Fed’s balance sheet unwind unlikely to support steeper curves. Minutes from the March FOMC revealed details about the Fed’s balance sheet reduction plan, which were largely in line with our expectations. The maximum cap is to be$95bn/month (split between $60bn for USTs and $35bn for MBS), roughly twice the pace seen in the last cycle, and the caps could be phased in over a three month (or modestly longer) period. With active UST sales from the SOMA portfolio very unlikely, net UST coupon issuance and gross MBS issuance set to decline, and the strong likelihood that Treasury will lean heavily on bill issuance to replace lost Fed financing, the change in duration risk the public has to absorb is likely to be relatively modest. That said, over time, waning demand from other unlevered buyers could weigh on markets, resulting in steepening pressure, all else being equal.

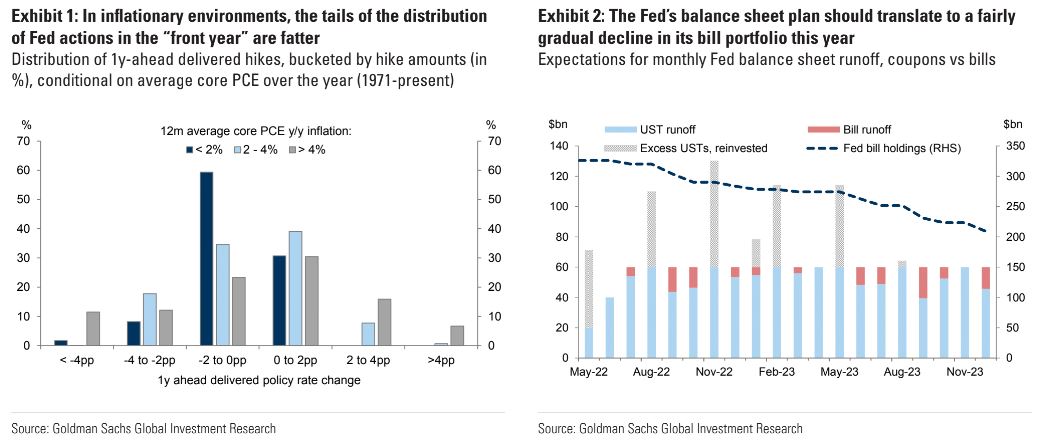

However, this will most likely be readily offset by curve flattening from a likely further front-loading of hikes—the minutes also seemed to suggest there was sizable support among officials for “one or more” 50bphikes if necessary. Given upside risks to inflation, and the Fed’s stated desire to move towards a neutral stance “expeditiously,” recent steepening not withstanding, we retain our curve flattening bias.nHistory suggests fatter tails in actual policy rate outcomes. In a recent report, we examined whether normalization in 2022 is already “fully priced,” using history from the 1970s onward as a guide. Our historical study yielded a few key observations. First, while markets appear to already be pricing the maximal amounts in the front year seen historically on a rolling basis, realized outcomes can deviate substantially in either direction. Depending on how inflation evolves, front-end shorts could still make sense—this for instance would be the case if inflation is slower to normalize than our current forecasts, which might present upside risks to our baseline policy rate forecasts for this year. Second, in high inflation environments, tail outcomes in both directions (i.e., greater than expected hikes or cuts) are more common than in a stable inflation regime (Exhibit1), and it may be prudent to protect against both. Third, while such environments appear to be associated with deeper curve inversions, long-run nominal rates nevertheless tend to drift higher through the hiking cycle, making selling calls/receivers on forwards in this part of the curve potentially attractive.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.