ANZ Bank had forecast in February that dwelling prices would rise by 8% cent in 2022, followed by a 6% decline in 2023.

However, ANZ says the prospect of aggressive monetary policy tightening means that it now expects dwelling prices to fall by 3% in 2022 and 8% in 2023.

ANZ economists have forecast the official cash rate (OCR) will rise to 2.35% by mid-2023, compared with 0.35% currently. This would equate to an average variable mortgage rate of 4.75% and would “significantly” reduce borrowing capacity.

From The AFR:

“Housing prices look set to turn lower in coming months,” the economists wrote.

“While fixed rates have already risen sharply, the steep increases in the cash rate will flow through to variable mortgage rates, lifting minimum repayments significantly and reducing borrowing power. Macroprudential tightening, solid supply and constrained affordability will also be headwinds for house prices.”

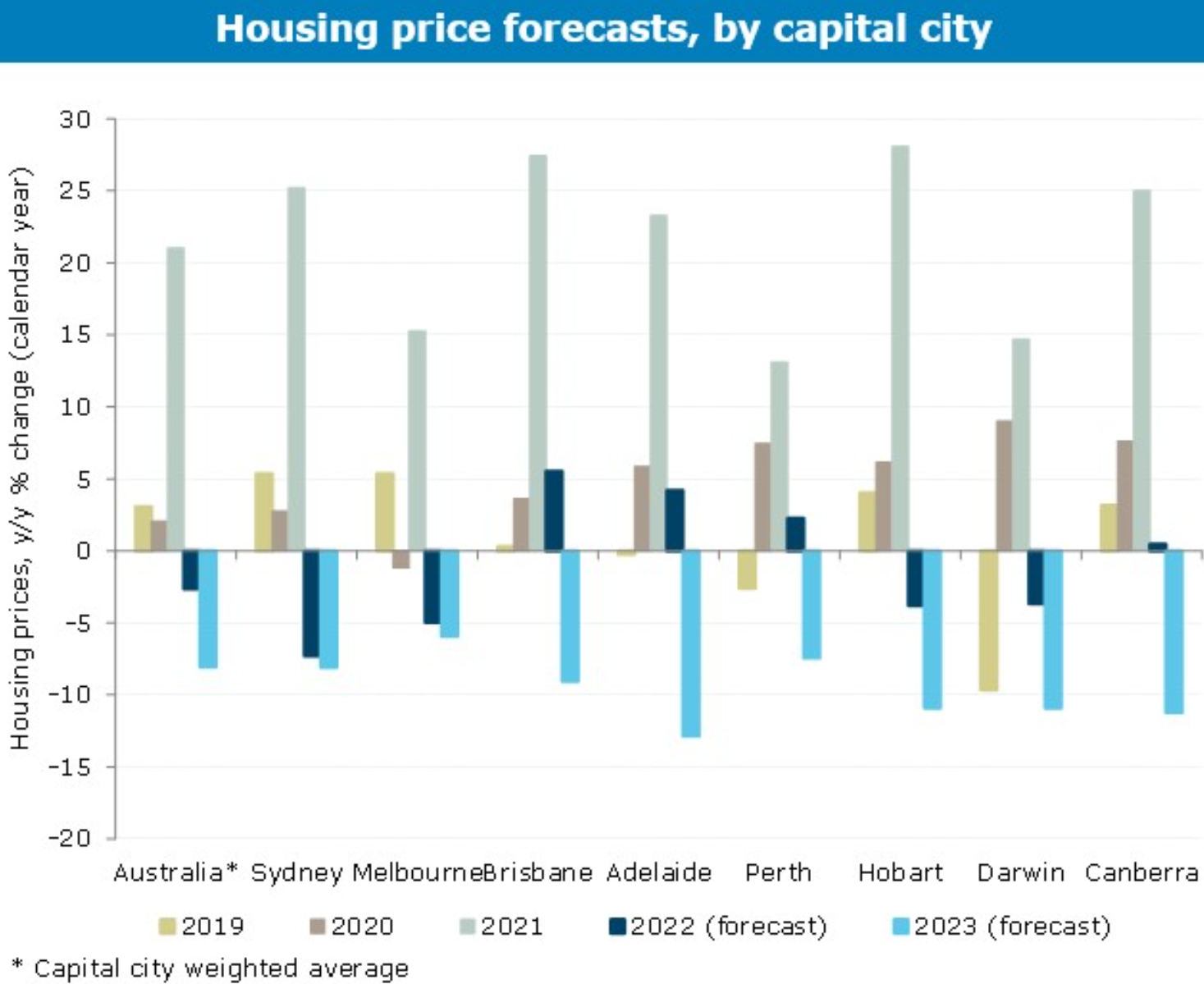

Below are the ANZ’s updated price forecasts:

I believe the ANZ’s house prices forecasts are too optimistic if the OCR rises to 2.35% by mid-2023. Such an increase in the OCR would see Australian households experience their sharpest ever increase in mortgage repayments – a circa 80% rise – resulting in far steeper house price falls.