The federal government’s Home Guarantee Scheme, which allows first home buyers (FHBs) to purchase a property with only a 5% deposit, was more than doubled to 50,000 places in the Federal Budget and last week had its price limits increased to between $900,000 in Sydney and $450,000 in regional Tasmania.

Economist Jason Murphy is the latest to warn that the Home Guarantee Scheme is a “poison pill” that could leave many FHBs drowning in negative equity when house prices inevitably fall:

Why could this be a poison pill?

The answer is that the government is herding people into the housing market just before it is forecast to fall…

Who goes under water first?

– Newest buyers

– People with the smallest deposits

i.e. exactly the people who are buying under the Home Guarantee scheme. This is the danger.

If you had a 5 per cent deposit and borrowed 95 per cent of the value of your house, what happens if your house immediately goes down in value by 6 per cent? You owe the bank more than the house is worth. House prices are forecast to fall more than that though…

In the worst case scenario, thousands of punters are lured into the expensive part of the housing market just in time to go under water. They can borrow huge sums – up to $855,000 in Sydney – just as interest rates are forecast to go up and house prices are forecast to go down.

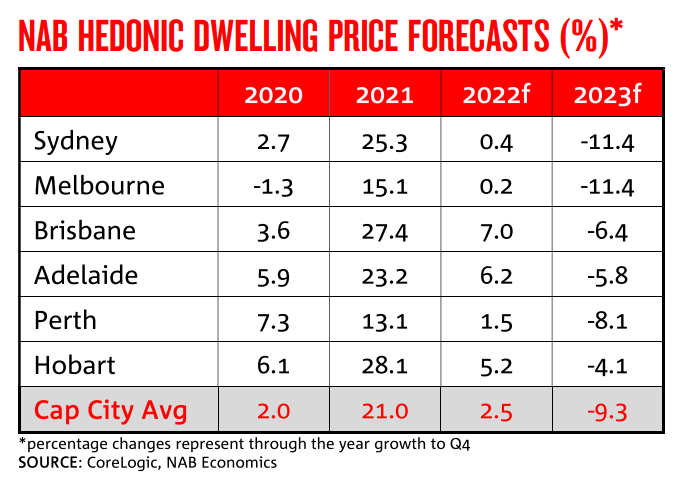

Jason Murphy is spot on. NAB’s latest house price forecasts, released last week, tip that dwelling values across the combined capitals will fall by 9.3% in 2023, led by steep declines across both Sydney and Melbourne (both -11.4%):

NAB also forecasts that the RBA will hike the cash rate to 2.25% by the end of 2024, which would mean that FHBs would experience a massive 30% rise in average mortgage repayments, assuming increases in the cash rate are passed on to mortgage holders.

Using the Sydney example cited by Jason Murphy above, monthly mortgage repayments on an $855,000 priced Sydney home would rise by $1,100 if NAB’s interest rate forecast came to fruition.

In this scenario, many FHBs would face a crushing increase in mortgage repayments, alongside deep negative equity as house prices fall.

Offering government-backed mortgages to FHBs with 5% deposits is a bad idea at the best of times. It is much worse when interest rates are about to rise sharply and home prices are about to fall.