Yes, it is a non-stop nightmare for the Chinese property market as “houses are for living in, not speculation”. The great adjustment has so far been confined largely to construction volumes over prices but no more!

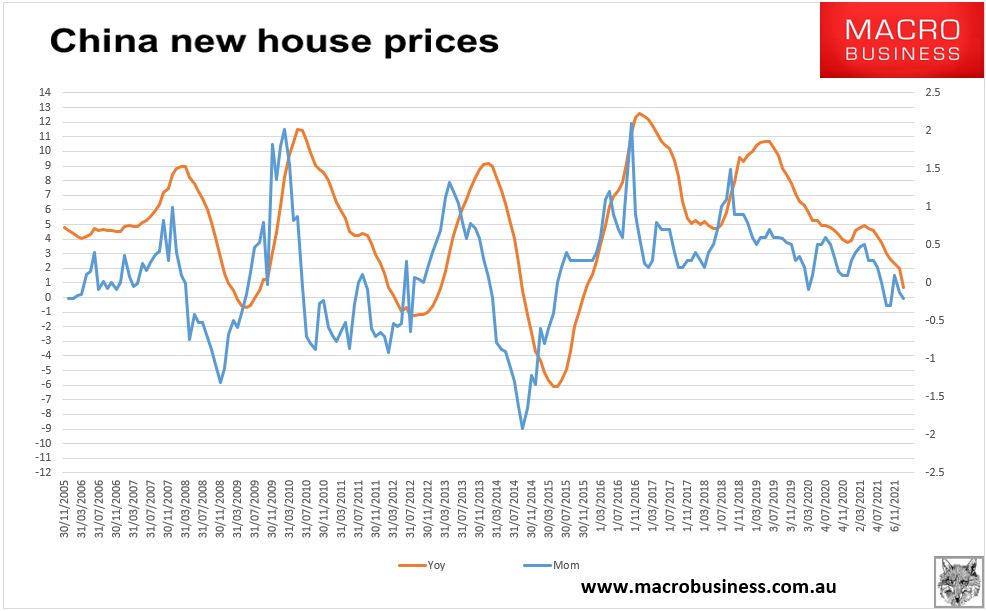

Late yesterday China released its latest 70-city guide to prices and kapow! April price falls were modest at -0.2% and 2% in aggregate:

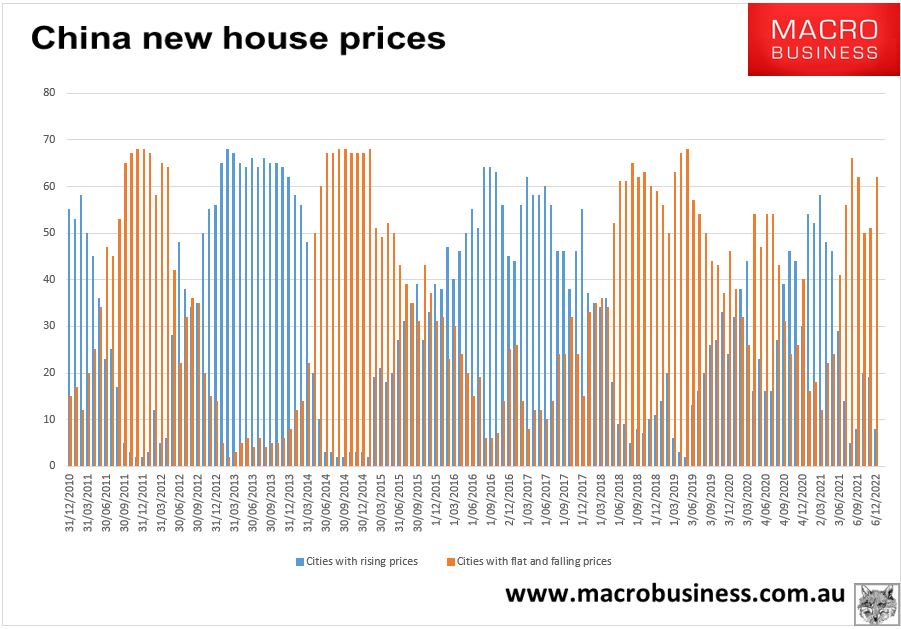

But the correction broadened:

Advertisement