The Reserve Bank of Australia (RBA) has released its household and mortgage debt statistics for the December quarter of 2021.

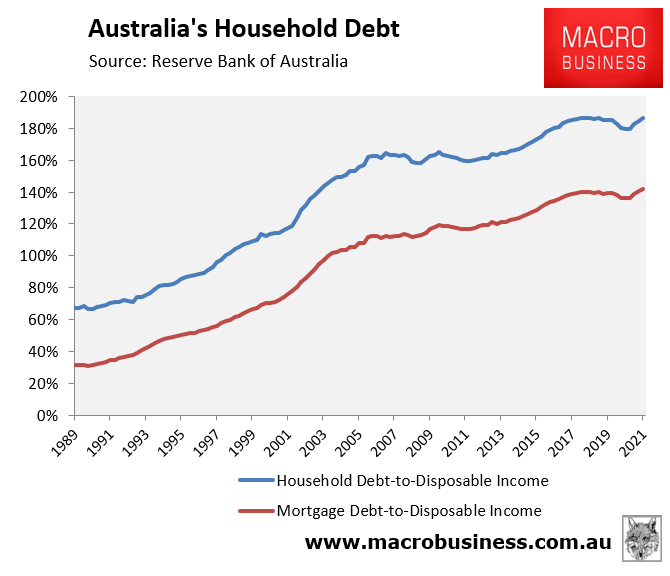

As shown in the next chart, the ratio of aggregate household debt to disposable income rose to a near record high 186%, whereas aggregate mortgage debt rose to a record high 141.8% of household disposable income:

Household debt loads rising.

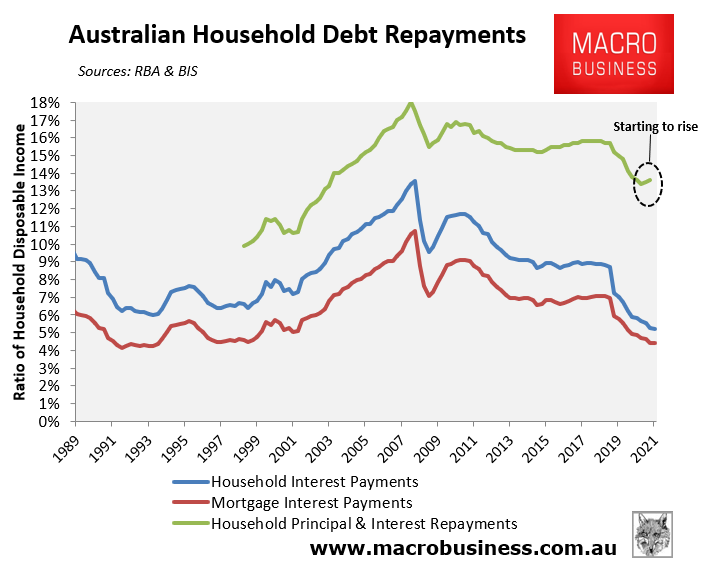

Due to cratering interest rates, the ratio of mortgage interest payments to household disposable income fell to a 28 year low of just 4.4%, which was less than half the 2008 peak of 10.8% (see red line below). Thus, the fall in interest rates has more than offset the rise in household debt.

Interest repayments fall, but principal repayments rise.

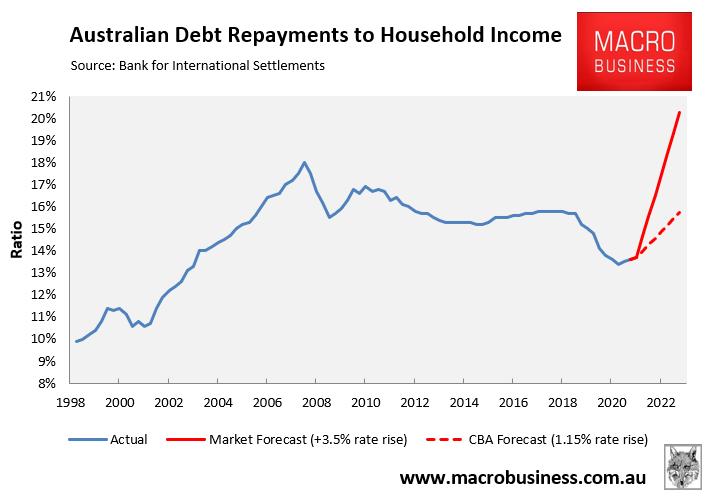

However, separate data from the Bank for International Settlements, measuring both principal and interest repayments as a ratio of disposable income (green line above), shows that overall debt repayments are beginning to rise. This is because the rapid appreciation of dwelling values has increased the principal share of debt repayments, more than offsetting the reduction in the interest component of debt repayments.

The above data is also likely to represent the low water mark for mortgage repayments, which are about to rise sharply.

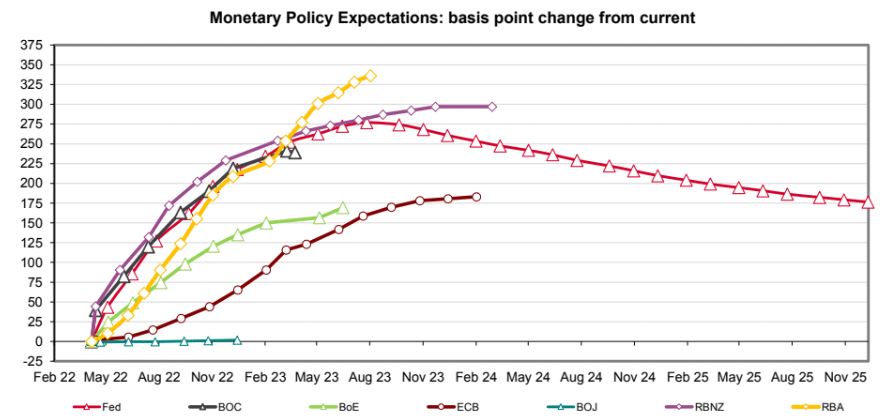

Australia’s four largest banks are tipping the RBA will hike the official cash rate (OCR) at least four times in the six months from June. CBA tips the OCR will peak at 1.25%, whereas Westpac (2.0%) and NAB (2.25%) have forecast a higher peak.

The market is even more bullish tipping nearly a 3.5% rise in the OCR by August 2023 – equivalent to fourteen 0.25% rate hikes in only sixteen month’s time:

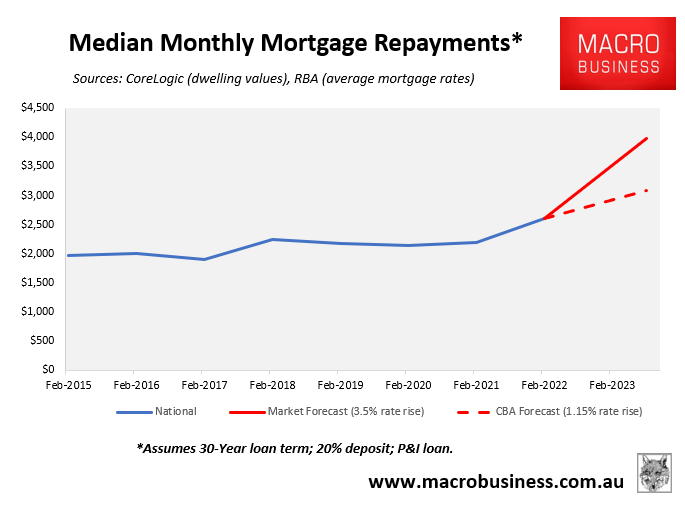

If the CBA is correct and the RBA only hikes the OCR to 1.25%, and this was passed on in full to mortgage holders, then this would increase average mortgage repayments by 15%, or by around $400 per month on the median priced Australian home.

But if the market is correct and the RBA hikes the OCR by around 3.5%, then the median mortgage repayment would rise by 48%, or by around $1280 per month on the median priced Australian home:

The next chart shows that under the market’s interest rate forecast, Australian principal and interest debt repayments would shoot way past the 2008 peak, whereas it would rise to the pre-COVID level under the CBA’s forecast:

For what it is worth, I am firmly in the CBA’s camp on interest rates for the simple fact that Australians are carrying so much debt that larger rate rises risks crashing the housing market and smashing the economy.

Irrespective, we are currently experiencing the calm before the mortgage storm, with repayments about to lift materially.

Subscribe to my Macro Breakdown YouTube channel @ Leithvo.