Westpac with the note. What’s “prudent” about tightening into tradable inflation, stagnant wages, and a global bust, Bill?

—

Recently Westpac revised down its growth forecast for 2022 from 5.5% to 4.5%. That reflected the sharp increase in the cost of living as headline inflation lifted by 5.1% in the year to March 2022, including an increase of 2% in the March quarter and an earlier and more rapid policy tightening from the RBA

That said, near term prospects are still positive. Post-COVID reopening is expected to see a further solid lift in consumer spending – as household savings normalises and more income flows through to spending. But in real terms the extent of this lift will be constrained by the higher cost of goods and services.

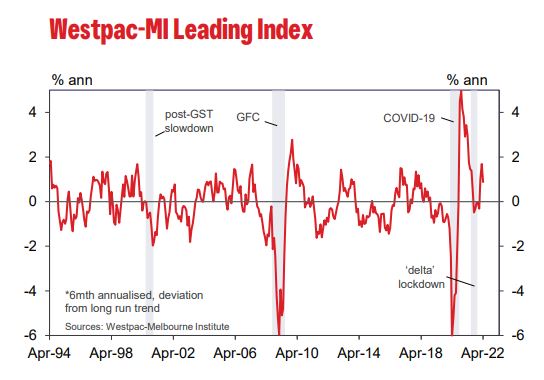

By holding comfortably above the zero level, the Leading Index is also consistent with above trend growth in 2022 and a large boost coming in the June and September quarters.

The Index growth rate has lifted from –0.02% in November 2021 – when the two major eastern states were just emerging from delta lockdowns – to 0.88% in April 2022. The 0.91ppt improvement has been mainly driven by a lift in total hours worked (contributing +0.62ppts, accounting for over two thirds of the turnaround); a widening yield spread (+0.27ppts); and a lift in commodity prices in AUD terms (+0.26ppts) with some additional support coming from dwelling approvals and US industrial production (adding +0.21pts on a combined basis).

These improvements have been partially offset by a softening in consumer expectations, the Westpac-MI CSI Expectations Index and the Westpac-MI Unemployment Expectations Index taking 0.45ppts off the leading index growth rate on a combined basis.

The Reserve Bank Board next meets on June 7.

Westpac expects that the Board will decide to raise the cash rate by a further 40bps to 0.75%. Most analysts favour a more cautious move of 25bps. Following the increase of 25bps in May the move would unwind the emergency rate cuts that the Bank enacted during 2020 when the economy faced the COVID crisis.

With the crisis having passed and the Bank challenged with the daunting task of bringing underlying inflation down from a forecast 4.75% to 3.25% in 2023 that emergency stimulus is no longer appropriate.

The Board will also be aware of the efforts of other central banks, including the US Federal Reserve, to quickly move interest rate settings back to neutral. While current headline inflation in Australia is below these other countries, the RBA has started more slowly than central banks abroad and inflation pressures are still increasing.

It is also much more prudent to front load the increases where at a stage in the cycle when rates are clearly below what might be considered a ‘neutral’ level.