Chinese banks cut a key interest rate for long-term loans by a record amount, a move that would reduce mortgage costs and may help counter weak loan demand caused by a property slump and Covid lockdowns.

The five-year loan prime rate, a reference for home mortgages, was lowered to 4.45% from 4.6%, according to a statement by the People’s Bank of China Friday. That was the largest reduction since a revamp of the rate in 2019. A majority of economists surveyed by Bloomberg had predicted a cut by five to 10 basis points.

As I warned last year when the property adjustment began, China has never cut RRR without finally resorting to prime loan rate cuts as well so this is zero surprise.

But, it is nowhere near enough because the price of money is not the problem. It is the distribution of credit that is at issue and there is no move to change that.

Advertisement

Ipso facto you can expect a lot more rate cuts.

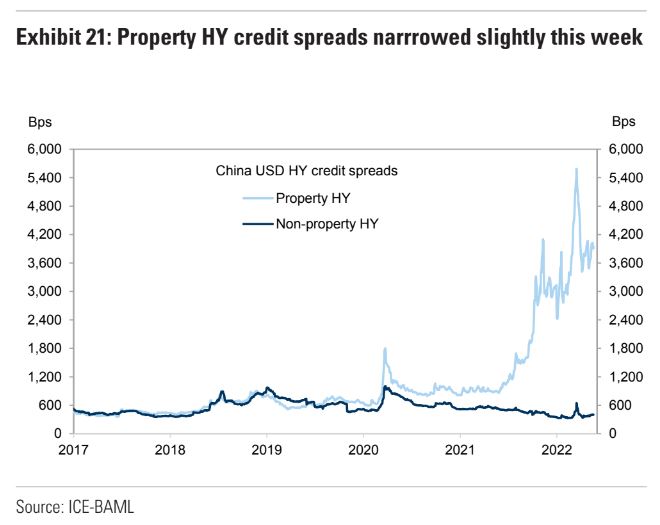

To wit, developer credit remains utterly frozen so one mortgage rate cut is like a rain shower in the Arctic:

Advertisement

Defaults are piling up and developers keep going under. Goldman:

Raising FY22 China Property HY default rate forecast to 31.6%. There has been 22 China HY issuers that have either defaulted on their USD bonds or have conducted bond exchanges since the start of this year, all of which are related to the property sector. Given the pick up in stresses, we raise our FY22 China Property HY default rate forecast to 31.6% (from 19.0% previously), which was our previous bear case assumption. We commented in recent weeks that the likelihood of our bear case scenario has increased.

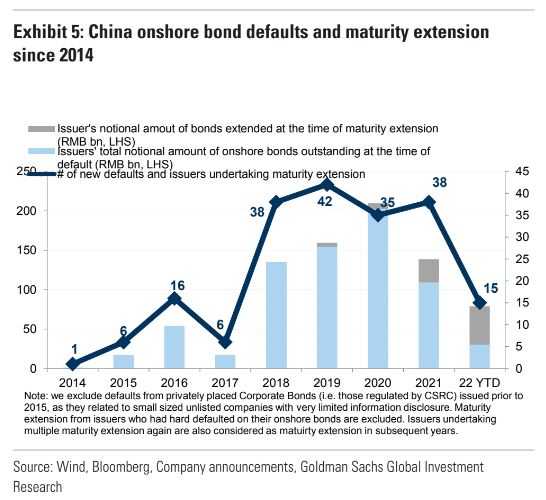

Onshore bond stresses increasingly emerge via maturity extensions. So far in 2022, 6 issuers have defaulted on their China onshore bond obligations, with an aggregate RMB 30.2bn in notional amount of onshore bonds outstanding at the time of default. In comparison, 9 issuers avoided defaults by conducting bond maturity extensions, and the notional amount of bonds that were extended is RMB 48.8bn. Therefore, unlike in previous years, more issuers have conducted bond exchanges than have defaulted so far this year.

A long path towards restructuring for China property HY sector. We view bond exchanges and maturity extensions as efforts that provide short term relief on credit stresses by pushing bond maturities to a later date, but are not sufficient to resolve the credit issues. Furthermore, we note a number of issuers that have defaulted over the past two years (including property and non-property companies) are still to restructure their debts. To us, these indicate we are on a long path towards restructuring the China property HY sector.

So long as developers have no access to US dollar, and increasingly, local credit, they are caught in a solvency crisis and would-be buyers are put off by the counter-party risk.

Advertisement

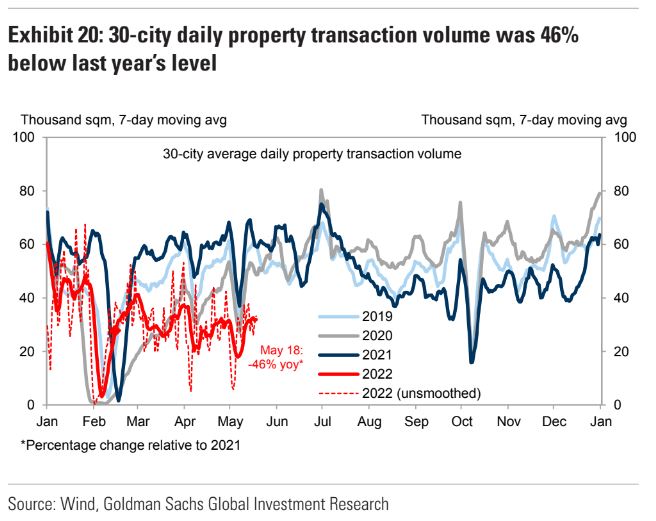

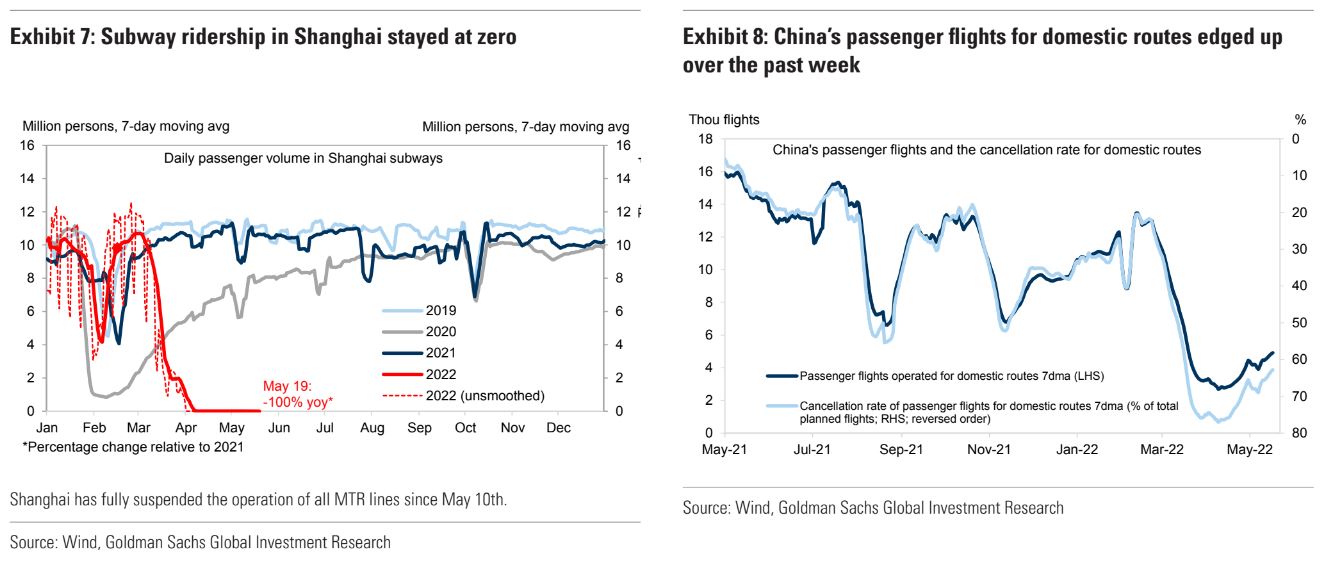

Hence sales remain in the s-bend:

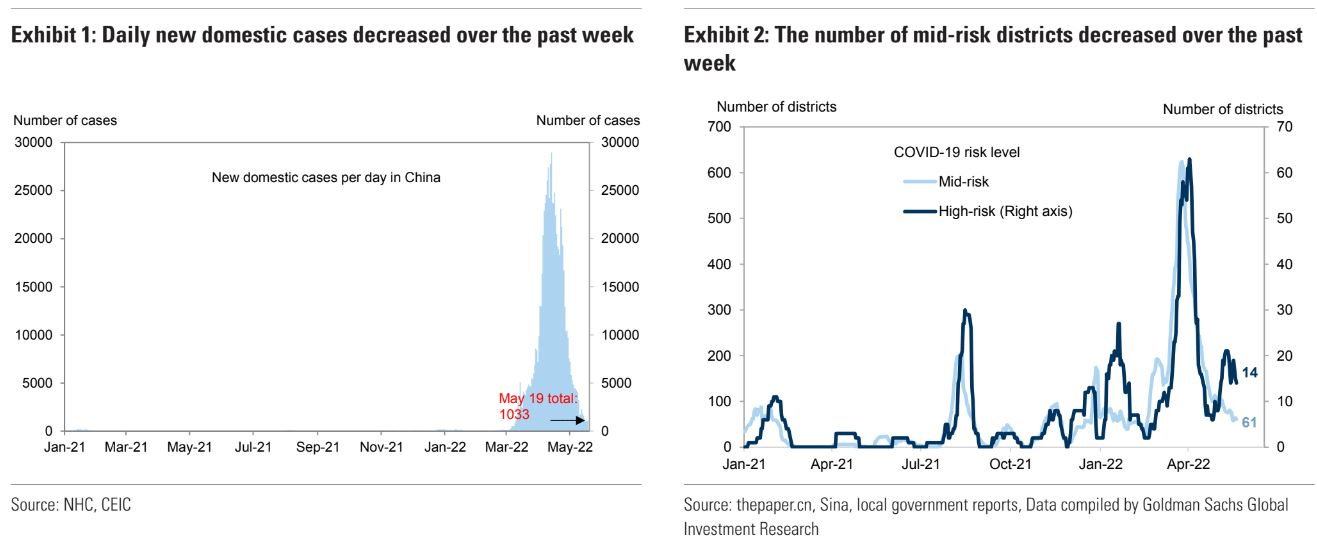

Not helped by OMICRON:

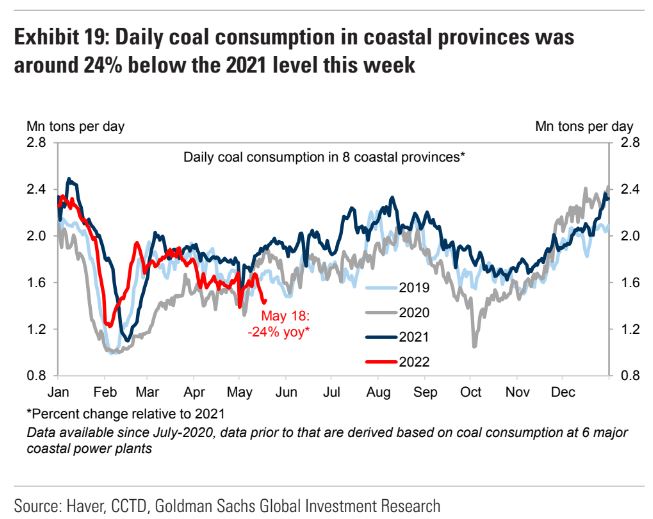

With both obliterating output:

Advertisement

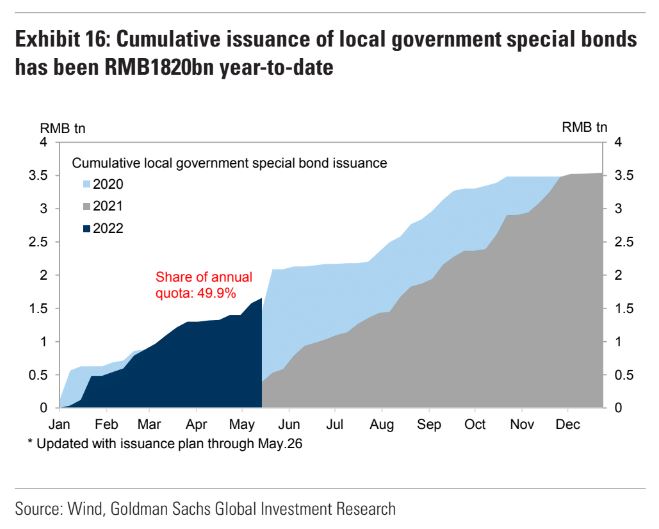

Transmission of the fiscal stimulus offset also remains inhibited. Local governments are issuing debt:

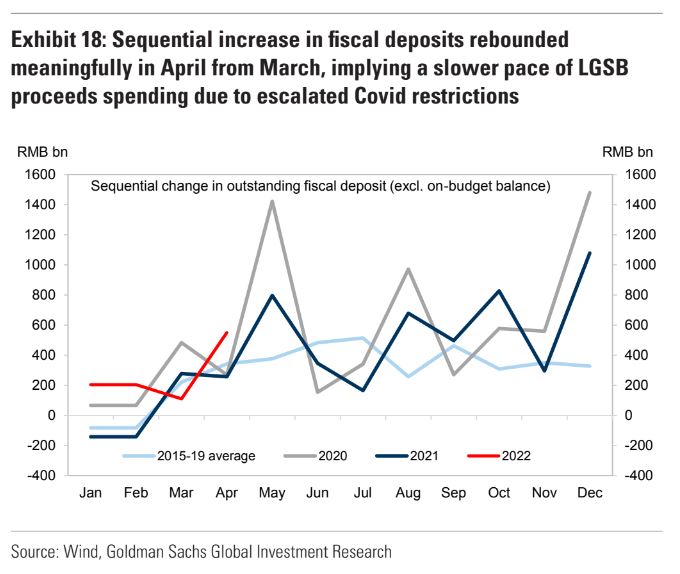

But they can’t spend it with everybody locked up:

Advertisement

So, ahead for the economy is rising infrastructure spending and tumbling property starts for some kind of net outcome near neutral or worse.

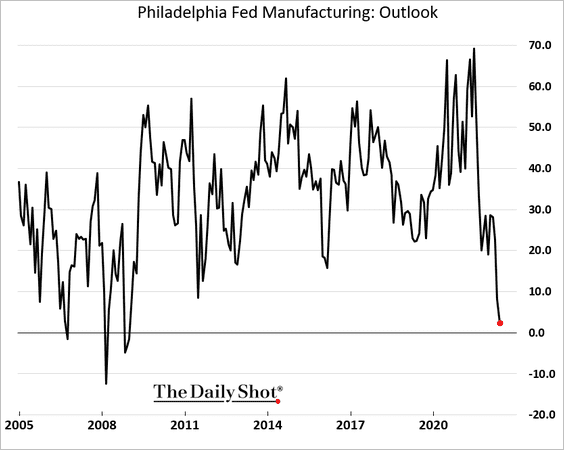

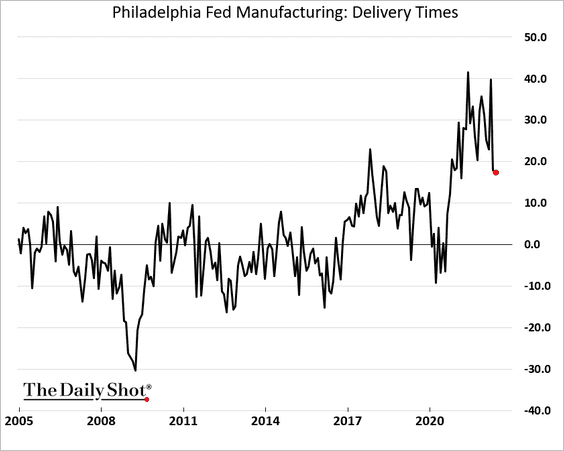

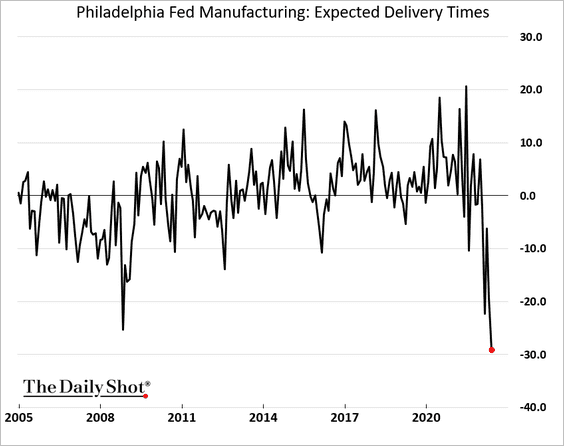

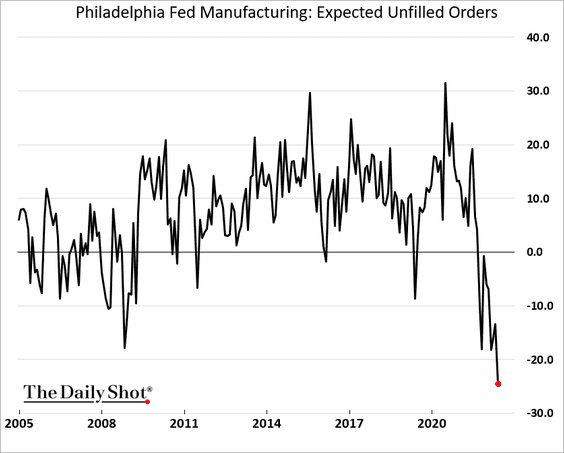

And that’s before the exports hit arrival from the US. US manufacturing indexes are sickening fast as the consumer transitions to services and retrenches on interest rate tightening

Advertisement

The same is coming to China soon.

CNY rallied on the rate cut but there’s still no reason to buy and every reason to sell. China is in all sorts of trouble and the only thing that can save it is a lower CNY.

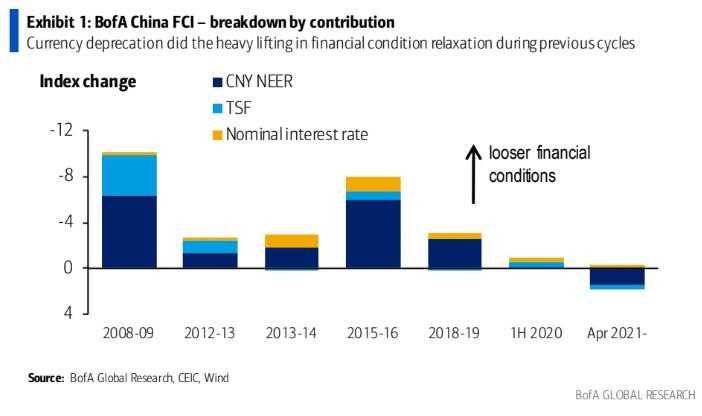

In fact, that’s all that’s ever saved it, BofA:

Currency depreciation needs to do the heavy lifting

A careful examination of the three underlying components of our China FCI—CNYNEER, TSF and nominal interest rate—indicates currency depreciation used to play the most important role in loosening overall financial conditions during previous cycles (Exhibit 1 and Exhibit 2). In sharp contrast, this time, notable year-over-year CNYappreciation has driven the financial conditions tighter since mid-2021.

In our view, further currency depreciation would be much needed to relax the financial conditions in China. With rapid yuan depreciation seen over the past few weeks (6.8% fall against USD since early April), the PBoC rolled out policy measures to curb further weakness in yuan. On April 25, the central bank announced to lower the FX reserve requirement ratio (RRR) by 100bp to 8% (Exhibit 3). However, such symbolical moves will unlikely prevent depreciation pressure from building, especially in light of the divergence in central bank policies within and outside of China. Our FX strategist expects USD/CNY to reach 6.80 at end-4Q, and 7.20 in a bear-case scenario.

An outright China crisis may well be what breaks in the global economy to eventually force a Fed pivot.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.