Other than faltering macro, the other big one is earnings. In particular, the forward estimates of coked-up kids on Wall Street. Morgan Stanley has more.

—

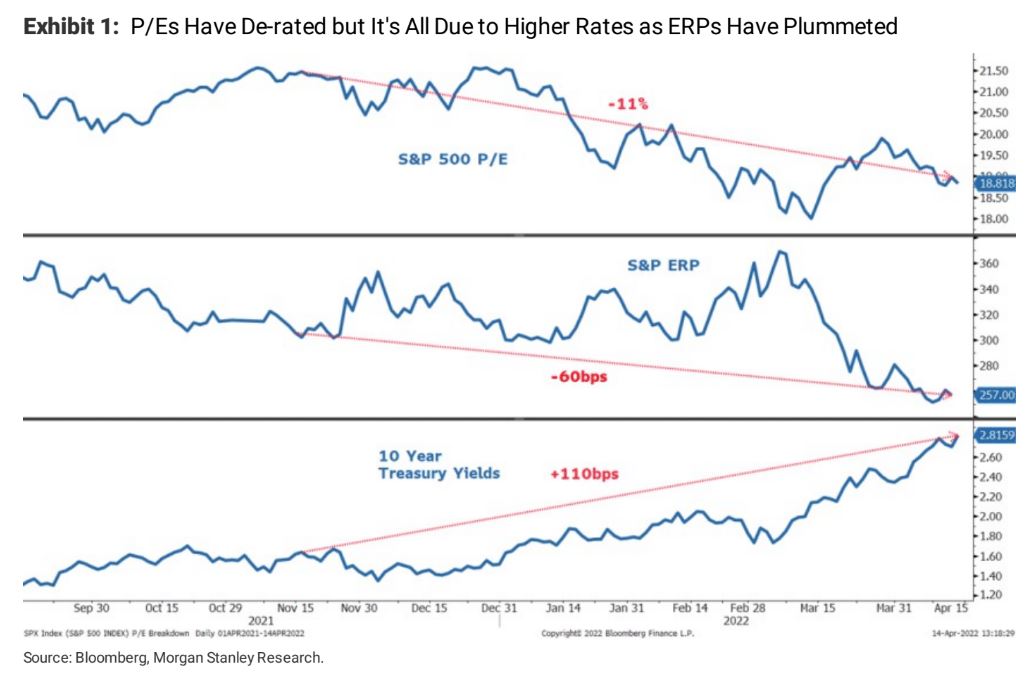

We make the case that earnings revisions will decelerate amid 1Q reporting season as the MS Business Conditions Index (a survey of our industry analysts) just fell further and margin headwinds mount / are not fully reflected in consensus estimates. Stocks should discount this risk via the ERP channel.