The few smartest gentlemen in the room worthy of the title are back today with grisly new warnings. BofA is still the grizzly:

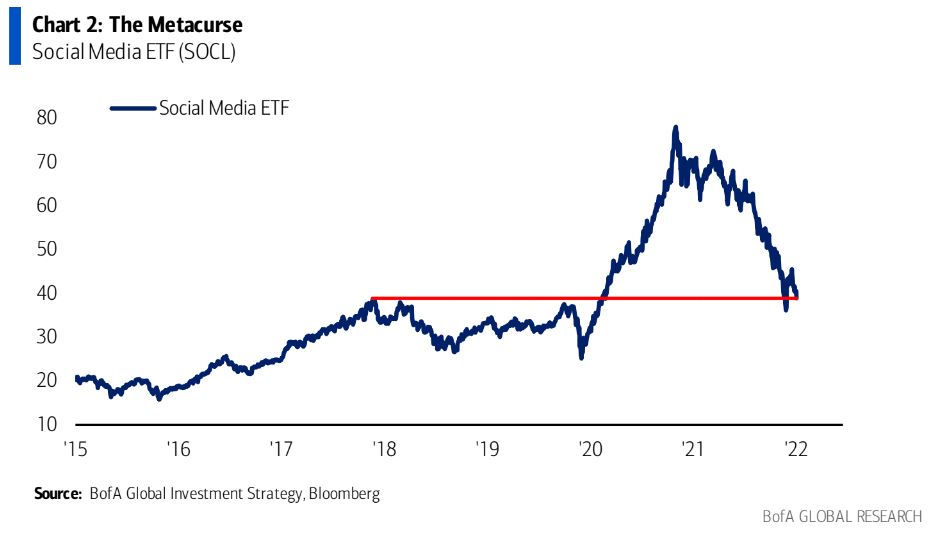

The Metacurse: world of extreme inflation,rates shock just beginning(“75bpsisthenew 25bps”), secular flip from QE-winners to QT-winners (see natural resources vs biotech–Chart3) well-underway as era of higher global rates begins(Chart4);“rates shock”=techtrauma…social media stocks back at spring 2018 levels (Chart2).

The Charge of the Hike Brigade: 75 global rate hikes YTD–highest net % centralbanks hiking since 2008 (Chart5)…era of higher volatility has begun; but Charge of Hike Brigade follows >1000 cuts since Lehman and $23tn of QE; asset, housing, consumer, commodity, consumer inflation of 2022 demands that coming Quantitative Tightening is draconian.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.