The smartest guys in the room that have survived the last six months best are more not less bearish. BofA’s Michael Hartnett, who has been the maestro conductor of this crash, leads us off:

The Way We Were: “Millennials are quitting jobs to become crypto day traders”, USAToday, Aug 12th 2021.

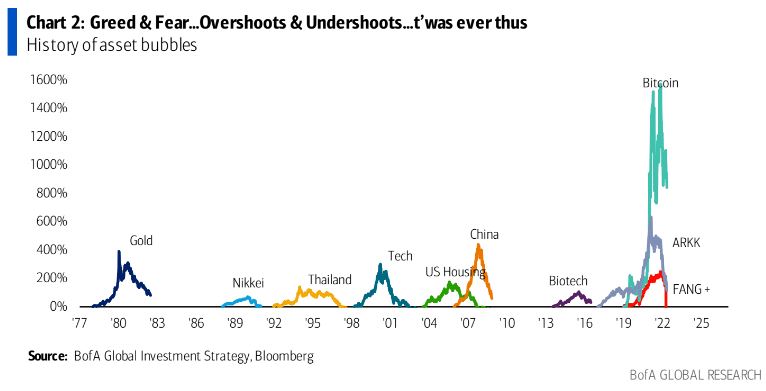

The Biggest Picture: crash in crypto (Chart2)/speculative tech now rivals internet bubble crash (Nasdaq-73% peak-to-trough) & GFC (banks-78%); trading pattern of post-bubble assets always furious bear rallies amidst dead sideways trading range for couple of years.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.