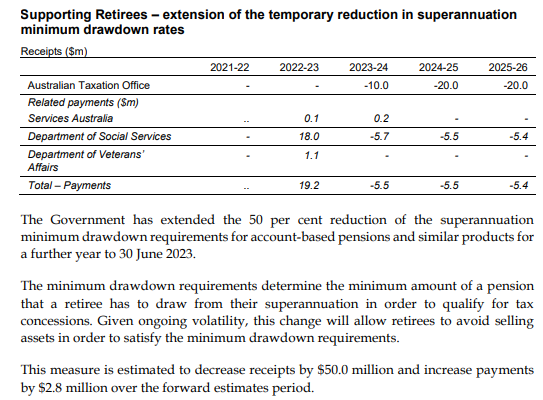

Last week’s federal budget extended by 12 months a measure introduced during the height of the pandemic allowing wealthy retirees to maintain their superannuation nest eggs without needing to sell-down their assets.

This “emergency” measure was introduced in March 2020 when the world’s stock markets were in free-fall, and reduced minimum drawdown rates by 50%.

This “emergency” measure was introduced in March 2020 when the world’s stock markets were in free-fall, and reduced minimum drawdown rates by 50%. The biggest beneficiary of this budget extension are wealthy retirees, who use generous superannuation concessions to reduce tax paid on funds they are accumulating to pass down to their children.

By contrast, it provides minimal benefits to poorer retirees that actually use money they have saved within superannuation to fund their retirement.

Before drawdown requirements were “temporarily” halved in March 2020, retirees aged between 65-74 were required to withdraw at least 5% of their account balances every year.

The policy rationale for this rule was that it limited the ability of well-off retirees to utilise superannuation as a tax dodge. Funds accumulated in super retirement accounts enjoy a zero tax rate on earnings and are untaxed when withdrawn.

Since superannuation fund returns have rocketed over past 18 months, more than reversing the temporary losses at the beginning of the pandemic, there is little policy merit in extending the temporary reduction in the minimum pension drawdown rate. Doing so is an unwanted ‘free kick’ for wealthy retirees that further entrenches super as a tax minimisation scheme.

This week, Peter Martin took similar aim at the “budget super giveaway that allows the already wealthy to amass even more tax-free”:

One of the strangest, certainly one of the hardest to justify, measures in last week’s budget was called “supporting retirees”.

A better title would have been “supercharging the wealth of those retirees who already have more than enough to live on”.

It flies in the face of the findings of the government’s own retirement income review and legislation it introduced partly in response earlier this year.

It happens not to support the living standards of retirees at all. It will enable some to spend less on themselves than they would have, while enabling those with serious wealth to accelerate the accumulation of even more, tax-free…

It’s at odds with the purpose of super, defined by the government as to provide “income in retirement”…

It is as if the government has junked the idea that super should actually be used to provide income to the people who accumulate it.

What all of this proves, yet again, is that superannuation is really a tax avoidance and inheritance scheme for the rich rather than a genuine retirement system.

Superannuation fails on almost every policy mark, namely:

- It is poorly targeted away from those in genuine need.

- It costs the budget far more than it saves in aged pension costs.

- It reduces workers’ take home pay.

- It entrenches inequality by encouraging tax avoidance and wealth accumulation by the rich.

Australians would be far better-off if we unwound the compulsory superannuation system and ploughed the billions in budget savings into a more generous universal aged pension – Australia’s true retirement pillar.