Goldman explores the question. It looks increasingly likely that the long-bond yields have peaked a US growth fades away. But whether the Fed can stop is another question. I still think it needs to break the commodity complex before it pivots.

—

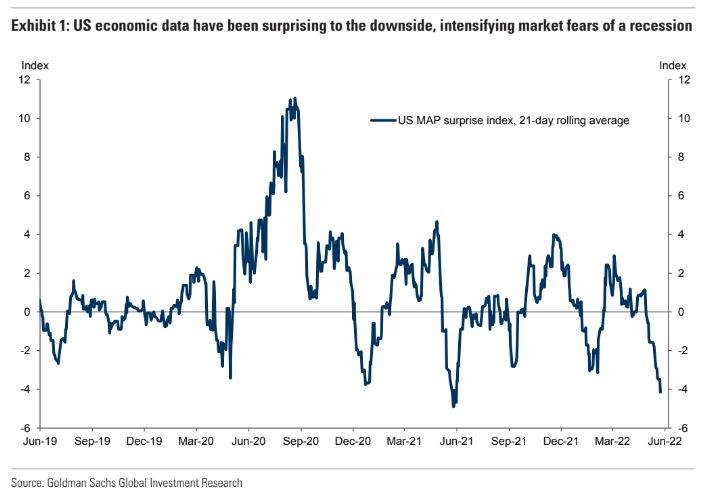

1. From tightening to growth fear to peak inflation. A few weeks ago, we argued that the pressure to tighten financial conditions will define market dynamics— keeping both equities and rates under pressure—as long as the market believes that inflation is still too high and that the Fed needs to slow growth further to deal with that. Since then, financial conditions have tightened further and Fed rhetoric has remained hawkish in the wake of another high core CPI print. With growth worries increasing, equities and credit have driven that tightening, with longer-dated yields moving more clearly off their peaks. There are two main ways for the market to move beyond this dynamic. The first is if the market moves towards fear of outright recession. In that case, risk assets would likely remain under pressure but the market would begin to push yields more clearly lower even with sticky inflation. The second, more benign route is if the inflation picture improves more clearly and the market judges that the Fed’s tightening is doing its work. This would likely provide relief to both bonds and equities, at least in the short term. The market has been firmly focused on rising recession risk lately, fueled by deterioration in the US data in particular. But hints of inflation improvement may be reinforced by Friday’s PCE release and perhaps the upcoming JOLTs and payrolls release. If the “peak inflation” narrative gathers steam, it could provide some relief from the relentless pressure for tighter policy. Although we doubt that this is the end of the road for the tightening dynamic yet, we do think the picture for rate shorts has become more complicated here and see value in exploring upside optionality in equities and downside optionality in the USD in the weeks ahead, alongside positive carry risk-neutral FX trades.