Highest interest rates in galaxy to pop Australian property bubble

Advertisement

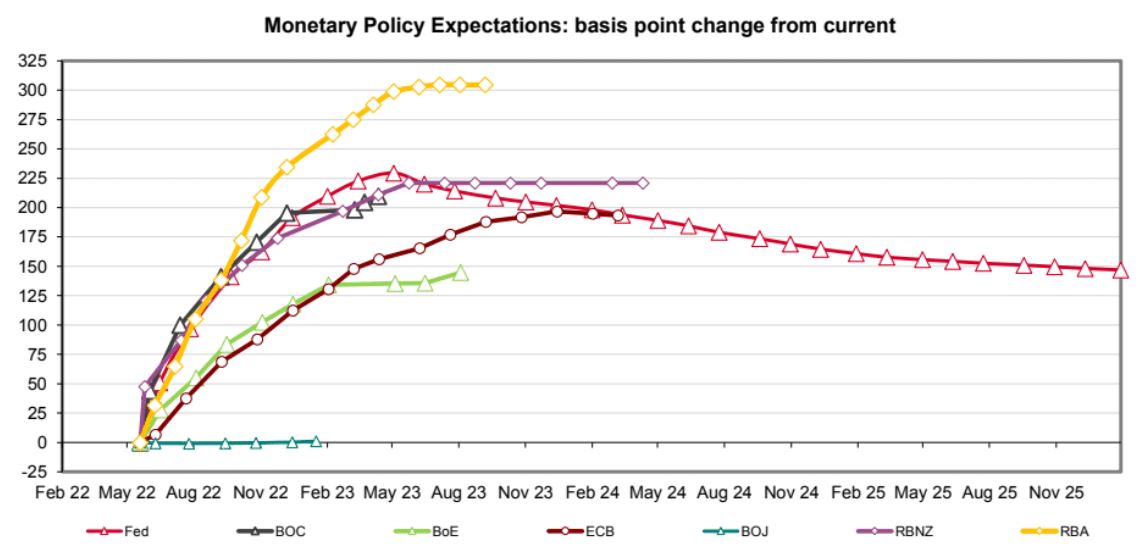

That’s what is still coming according to financial markets. Even as other long-end interest rates around the world have started to decline as markets price in an economic downturn from the paltry tightening we’ve seen to date, Aussie interest rate forwards have held onto all of their gains:

In short, markets are forecasting Australia is headed for the highest interest rates in the developed galaxy by mid-2023.

These interest rates will trigger the following in my view:

Advertisement

- The bursting of the Australian property price bubble. with prices down 30-50%

- An AUD back to parity.

- A deep recession and unemployment soaring above 10%.

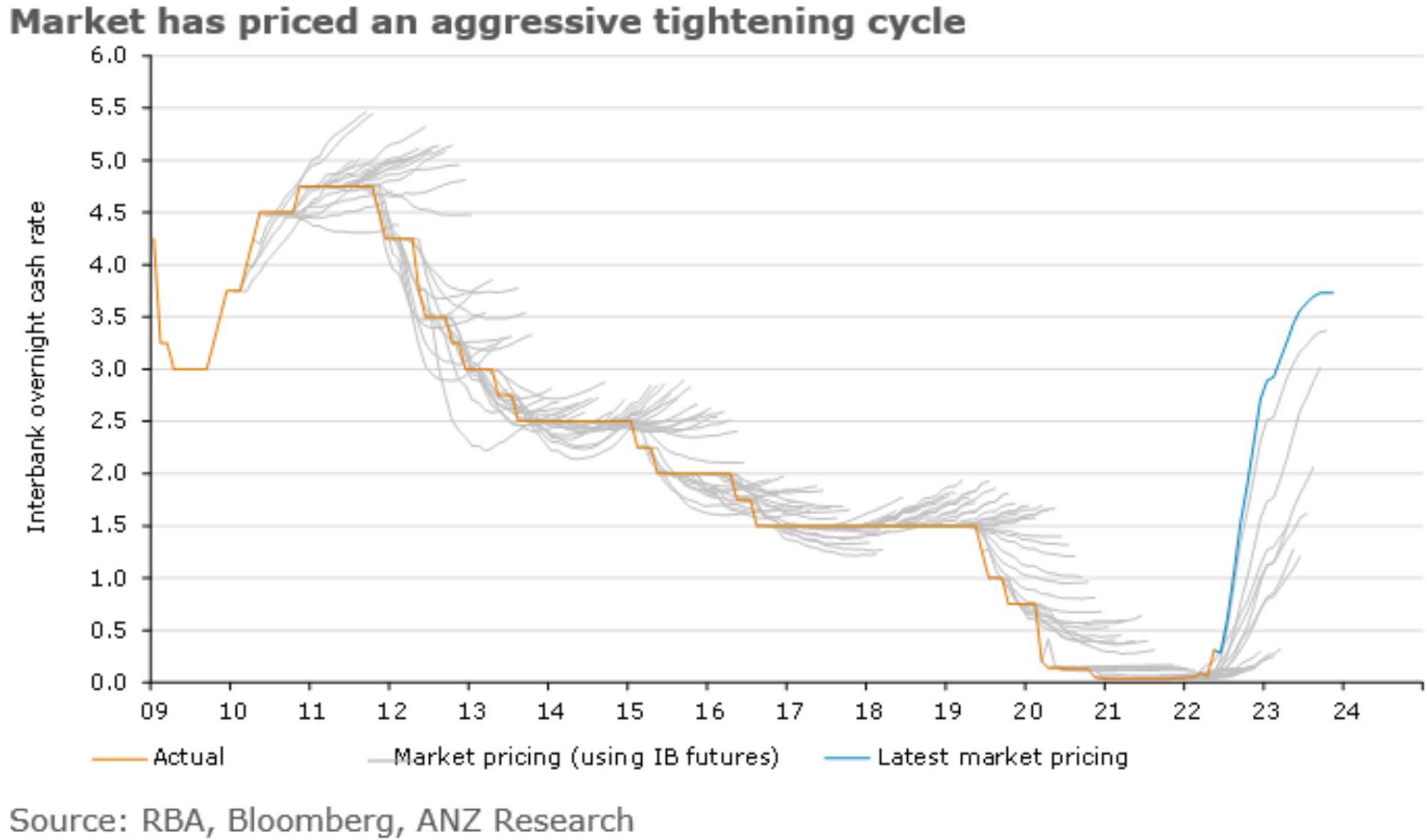

It is no wonder that markets have such a terrible forecasting record for Aussie rates because they have NO IDEA what they are pricing today:

Advertisement

It is, in a word, ludicrous.

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Advertisement