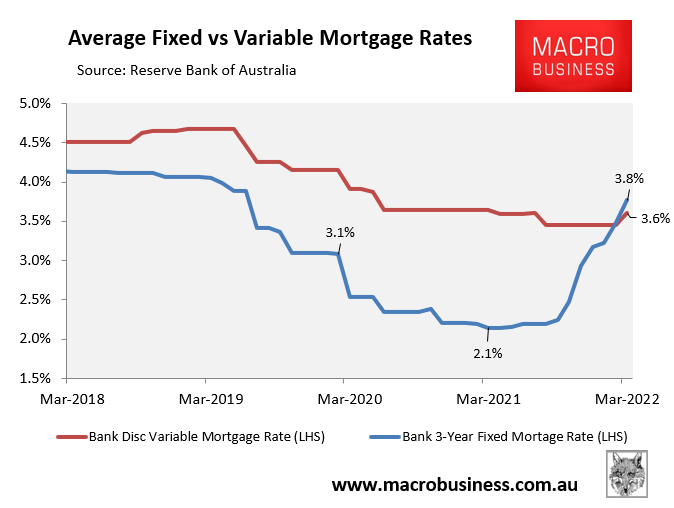

The Reserve Bank of Australia (RBA) has updated its indicator lending rates for March, which shows mortgage rates across Australia rising:

Fixed and variable mortgage rates rose in March.

As shown in the above chart, the average discount variable mortgage rate finally rose by 0.15% from its pandemic low to 3.6% in March.

The 3-year fixed mortgage rate also rose another 0.3% in March to 3.8%, and is now 1.7% above its March 2021 low.

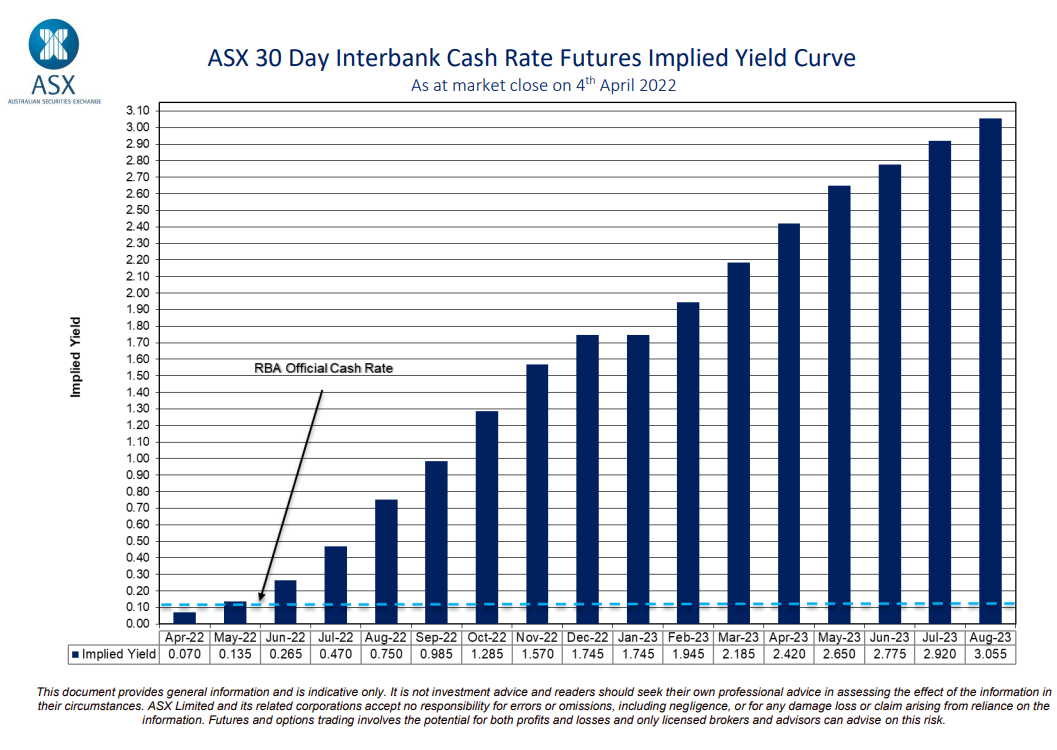

The latest futures market forecast has the RBA hiking the Official Cash Rate (OCR) to around 3% by August 2023:

3.0% interest rates by August 2023?

A 2.9% increase in the OCR by August 2023 would be the equivalent of twelve interest hikes in only sixteen months!

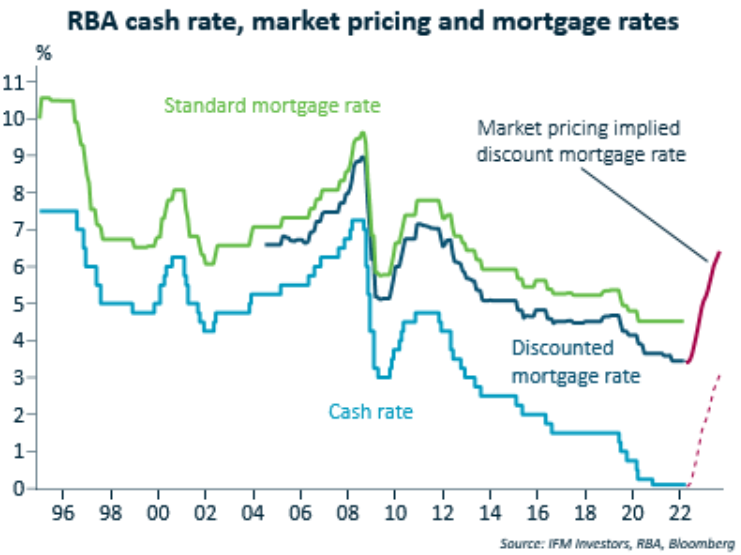

Assuming these rate hikes were passed onto mortgage holders in full, then the average discount variable mortgage rate would surge from 3.6% currently to 6.5%:

Mortgage rates to 6.5% in only sixteen months?

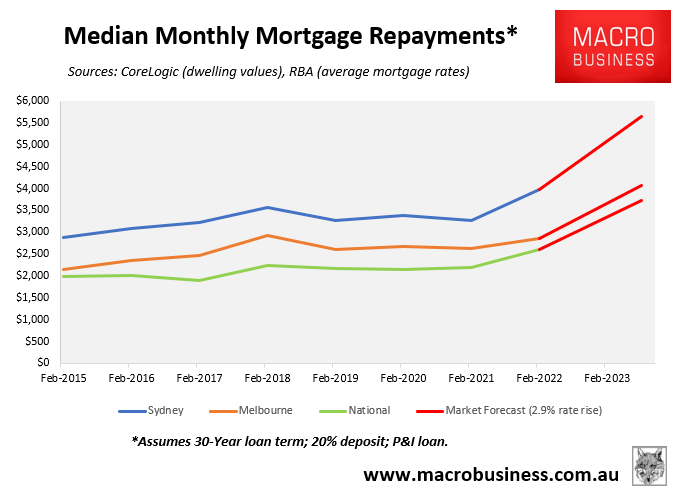

In turn, average mortgage repayments would lift by 39% from their current level.

This would see monthly mortgage repayments on the median priced Australian home rise from $2,688 in March 2022 to $3,737 – an increase of $1,049:

Median monthly mortgage repayments to rise by $1050.

For the median Sydney buyer, median monthly repayments would rise by a whopping $1,585, whereas they would rise by $1.143 in Melbourne.

Obviously, such a sharp increase in mortgage rates would devastate household finances, hammering both the housing market and broader economy.

Thankfully, the lever is in the hands of the RBA, not the markets. And I see little reason why the RBA would lift rates so aggressively, thereby engineering an unnecessary house price crash and recession.

For these very reasons, the RBA is unlikely raise rates as swiftly nor far as the market is predicting.