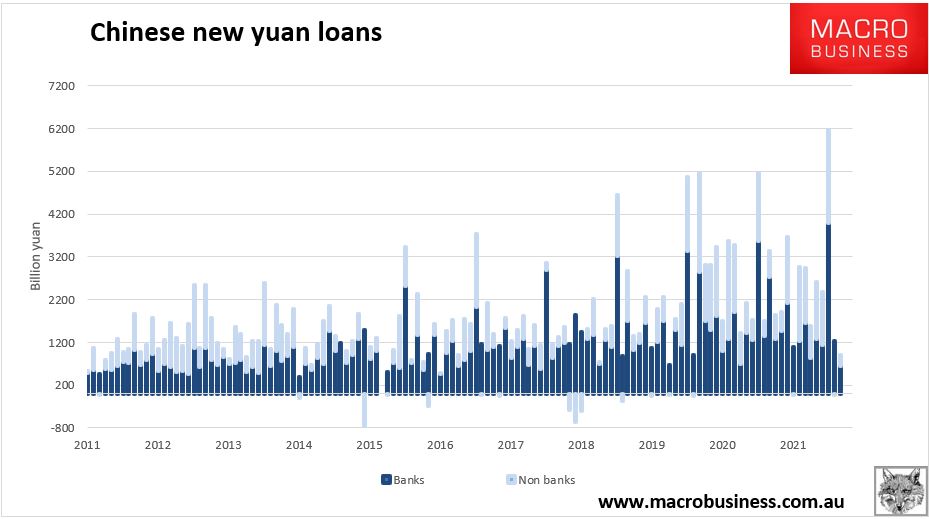

On the weekend we also got April credit data. Much of what I read tried to put a brave face on it but the numbers are a disaster. Total social financing came in at a paltry 910bn yuan, less than half expectations. Bank lending was a terrible at 645tr yuan:

Advertisement

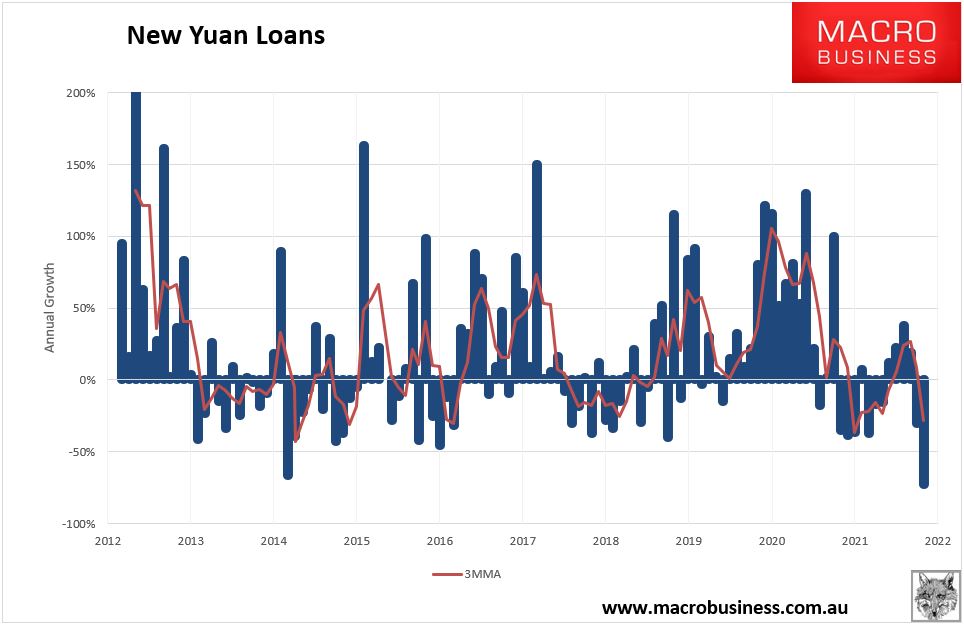

As China tries to stimulate, credit fell 73% year on year for April and the 3MMA has collapsed to -28%:

Advertisement

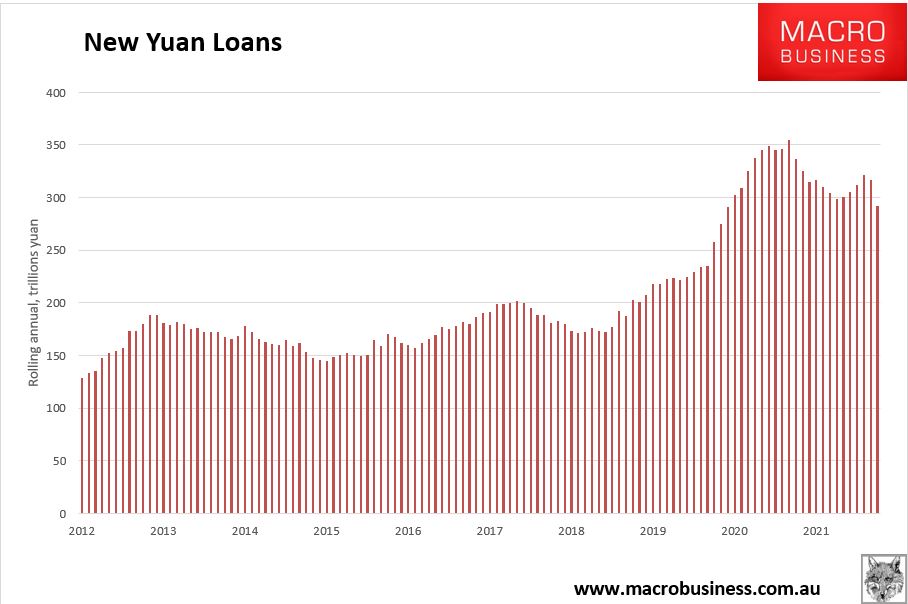

Rolling annual credit flow is being punished:

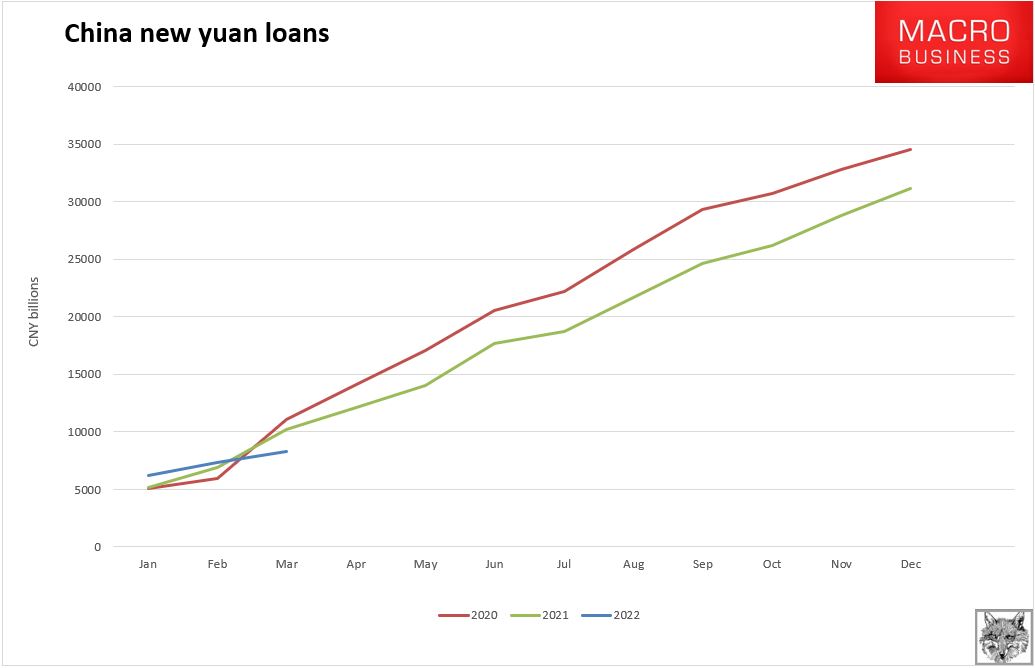

Year to date credit flow is on track for nothing good:

Advertisement

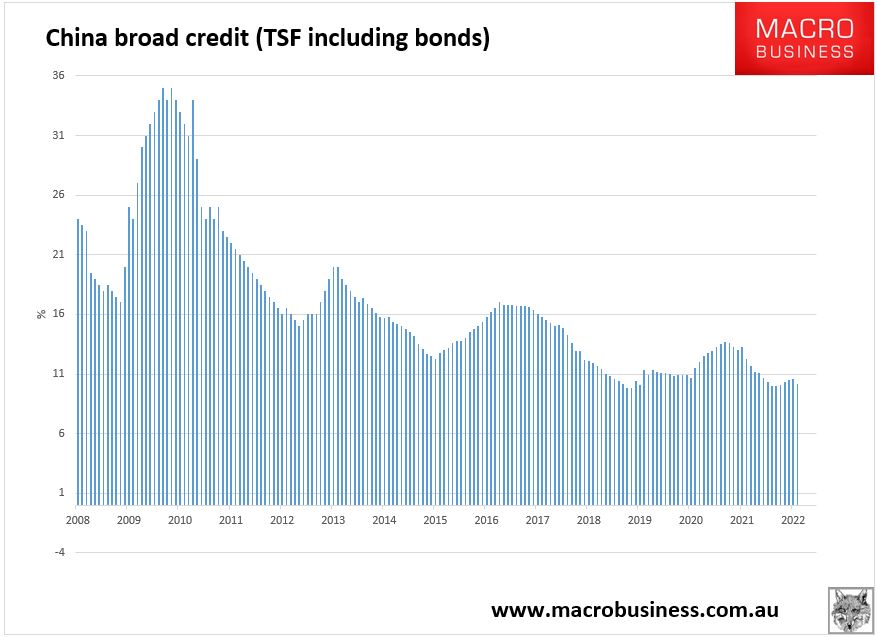

And the growth in stock of loans shrank to 10.2%:

Under the bonnet, it does not get any better. Goldman:

Advertisement

April total social financing and RMB loans came in much below market expectations, while M2 growth accelerated and was above market expectations on the back of the RRR cut and more expansionary fiscal policy stance. Composition of RMB loans suggests corporate loan growth decelerated and household loans stock declined in April (after adjusting for seasonality). PBOC cited weak credit demand due to Covidresurgence as one main reason behind the weak RMB loans and TSF data. Medium to long term loan growth was still much slower than short term loans (such as bill financing) growth, and loans to the real economy was also much lower than overall RMB new loans (which include lending between financial institutions). These all implied very weak credit demand despite monetary policy easing.

April total social financing (TSF) was well below expectations after a strong acceleration in March. The sequential growth of TSF stock decelerated to 3.9% mom annualized sa in April, the slowest sequential growth in the past decade. Overall CNYloans growth also decelerated materially and grew 6.6% mom annualized sa from18.1% in March.

Among major TSF components, shadow banking credit continued to contract in Aprilat a much faster pace compared with March. After our adjustment for seasonality, trust, entrusted loans and undiscounted bankers’ acceptance bills fell RMB275bn in April, vs the RMB113bn contraction in March. Based on loans to different sectors, after our adjustment for seasonality, weakness in loan growth was broad-based, with the only exception being bill financing. Corporate mid-to-long term loan growth was 6% vs22.5% mom annualized in March. Corporate bill financing rose strongly by 102.4% mom annualized from 97.3% in March. On loans to households, total household loans declined by 1.7% month-over-month annualized, vs an expansion of 6.6% in March.PBOC changed their categorization of household loans and now focuses on usage of loans (housing related vs consumption related, for example), rather than by maturity. April data are thus not strictly comparable with March data. However, on a net basis, new mortgages were -61bn RMB in April, in comparison with household new medium to long term loans (which are mostly mortgages) of 492bn RMB in April 2021, or +374bnRMB in March 2022 (NSA basis). Government and corporate bond issuance also slowed in April.

We see three main reasons behind the weak loan and TSF data in April: 1) Covid resurgence and anti-pandemic measures weighed on activity growth and thus weakened credit demand; 2) property-related indicators have also deteriorated further despite policy easing, which contributed to the weak mortgage growth; 3)the largescale of VAT credit rebates starting from April this year might have also added to corporates’ cash flows and thus further lowered their incentives for borrowing. The contrast of strong bill financing vs weak medium to long term loans, and also the contrast between higher overall RMB loans vs lower loans to the real economy also pointed to the abundant credit supply amid monetary policy easing (such as RRR cut)but much more sluggish credit demand due to the reasons discussed above.

We expect the broad credit growth to pick up in coming months as government bond issuance accelerated and Covid restrictions have been eased on a nationwide basis. However, the weak credit data in April still increased the chance of further policy easing, and we expect more demand stimulus such as stronger infrastructure investment support to be the main policy lever.

In addition, CBIRC commented this afternoon that it does not expect the CNY exchange rate to continue to show one-way depreciation; it noted that investors should refrain from betting on one-way continued depreciation of the currency, and over the long run, it expects the CNY exchange rate to appreciate on RMB internationalization and growth potentials of the Chinese economy. These comments contributed to the temporary stabilization of the currency this afternoon. Our recent analysis suggests continued depreciation increases the chance of PBOC reaction.

Pfft. Blind Freddy can see that thanks to crashing property sales and OMICRON monetary and fiscal policy is severely impaired. That can only mean two things:

China eases more, capital flight intensifies and CNY sinks.

China doesn’t ease more, the economy remains in recession, capital flees and CNY sinks.

Advertisement

Such is the impossible trinity. And as such, the PBoC is breaking. Pantheon Economics:

A Change of Tune from the PBoC Amidst a Slump in Lending

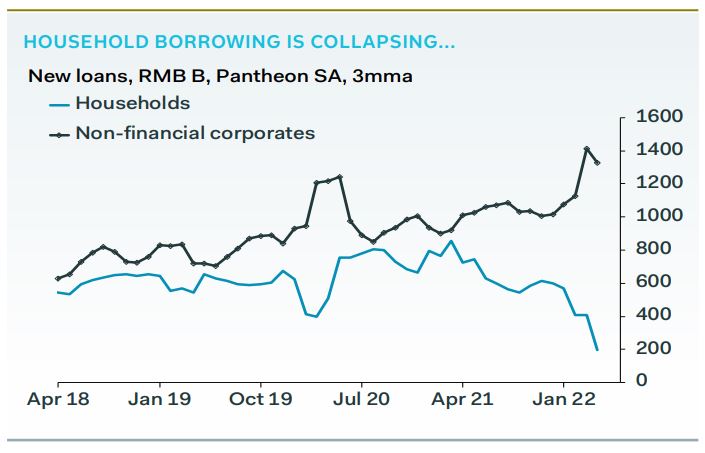

The first cracks are appearing in China’s policy edifice. The authorities have begun to acknowledge the impossible trilemma of zeroCovid, 5.5% growth, and stable debt-to-GDP, which we first raised here. The PBoC said on Friday that “the macro leverage ratio will increase, but stay within a reasonable range”, an admission that debtto-GDP will have to rise if growth is to be supported. The statement followed some pretty horrendous bank lending data. New loans for April were just RMB 645B, down from RMB 3,130B in March, and way below the RMB 1,530B expected by consensus. Both just new lending to households, and the total stock, shrank in April, month-on-month, something not seen even at the start of the pandemic. This douses any hopes that a housing market revival might be in the offing, but also highlights how dire the Chinese consumer story has become.

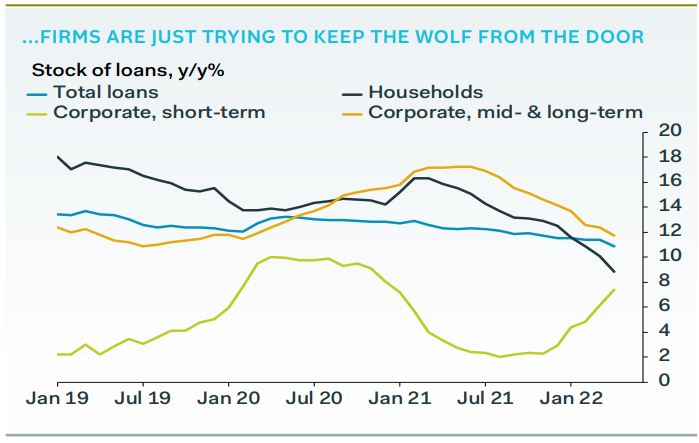

Corporate lending, which has outperformed household lending, also pulled back in April. The PBoC ascribed this weakness to the effects of Covid, and the associated policy measures. But a longer-term trend also flags growing stresses in the sector. One aspect of corporate lending has been accelerating this year, as shown in our chart above.

Unfortunately, it is short-term in nature, as firms turn to overdrafts and bridging loans to get them past the downturn in activity. Mid- and long-term lending— the sort needed for capex—is still slowing. The growth generated by each unit of lending is therefore shrinking, and the risk of NPLs is rising, as many firms are unlikely to survive much longer. The number of corporate zombies is set to rise.

Government bonds will remain a key feature for the rest of the quarter, following instructions further to front-load issuance of the full-year quota. But the impact on infrastructure spending will likely be delayed. Zero-Covid restrictions make it hard to transport materials or labour, so many infrastructure projects will be on hold until restrictions are eased.

We have seen some tentative signs in this direction, but restrictions are still elevated relative to March, as our chart below shows, and the situation is worsening in Beijing. Shanghai, which has had the worst experience of China’s Omicron outbreak, has said it aims for zero spread in the community by May 20, suggesting current restrictions will remain in place at least until then.

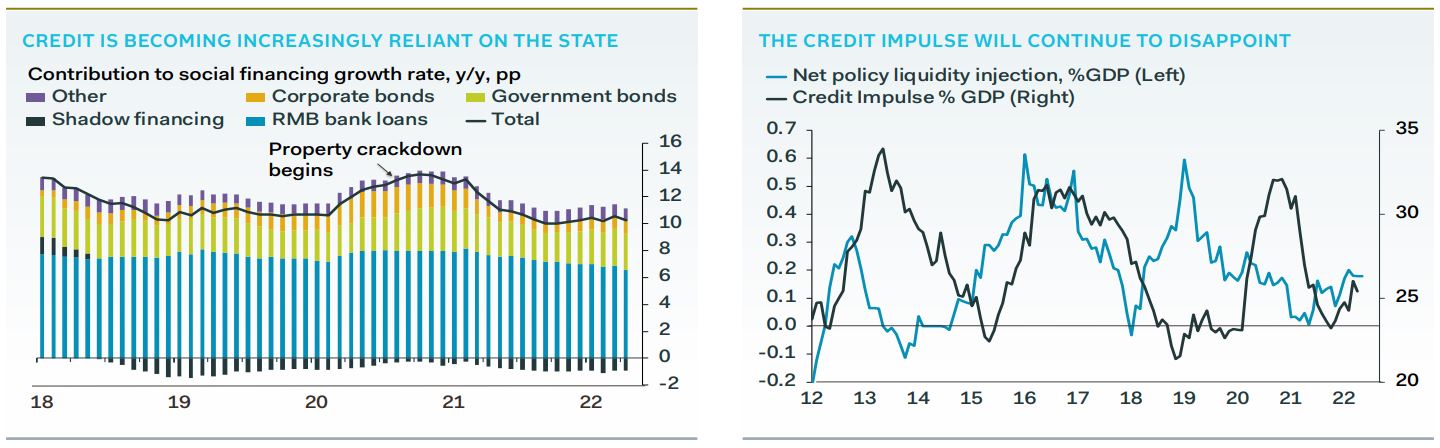

Corporate bonds, as we have argued before, are chiefly being issued by SOEs to finance the acquisition of distressed assets from troubled property developers. Sunac—the third largest Chinese developer by sales—defaulted on Thursday, so another wave of fire sales is likely to hit soon. The proceeds of these bonds, then, will help shore up construction activity, and put a floor—eventually— under land prices, but will not create much new investment, or commodity demand.

The weakness of the credit data seems to have scared policymakers into action, but we have our doubts. The PBoC has finally dropped the target of a stable macro leverage ratio, also known as debt-toGDP, which will now instead be allowed to rise. This should signal a more accommodative stance from the PBoC, which has only engaged in a very modest easing cycle so far, helping to explain the lacklustre credit impulse, as shown in our chart above.

The PBoC, however, also insists that credit should be channelled to where it is needed, and earlier last week repeated the mantra that flood-like stimulus would be avoided. Big liquidity injections would be unhelpful in the current environment anyway, adding to pressure on the weakening currency, and likely not reaching the struggling parts of the economy, given banks’ reluctance to increase credit risk.

Debt-to-GDP, of course, should also be expected to increase if GDP falls, which we expect to happen in Q2. Maintaining stable macro leverage would then require tightening from the PBoC. They can’t do this.

But even current policy would see debt-to-GDP rise.

The PBoC’s statement most likely reflects this new reality, and not a major dovish turn.

China’s central bank effectively cut the interest rate for new mortgages in an attempt to prop up the ailing housing market and boost the slowing economy.

The Sunday announcement from the People’s Bank of China means that first-home buyers will be able to borrow money at an interest rate as low as 4.4%, down from 4.6% previously. The change is aimed at supporting housing demand and will “promote the stable and healthy development of the property market,” the PBOC said.

But note that this is FHBs and all of China’s demand comes from property investment.

Even so, this will be a red rag to CNY bears. TS Lombard:

Advertisement

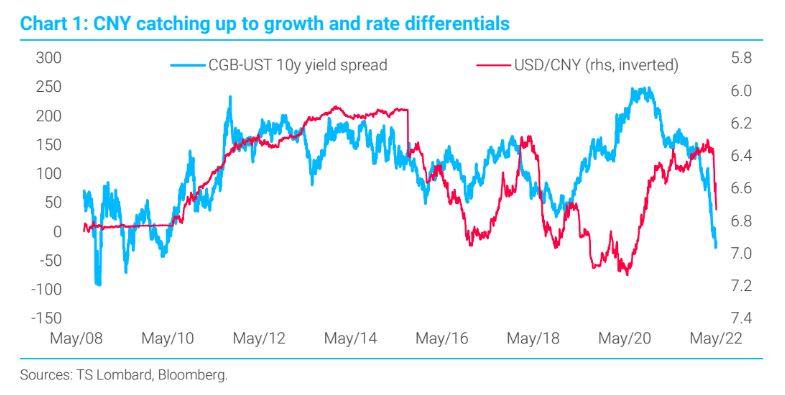

Growth and rate differentials are pushing portfolio outflows and, with them, RMB depreciation. Given large growth headwinds, particularly in interest rate-sensitive sectors, we expect the PBoCto continue easing monetary policy. Another 10 bps policy rate cut and a 50bps RRR reduction (or equivalent) is likely this quarter and half as much again in H2/22.

Foreign selling will continue. However, the peak in monthly portfolio outflows is likely over for now. Foreign investors sold heavily in March as many(especially the Central Bank of Russia) recalibrated geopolitical and economic risk tolerance. Going forward, CGBs remain an attractive option for currency-hedged investors. Yields are capped by domestic weakness and easing,inflation-adjusted returns are good, and bond index inclusion provides a tailwind for CGBpurchases. CGBs offer the option of capital preservation/gain with global yields rising. All these factors will help mitigate some of the yield differential-driven outflows.

The trade surplus decline is still to come. Less deadly Covid-19 variants also mean greater export competition, declining DM stimulus and a trend reversal in global goods consumption, hitting China’s trade surplus. However, the slump in domestic demand will support the trade surplus, which in April reached US$51bn as imports declined faster than exports. We expect the trade surplus to decline from record highs while net exports remain positive, partially offsetting capital outflows.

ThePBoC’s reaction function. Beijing has to maintain an easing bias to put a floor on economic activity; this necessitates lowering the price and increasing the quantity of money. A weaker exchange rate is a welcome by-product of monetary policy focused on growth. RMB depreciation becomes a constraint on monetary policy only if it threatens financial stability and/or imposes excessive inflationary burdens. The latter is unlikely given domestic demand weakness, but the former could happen if the pace of depreciation continues at its current rate. Uncontrolled and rapid FX weakness might trigger surging household and corporate outflows and add to dollar-debt repayment difficulties in the property sector.

Where does the RMB stop? Given the macro outlook, policy framework and constraints, we expect the PBoC to attempt a managed stepped depreciation of RMB to pre-Covid levels of 7-7.2within the next nine months. On a trade-weighted CPI basis, China’s REER is still7% above pre-Covid levels, the CFETS basket is10% stronger and USD/CNY5%. A further decline of~6% wouldunwindCovid-related gains and put the currency broadly in line with domestic fundamentals. Further economic weakness–beyond our below consensus2022 GDP forecast of ≤4%–would imply a steeper fall towards 7.4

This is the fastest devaluation I can remember and the PBOC has not even cut interest rates properly yet. There is a real risk of capital outflow and CNY depreciation turning unruly and overshooting.

Which, given monetary transmission is failing anyway, will blow up markets and the global economy as sure as the sun rises.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.