The Reserve Bank of New Zealand (RBNZ) has released data on mortgage finance commitments, which shows that buyer demand is collapsing fast.

In April 2022, only 13,939 mortgages were issued, which is the third lowest monthly total since the RBNZ began producing this series in 2014.

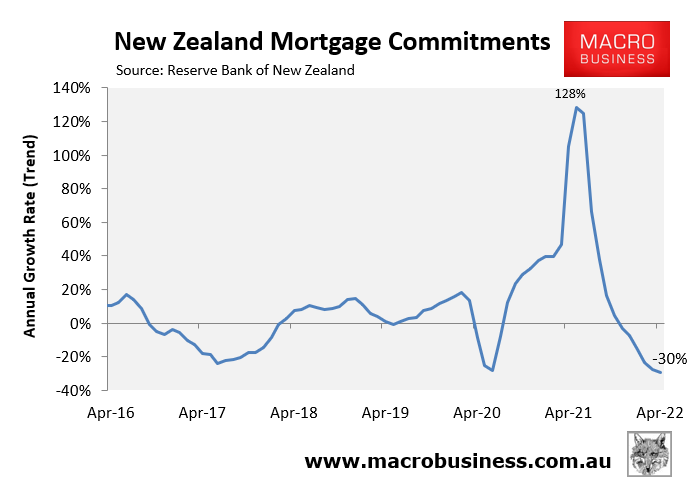

In dollar terms, mortgage commitments collapsed 30% in the year to April 2022 – a sharp turnaround from the 128% annual growth recorded in May 2021:

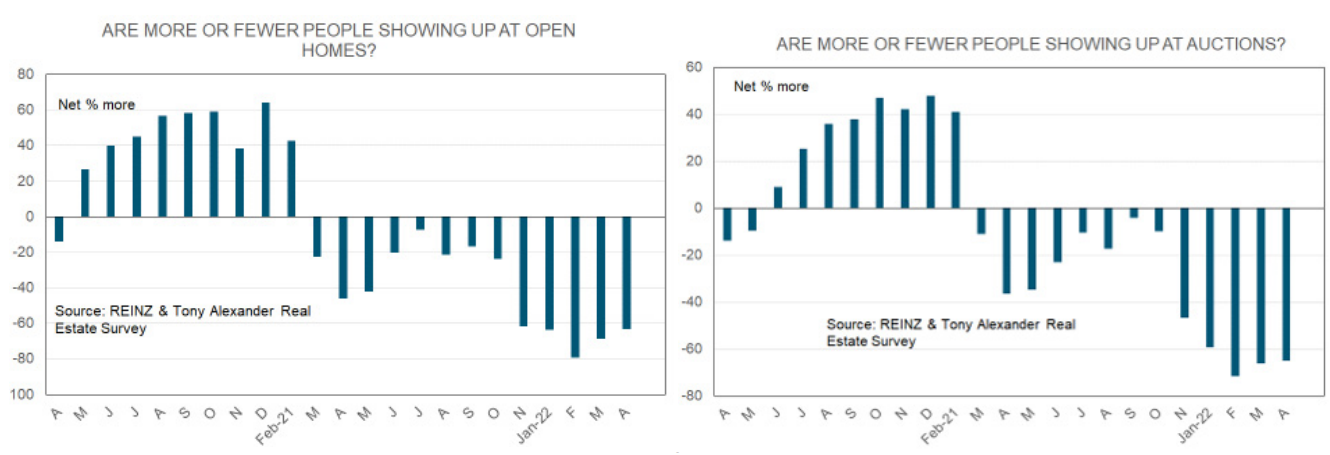

Separate survey data released this month by the Real Estate Institute of New Zealand (REINZ) also showed that attendance at auctions and open homes has collapsed:

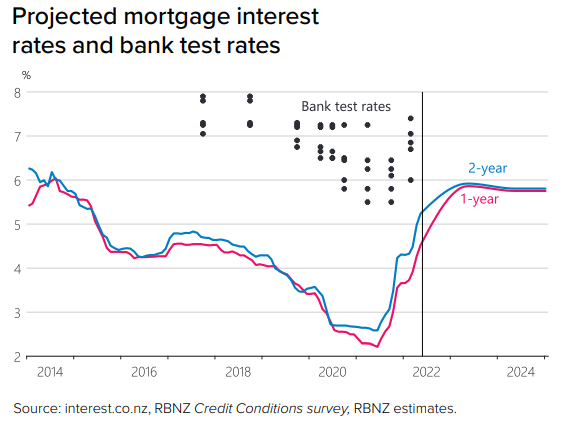

This slump in buyer demand follows 1.75% of interest rate hikes from the RBNZ since October 2021, which has lifted the official cash rate (OCR) to 2.0%.

There is worse to come, too, with the RBNZ’s ‘forward track’ guidance showing the OCR at 2.7% by September of this year and 3.4% by December, before peaking at 3.9% in June 2023.

These rate hikes are projected by the RBNZ to more than double mortgage rates from their pandemic lows to around 6%:

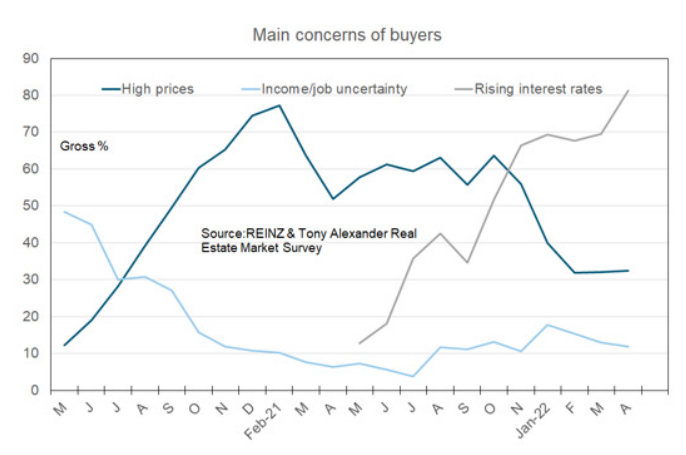

This month’s REINZ survey also showed that rising interest rates are by far the number one concern of home buyers:

Therefore, we should logically expect home buyer demand to collapse further as interest rates soar.

How bad it gets will depend on how aggressively the RBNZ tightens monetary policy. If the RBNZ follows through with its forward guidance, then New Zealand’s housing market faces a serious correction or crash.