Soaring CPI has RBA ready to fire interest rate missile

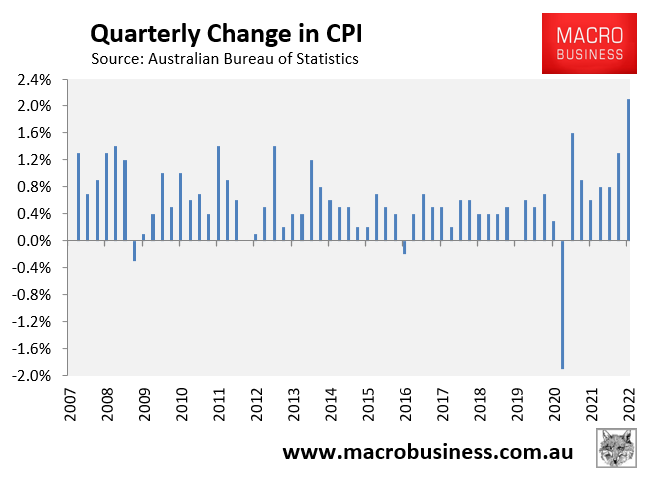

As reported earlier, Australia’s Consumer Price Index (CPI) came in white hot at 2.1% in the March quarter – smashing market expectations of a 1.7% rise:

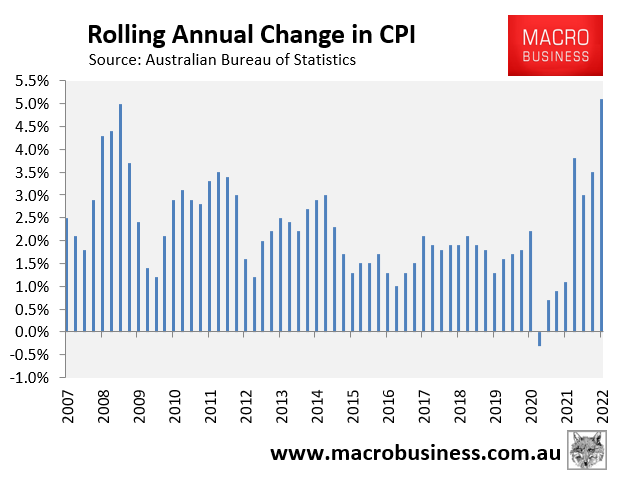

Annual CPI soared by 5.1%, beating expectations of a 4.6% rise:

It was the largest quarterly and annual rise in CPI since the GST was introduced in 2000.

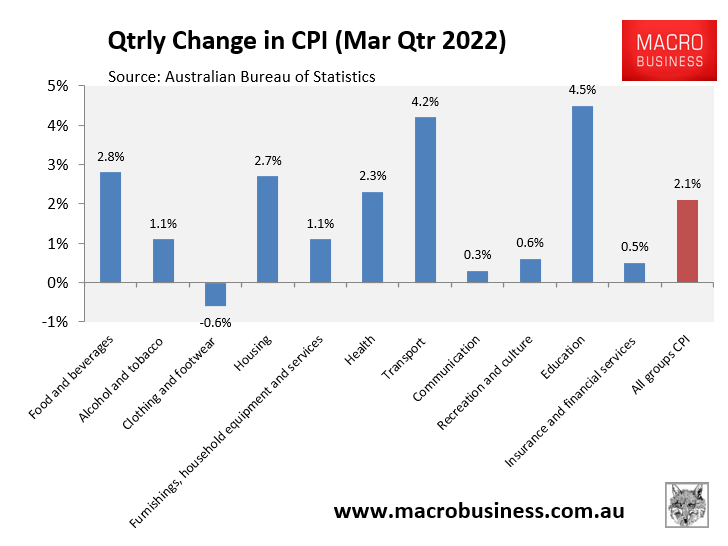

Looking at the major components, you can see that the rise in quarterly inflation was driven by Education, Transport (petrol prices), Food & Beverages and Housing (new dwellings and rents):

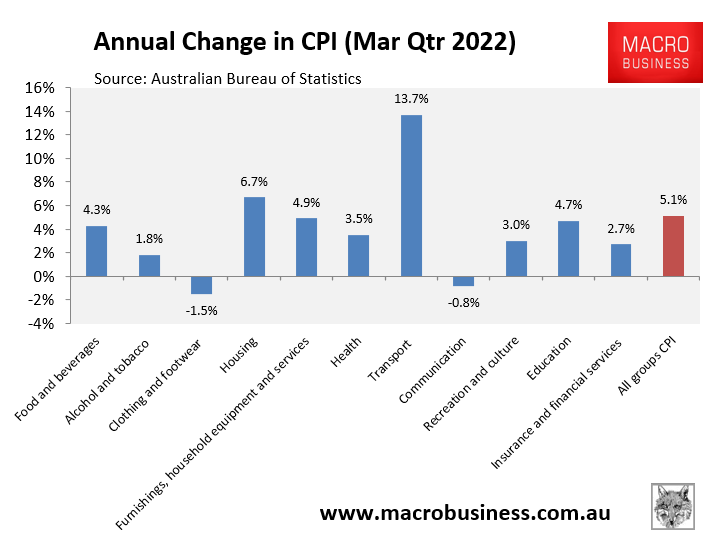

Over the year, Transport (petrol prices) also drove the inflation, with Housing, Furnishings and Health also posting strong rises:

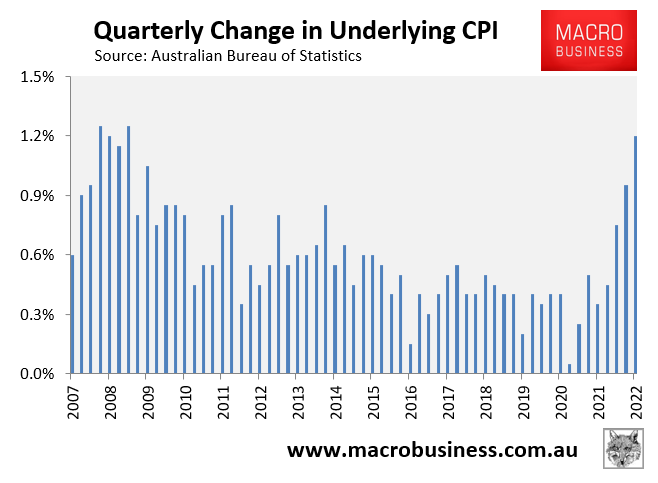

The most important part of this release is actually the ABS’ ‘analytical series’, which provides alternative measures of underlying inflation in the economy. These measures – namely the trimmed mean and weighted median – aim not to measure the size of inflation (which is captured by the headline figure), but the breadth of price inflation across the basket of consumer goods and services.

The purpose of these underlying measures is to exclude unusually large price movements (in both directions) of just a few of the subgroups, which may have quite an impact on the headline CPI. By excluding these outliers, you can get a feel for how widespread across the consumer basket inflation really is.

It is this underlying inflation that the RBA watches most closely in setting interest rates.

According to the ABS, the trimmed mean and weighted median measures came in below the headline result at 1.4% and 1.0% respectively over the March quarter – the highest level since September 2008:

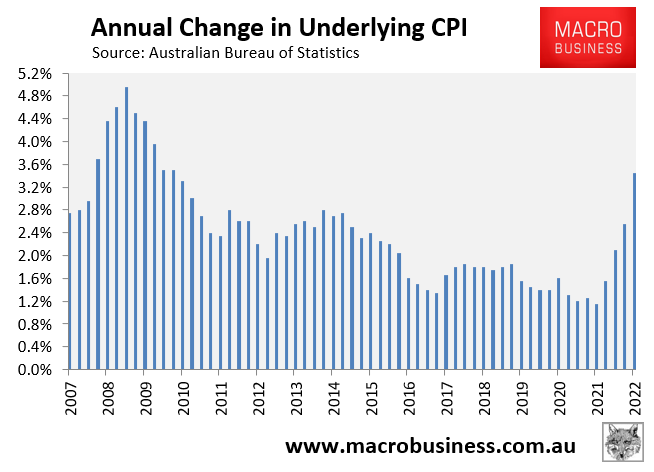

Over the year, the trimmed mean and weighted median rose by 3.7% and 3.2% respectively – the highest level since 2009:

The only thing stopping the RBA from lifting the official cash rate (OCR) is Australian wages, which grew by only 2.3% in 2021.

The March quarter wage price index will be released on 18 May, and if it comes in solid, the RBA will likely lift the OCR at the June meeting (probably by 0.40%).

The days of record low interest rates are numbered.