CBA: Next week’s ABS data crucial to RBA’s interest rate decision

By Gareth Aird, head of Australian economics at CBA:

Key Points:

- Next week the ABS will publish the Q1 22 Wage Price Index (WPI) and the April labour force survey.

- These two data releases are the most important economic information ahead of the June Board meeting.

- We expect the WPI to increase by 0.8%/qtr in Q1 22 which would see the annual rate step up to 2.5%.

- We forecast the unemployment rate to dip from 4.0% to 3.9%.

- Outcomes on the WPI and unemployment rate in line with our forecasts would be consistent with a 25bp rate hike at the June RBA Board meeting (our central scenario).

- A bigger lift in the WPI or more significant fall in the unemployment would raise the risk of a 40bp hike at the June Board meeting (such a move could be justified by the RBA as the data would be stronger than their recently released forecasts and a 40bp hike would take the cash rate to 0.75%; a more ‘orthodox’ rate).

- Notwithstanding, a rate hike of more than 25bp at the June Board meeting would put unnecessary angst into a household sector that is already quite concerned about the economic outlook, in part because of the expectation of higher rates.

Overview

The RBA’s tightening cycle is underway. Every monthly RBA Board meeting over 2022 from here will be ‘live’. This means that at each meeting for the remainder of this year the Board will debate the case to either raise the cash or leave the cash rate on hold. As a result, key economic data that proceeds a meeting has the capacity to influence the pending monthly policy decision.

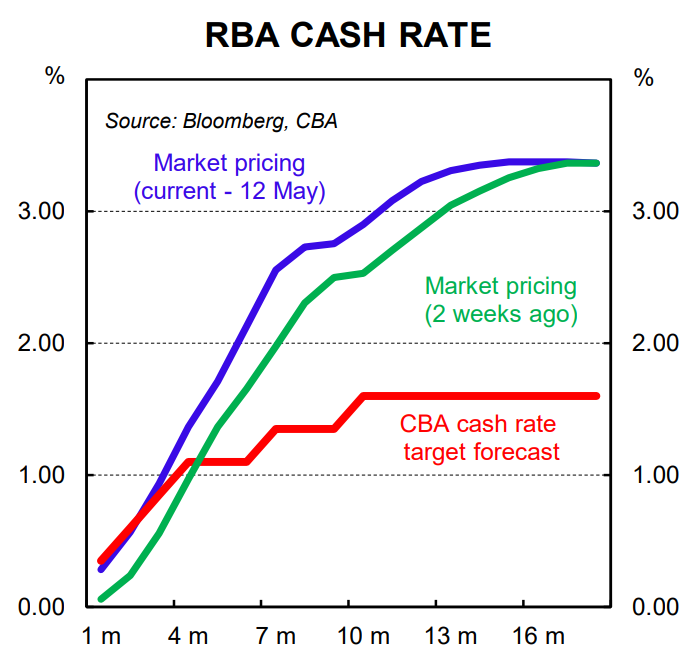

Our central scenario sees the RBA deliver 25bp rate hikes in June, July, August and November 2022 that would see the cash rate target end the year at 1.35%. We then expect a further 25bp rate hike in February 2023 that would see the cash rate target at 1.60%. From there we have the key policy rate on hold over 2023. As we have covered previously, natural tightening continues over 2023 given the fixed rate home loan expiry schedule, keeping the RBA on hold, in our view.

The decision to raise the cash rate by 25bp, rather than 15bp or 40bp, at the May Board meeting caught almost every analyst off guard. Whilst the hike of 25bp was a ‘conventional’ rate increase, it took the cash rate to an ‘unconventional’ level (0.35%). Most forecasters calling for a hike in May were looking for 15bp, while some analysts had pencilled in a 40bp hike (i.e. an increase in the cash rate that would have taken the cash rate target to either 0.25% or 0.5%).

A tightening cycle from here that is based on orthodox increases in the cash rate of 25bp (or even 50bp at a particular meeting) would see the cash rate target at any given point sitting at an ‘unorthodox’ level. As such, markets will be aware that the RBA could deliver a 40bp hike at any particular meeting if the Board sought to reset the cash rate target to a more conventional metric. Such a move would likely need a key piece (or pieces) of economic information to support the case for a larger than 25bp increase in the cash rate. That data is likely to arrive earlier in the tightening cycle given we expect forward looking indicators of the economy to slow as the policy rate moves towards neutral (CBA estimate the neutral rate is just 1.25%, but we expect the terminal rate to land a little higher).

In that context, there are a few very important data releases next week that could influence the Board’s decision at the June meeting – the Q1 22 wage price index (due Wednesday 18/5) and the April labour force survey (due Thursday 19/5).

Q1 22 Wage Price Index (due 18 May)

The RBA chose not to wait to see official data on labour costs when the Board made its decision to raise the cash rate in May. Instead the Governor, in his post meeting statement, cited the RBA’s “business liaison” and “business surveys” to make the case that wages growth is moving sufficiently higher. But the official data still matters. And the Q1 22 WPI will provide detailed information on how wages pressures are evolving across the economy.

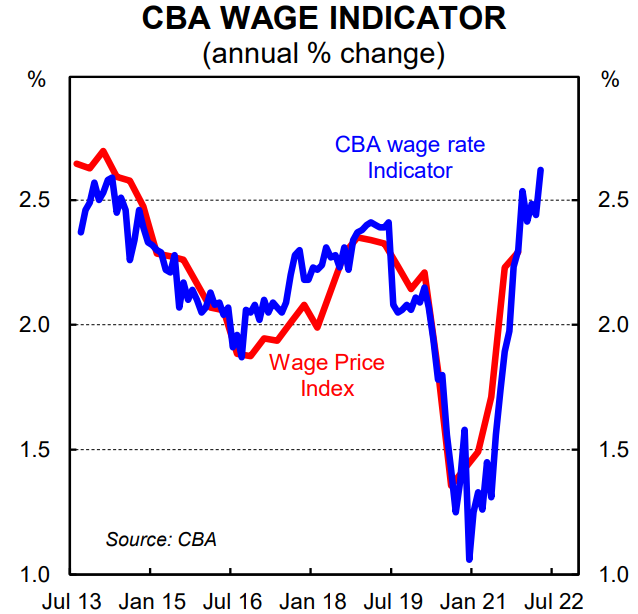

We use quite a sophisticated methodology based on our internal data on wages and salaries paid into CBA bank accounts to model the WPI. More specifically, we apply a strict criteria to the accounts we include in our sample each month to account for people moving jobs, receiving a bonus or modifying hours worked in any material sense. We also take into account changes in tax rates or levies.

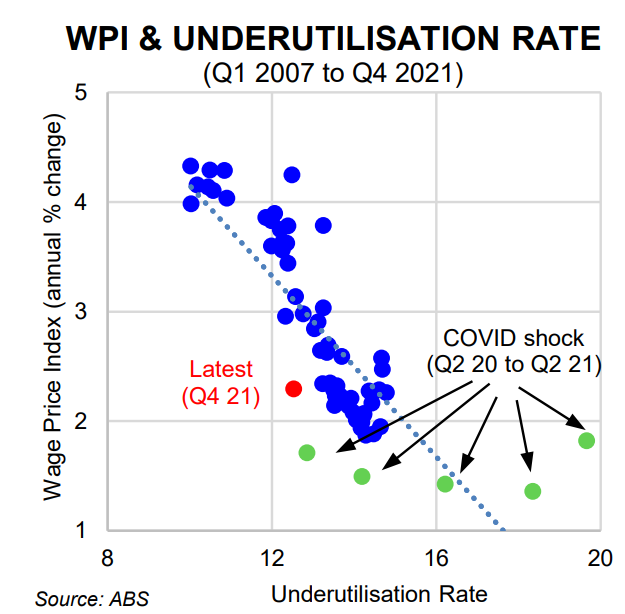

The upshot is that our real time wage price model, which is based exclusively on wages and salary payments into CBA bank accounts, very accurately tracks the WPI (see below chart).

Our data suggest that wages inflation, as measured by the WPI, accelerated by ~0.8% over Q1 22 to take the annual rate to 2.5% (note our data is up to April). Indeed that is our forecast. It means that on a six month annualised basis we expect wages growth to be travelling at 3.0% in Q1 22 (recall that the Q4 21 WPI rose by 0.7%/qtr – it was a ‘soft’ 0.7% given it was 0.65% when taken to two decimal places).

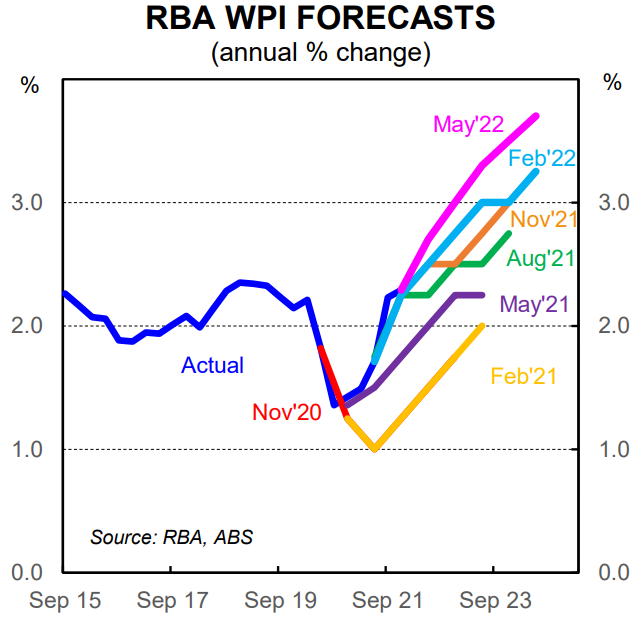

The RBA’s updated forecasts in the May Statement on Monetary Policy (SMP) put the Q2 22 at WPI at 2.7%/yr. Such an outcome implies quarterly growth in the WPI of ~0.7% over both Q1 22 and Q2 22. These forecasts appear somewhat inconsistent with the RBA’s business liaison and the Governor’s comments that, “larger wage increases are now occurring in many private-sector firms”. But they do imply that whilst the RBA acknowledge that strong pay rises are taking place in some parts of the private economy, aggregate wages growth is still taking some time to rise in a material sense.

An outcomes for the Q1 22 WPI in line with our forecast or the RBA’s would be consistent with, as Governor Lowe labelled last week, a “business as usual” increase in the cash rate of 25bp at the June Board meeting. But an increase in the Q1 22 WPI of 0.9%/qtr or above could be used as justification for the RBA to deliver a ‘business not as usual’ 40bp rate hike which would take the cash rate target to 0.75%.

April labour force survey (due 19 May)

The labour force data remains very important to the monetary policy outlook. To be clear, the unemployment rate is a lagging indicator. It provides a gauge on how the economy has been performing rather than a guide to what the future holds. Notwithstanding, the level at which the unemployment rate prints over coming months will feed into policy deliberations as tightness in the labour market is linked with wages outcomes and by extension inflation.

If the unemployment rate continues to grind lower and to a level that the RBA assess to be below the NAIRU (non-accelerating inflation rate of unemployment), the Board may feel the need to tighten policy more aggressively than we believe is necessary at this juncture (i.e. deliver a larger than 25bp rate hike at the June Board meeting). We say this because labour market supply will rise over 2022 as the immigration tap has been turned back on and temporary workers are returning.

The unemployment rate in any given month is influenced by the change in employment, the participation rate and the change in the working age population. As such, there are a number of moving parts that feed into the jobless rate which complicates the forecasting process.

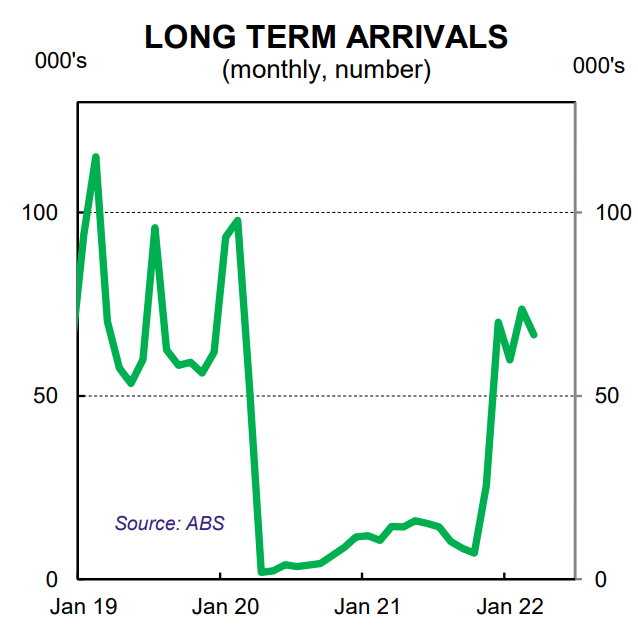

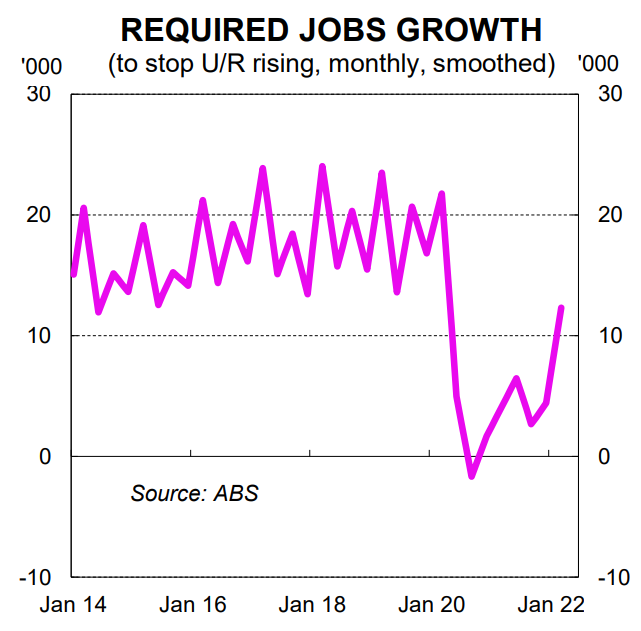

The reopening of the international border has seen growth in the working age population lift. This means that on an unchanged participation rate the economy needs to generate a larger increase in monthly employment to keep the unemployment rate flat (see below charts).

Our forecast for the April labour force survey is for employment to rise by 30k and for the participation rate to remain flat at 66.4%. On our calculations this would see the unemployment rate edge lower to 3.9% (here we assume that growth in the working age population continues to lift due to an increase in overseas resident arrivals).

The RBA forecast the unemployment rate to average 3.8% over the June quarter (note that this is an average rate over the quarter and note a point forecast for the month of June). As such, an employment rate in April of 3.9% or 3.8% would be consistent with this outcome and by extension a 25bp hike at the June Board meeting. But an unemployment rate below 3.8% could sway the Board to deliver a bigger rate hike at the June Board meeting (i.e. 40bp).

On one hand, we are quibbling over decimal points and the monthly labour force survey is something of a lottery. However, the margins are fine at this point when predicting what the RBA Board will decide at the June meeting.

Our expectation is that the data next week on wages and unemployment will support a 25bp rate hike at the June meeting. And we think that slightly stronger outcomes than we anticipate should not be cause for concern and used to justify a 40bp hike.

That said, if wages prints significantly stronger than our forecast and/or the unemployment rate drops more materially the RBA Board may opt for a 40bp hike in June. It would not be a “business as usual” rate hike, but it would restore the cash rate to a more orthodox metric. Indeed it would take the cash rate back to its pre pandemic level of 0.75% (thus the ‘emergency cuts’ would be removed).

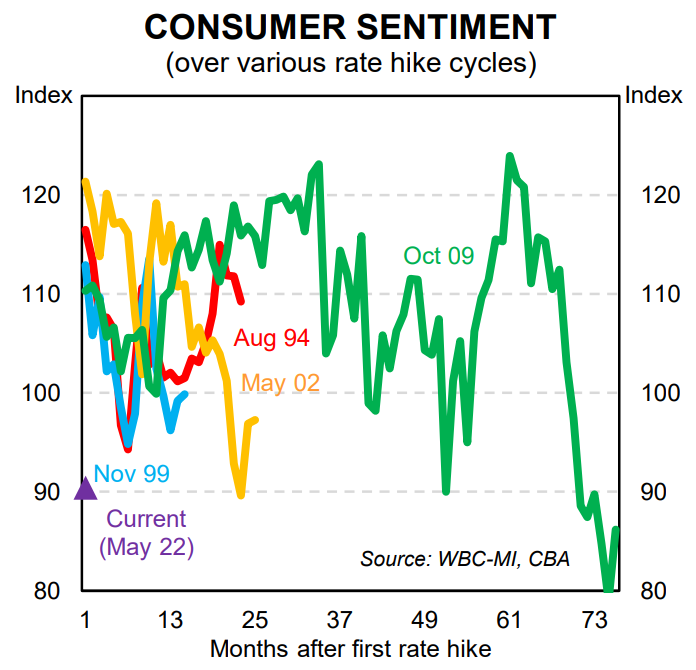

A rate hike larger than 25bp in June accelerates the RBA’s timeline of normalising the cash rate. But it risks putting undue angst into a household sector where consumer confidence is brittle. Indeed consumer sentiment has never been this low at the beginning of an RBA tightening cycle – it is currently well below average levels while at the beginning of previous rate hike cycles confidence was well above average levels (see below chart). Given RBA Governor Lowe flagged 25bp moves as “business as usual” last week, anything larger that a 25bp rate hike at any particular monthly Board meeting could genuinely alarm borrowers.