two years ago, we had a 2.2 per cent interest rate and our repayments were quite manageable, but now we’ll have to consider the repayments if interest rates go to 3.5 to 4 per cent,” says Jess.

“The repayments at 4 per cent on $1.1 million are more than double what we were paying previously, and we’re not sure where we’re going to get that sort of extra money from”…

On a $1 million mortgage, repayments will go up from around $19,000 at a 1.9 per cent interest rate to $35,000 to $40,000 a year as rates head to 3.5 per cent to 4 per cent.

Recall that most bank economists are tipping that interest rates will rise by more than 2% from their pandemic low, whereas financial markets are tipping a heftier increase of more than 3%.

For households that borrowed to the hilt at rock bottom rates near the peak of the market, it will be a bitter pill to swallow. Some will be forced to sell, while others will be plunged into negative equity as house prices plunge.

The rate rise apocalypse is about to begin.