The steam had well and truly come out of Australia’s housing market before the Reserve Bank of Australia (RBA) commenced its monetary tightening on Tuesday.

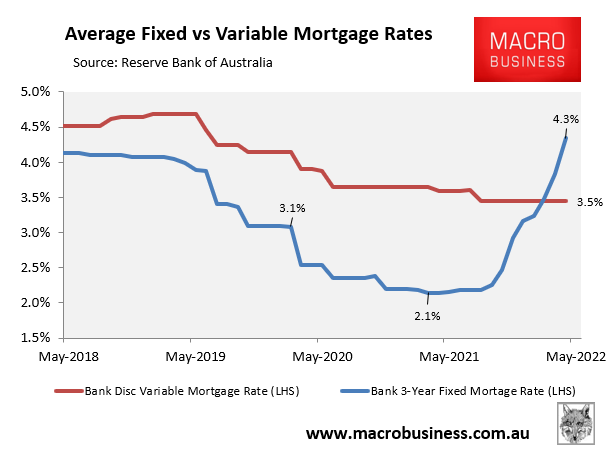

While variable mortgage rates had yet to rise, fixed rates – which comprised around half of all borrowing over the pandemic – had already roughly doubled, according to RBA data:

Fixed mortgage rates surged long before the RBA hiked rates.

This surge in fixed mortgage rates, alongside the general unaffordability of Australian housing, had driven mortgage demand sharply lower, which has historically been a leading indicator for house prices:

Falling mortgage growth bearish for house prices.

Not surprisingly, then, sales volumes have fallen significantly from their December quarter peak, “with the quarterly number of home sales nationally estimated to be 14.0% lower relative to the same time a year ago”, according to CoreLogic’s April housing market report.

CoreLogic’s Tim Lawless explained that “with higher inventory levels and less competition, buyers are gradually moving back into the driver’s seat. That means more time to deliberate on their purchase decisions and negotiate on price”.

Looking ahead, Mark Bainey – chief executive of Sydney-based property developer Capio Property Group – believes the outlook for Australian housing is “dire” as the RBA lifts rates and homebuyer demand collapses:

“I think the initial shock of the first interest rate rise in more than a decade will really slow the market and put a handbrake on house prices”.

“The first rate increase will be a line in the sand to show people this is the new economic reality, and it will be a shock for them to experience multiple interest rate rises.”

“Buyer inquiry levels are down 50 per cent at the moment, so demand has essentially collapsed”.

“Inquiries are always the best indicator of where prices are going. If inquiries are going down, then prices are going in the same direction. We’re prepared for it, but I think the outlook for the market is quite dire.”

“Anyone who has bought in the last 12 months is going to be the first in line for some pain through the rate rise cycle”.

“They are a generation of home buyers who have never experienced a rate rise, so the harsh reality of a higher mortgage cost has just hit them.”

Henderson Advocacy buyer’s agent Jack Henderson agrees, saying the contraction in buyer demand has allowed him to secure properties at a heavy discount:

“A lot of the properties that we’re buying right now are around 10 per cent or 15 per cent cheaper than what they would have sold for six months ago because people are just sitting on their hands, scared about what could happen, so there’s less competition”.

Whereas SQM Research managing director, Louis Christopher, has forecast a 7% to 8% fall in Sydney and Melbourne house prices this year amid “a sharp drop in the number of buyers”.

With most economists tipping a 200 basis point increase in mortgage rates, which would lift repayments by more than one-third, Australia’s housing market is clearly cruising for a bruising.