The smartest guys in the room were the last to know as usual. Starting with Goldman which is still fighting it:

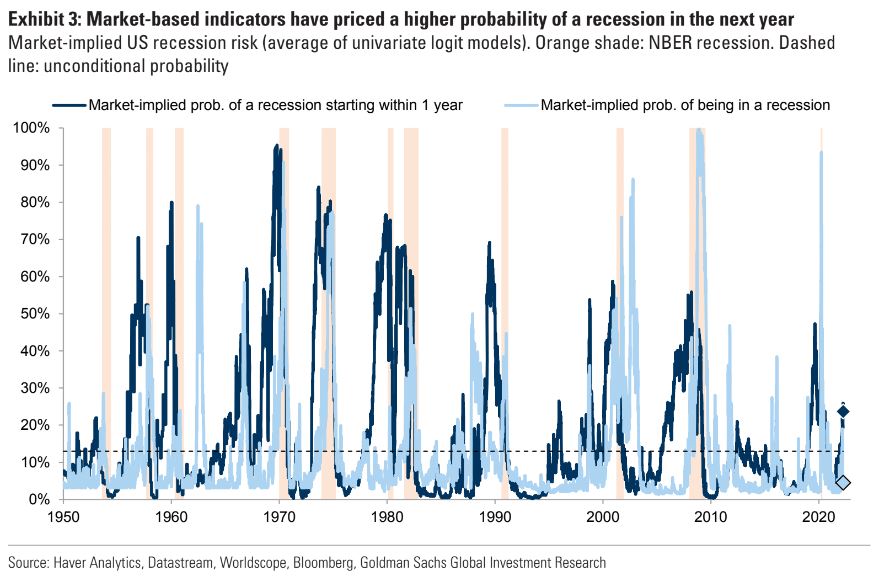

With elevated inflation, the Fed tightening cycle accelerating and the US yield curve inverting, investors are increasingly worried about the risk of a recession.

While rising inflation and rates have pushed investors to higher strategic allocations to real assets including equities, a recession could change that playbook materially on a tactical basis.

Forecasting recessions is difficult – while the yield curve has historically inverted ahead of recessions, it has been less useful for timing them. Current high inflation might drive an earlier and deeper inversion. Looking at a broader range of market indicators, including cyclicals vs. defensives valuations, credit spreads and Fed funds pricing, might help gauge future recession risk. Currently they send a mixed message, with cyclicals vs. defensives valuations and the yield curve more bearish, and other indicators less so.

Low inflation and gradual monetary policy tightening since the Great Moderation has resulted in cycles becoming longer and lower macro volatility. In fact, often imbalances in the economy that grew due to lack of macro volatility drove recession risk. Before then recessions were more frequent and often related to sharply higher rates and oil price shocks, similar to now.

Most recessions triggered, or occurred around, equity bear markets, but not all of them – some equity drawdowns were smaller. Broadly, cross-asset performance during recessions since WW2 has been mixed, with poor returns in equities, credit and cyclicals vs. defensives the most consistent pattern. In part this is as recessions differed materially in terms of macro and market conditions, in particular in function of inflation.

Timing bear markets is even more difficult than forecasting recessions. Often equities perform well into bear markets, correct sharply early on and can recover quickly if macro conditions improve. And timing the market competes with time in the market. In many cases it was better to stay invested in the early stages of an equity drawdown and manage risks on the way down. With more equity drawdown risk we look for ‘safe assets’ to diversify portfolios better and option overlays to reduce portfolio risk in the coming months.

Goldman is so long commodities that any recession will cause serious dyspepsia. Nuff said.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.