RBA wraps finger around interest rate trigger

By Gareth Aird, head of Australian economics at CBA:

Key Points:

- We expect the headline CPI to increase by 1.4% in Q1 22 (4.3%/yr).

- The trimmed mean CPI on our forecasts will rise by 1.2% (3.4%/yr).

- We expect the RBA to shift to an explicit hiking bias at the May Board meeting on an underlying inflation outcome broadly in line with our forecast (or stronger).

- The May Board meeting should be considered‘live’ based on our forecast for the Q1 22 CPI, but we continue to see June as the most likely month for the RBA to commence their tightening cycle.

Overview

Our call published on 15 February that the RBA would commence normalising the cash rate at the June Board meeting was founded on two things:

(i) that the Q1 22 CPI would be a lot stronger than the RBA’s implied profile and therefore they would shift to an explicit hiking bias at the May Board meeting; and

(ii) data related to wages, particularly but not limited to the Q1 22 wage price index, would be sufficiently robust for the RBA to conclude that inflation was “sustainably within the target range” and therefore they would lift the cash rate at the June Board meeting.

The central scenario we proposed for lift off in June became the consensus call across the sell side of economists last week following the April Board meeting. RBA Governor noted in his post meeting Statement accompanying the April Board meeting that, “over coming months, important additional evidence will be available to the Board on both inflation and the evolution of labour costs. The Board will assess this and other incoming information as its sets policy to support full employment in Australia and inflation outcomes consistent with the target.”

The Q1 22 CPI is therefore widely expected to lay the foundations for a June rate hike.

A brief recap of the Q4 21 inflation data.

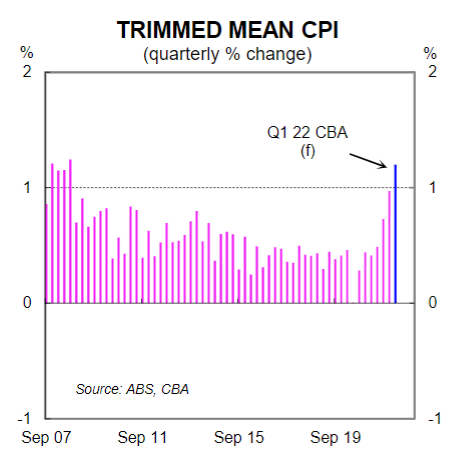

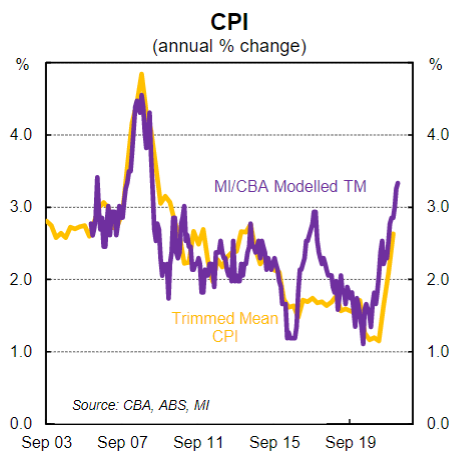

The trimmed mean, the RBA’s preferred measure of inflation, rose by 1.0%/qtr over Q4 21. It was the strongest quarterly increase since 2008. And there was evidence of broad based inflation.

The Q4 21 trimmed mean was much stronger than the RBA’s forecast (~0.6%/qtr) and significantly higher than the consensus forecast (0.7%/qtr). For the record, CBA was the outlier on the Q4 21 trimmed mean forecast with the highest prediction amongst the forecasters at 0.9%/qtr. As we remarked at the time,the inflation data validated the case we had made consistently over 2021 that the extraordinary fiscal expansion indirectly financed by money printing (i.e. quantitative easing) would generate a material lift in inflation.

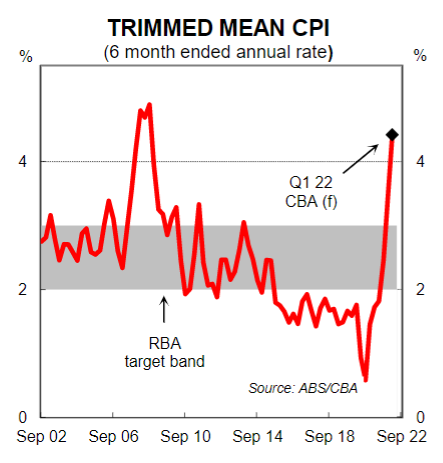

The annual rate of underlying inflation accelerated to 2.6%in Q4 21 (just above the mid-point of the RBA’s target band). The six month annualised rate of underlying inflation, which better captures the inflationary pulse, surged to 3.5%.The headline Q4 21 CPI was also very strong. It rose by 1.3% over the quarter following a 0.8% increase in Q3 21. The headline rate of inflation accelerated to 3.5%.

What to expect in the Q1 22 CPI

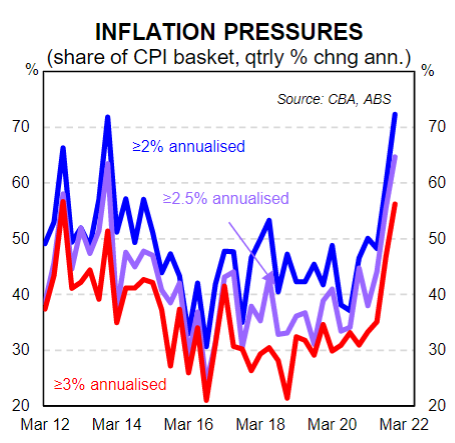

We expect there to once again be evidence of both demand pull and cost push inflation in the upcoming CPI. Input costs have risen in part due to supply side bottlenecks, while strong demand will have enabled firms to lift their prices at the consumer level.

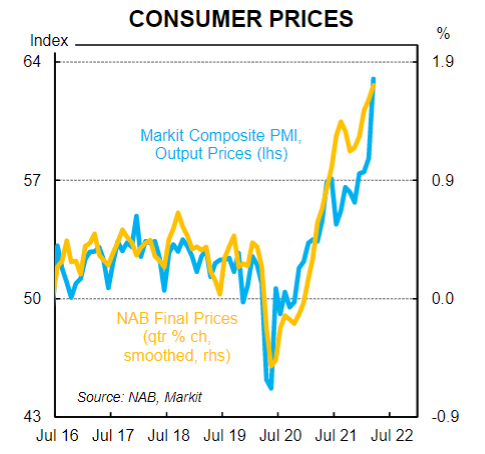

Private surveys like the NAB business survey and the Markit PMIs support our view that the rate of inflation accelerated over Q1 22 (see charts below). A lift in the inflationary pulse would also be consistent with discussions with our clients, particularly our corporates. In our view something would be amiss if we did not see inflation accelerate in the official data over the March quarter.

Our forecast is for the headline CPI to increase by 1.4% in Q1 22 which would see the annual rate lift sharply to 4.3%.

The more policy relevant trimmed mean CPI on our figuring will rise by 1.2%/qtr. This would see the annual rate surge to 3.4% (underlying inflation in line with our forecast means that core inflation will have spent just two quarters within the RBA’s 2-3% target range before blasting through it). The six month annualised rate, which better captures the inflationary pulse, is forecast to be a very strong 4.5%.

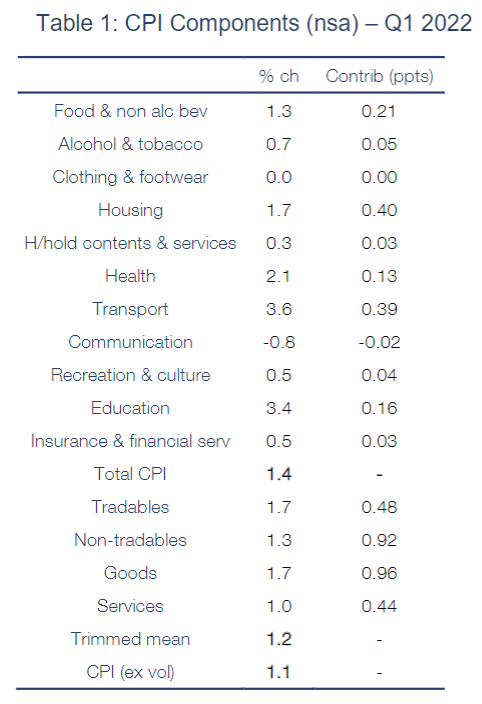

The detail

See Table 1 below for our detailed forecasts for the Q1 22 CPI basket.The main features of our call are as follows:

- a decent rise in food prices of 1.3% following a more modest 0.7% lift in Q4 21;

- a solid 3.6% increase in transport primarily driven by a 9.6% increase in petrol prices;

- a flat outcome for clothing prices as compared with the usual seasonal fall;

- the regular March quarter seasonal strength in health prices (2.1%) and education prices (3.4%);

- a solid 1.7% increase in housing as the impact of the HomeBuilder grant fades which has put substantial upward pressure on the measured price of building a home; and

- a seasonally strong 0.5% lift in recreation and culture prices (note that the usual drag on prices from lower international travel prices will not be apparent due to the annual reweight last year).

Inflation and the RBA

The RBA has forecast the trimmed mean to be 3¼%/yr at Q1 22 which implies a quarterly growth rate of ~0.8% over the March quarter. As such, if the trimmed mean CPI prints in line with our call it would be a big upside surprise relative to their forecast. Such an outcome lies at the heart of our view that they will move to an explicit hiking guidance at the May Board meeting(a print of 1.0%/qtr or above will be consistent with a shift to an explicit hiking bias). A number less than that would leave us with less conviction that the RBA will move to an explicit hiking bias at the May Board meeting.

The RBA will need to produce updated inflation forecasts in the May Statement of Monetary Policy. If we are correct on our inflation forecast the RBA will need to make a further upward revision to their inflation profile (underlying inflation forecasts over H2 22 will likely be upwardly revised to 3¾%).

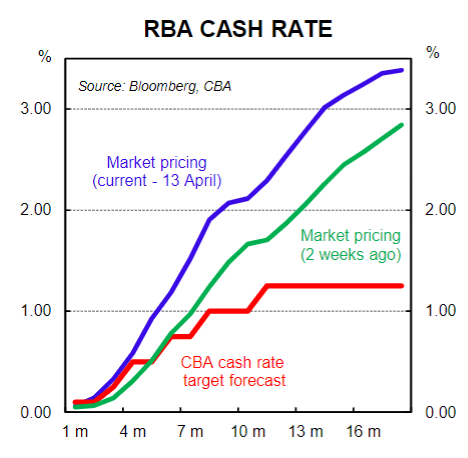

Ultimately we expect the Q1 22 CPI to be the last piece of inflation data the RBA sees before it commences normalising the cash rate.The Q1 22 wage price index (18 May) and the Q1 22 national accounts (1 June)should seal the deal for June lift off.Our base case is that the first hike in the cash is 15bps which would take the cash rate to 0.25%. We then expect a 25bp follow up rate hike in July.

Our central scenario sees the cash rate at 1.0% by end-2022. We expect the cash rate to be 1.25% by early 2023 and then on hold over 2023 (we estimate a cash rate of 1.25% to be neutral). At this stage we do not anticipate that the RBA will need to take monetary policy to a contractionary setting, though the very strong inflationary backdrop and incredibly tight labour market means the risks are skewed towards some further modest tightening in 2023.

The RBA has the capacity to put the brakes on the economy very quickly given the sensitivity of the Australian household sector to rate hikes and the direct transmission mechanism between the cash rate and the standard variable mortgage rate. The objective will be to normalise policy while keeping economic outcomes strong. We believe that successfully achieving both outcomes simultaneously will require a shallow tightening cycle.