A bifurcation in risk taking overnight as Wall Street rallied while European markets were more sanguine, with the new reporting season helping stateside. All eyes remain on the Fed, with the 10 year US Treasury yield making another new nearly four year high above the 2.9% level. The USD rose again with Yen dominating as it is dumped wholesale around the world, while the Australian dollar remains under the pump despite the recent lift in commodity prices. Oil prices however suffered some profit taking with both markers losing nearly 5%, with Brent crude back below the $110USD per barrel while gold suffered the same fate after recently touching the $2000USD per ounce level, selling off sharply below the $1950 level instead.

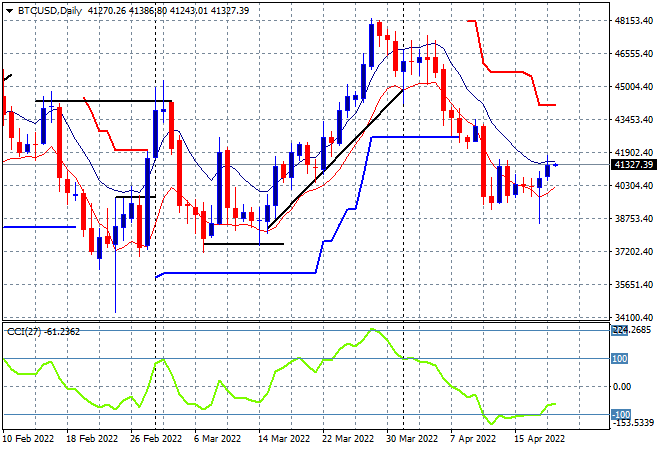

Bitcoin remains in somewhat of a depressed state, having sold off last week to be anchored around the $40K level after breaching daily ATR support at the $42K level in late March with a lot of oscillation recently seeing it pip back above the $41K level overnight. The lack of confidence in the crypto world could see a further retracement down to the February lows at the $37K level next if the daily high moving average is not breached soon:

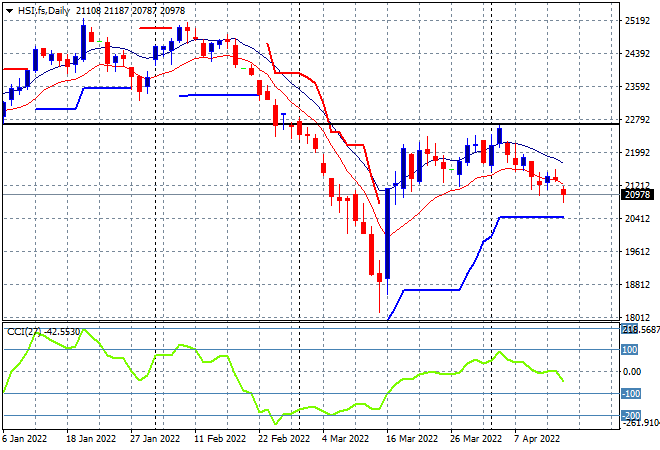

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets remain unsettled, with the Shanghai Composite scraping in with a scratch session to close at 3194 points while the Hang Seng Index has slumped again, falling more than 2% to finish at 20987 points. The daily chart remains stuck below very strong resistance at the 22600 point level with momentum pushing the market ever lower with continued moves below the low moving average likely as momentum switches from neutral to negative here:

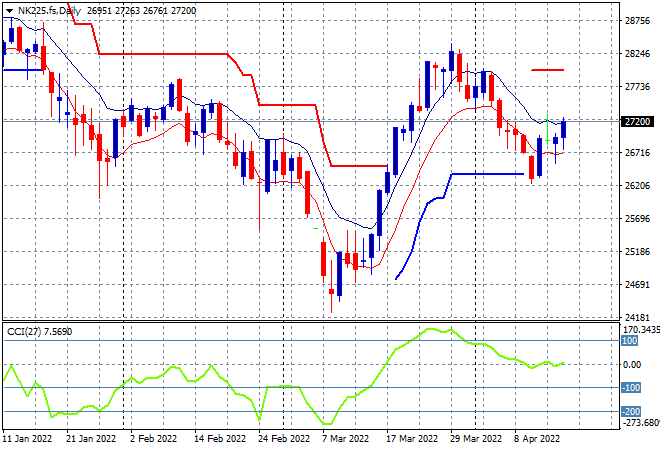

Japanese stock markets however are bouncing higher, lifted by a very weak Yen with the Nikkei 225 closing 0.6% higher at 26985 points with futures indicating a mild bounce on the open as the ever weaker Yen provides a strong buffer. Daily momentum is still at a neutral level with price not yet retreating below daily ATR support but its still rejecting weekly resistance at the 27500 point level. Watch for a potential break above the high moving average soon:

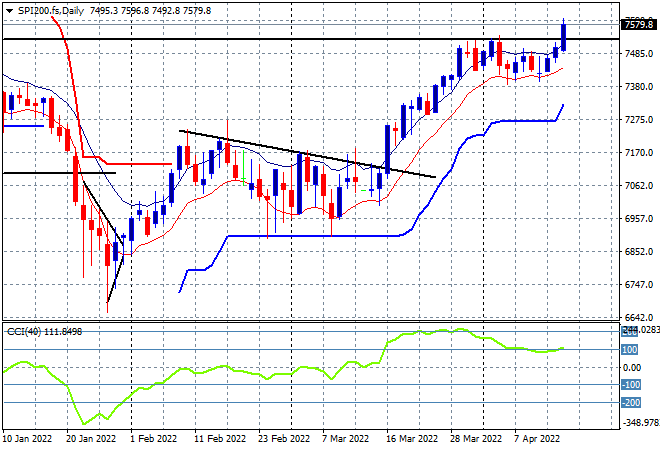

Australian stocks were able to put in a good jumpstart to the truncated trading week with the ASX200 closing 0.5% higher at 7565 points as SPI futures are up at least 50 points or another 0.6% to keep the pre-election euphoria rolling along. The daily chart continues to show a lot of potential with daily momentum still quite strong with price now seeming to push aside resistance at the former highs from December last year – watch for a good close today to clarify a new uptrend:

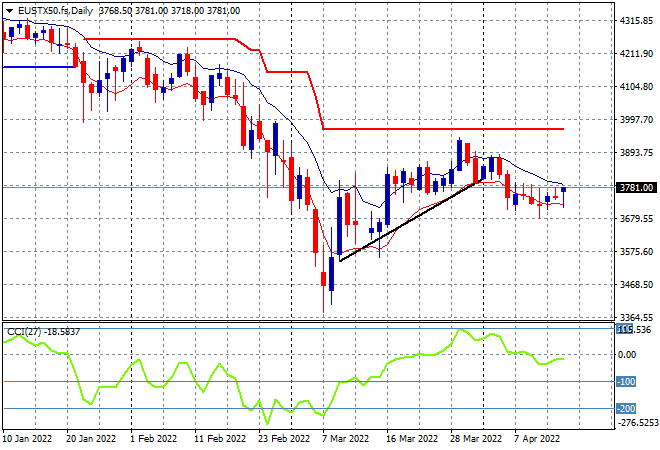

European shares continue to go nearly nowhere, despite a late charge on Wall Street with the Eurostoxx 50 index finishing 0.5% lower, taking back the previous gains to close at 3830 points, with French stocks the main culprit for the falls. Support has held around the 3700 point area but trading sessions are so tight and muted – even with the Easter break – I would contend there is some big volatility brewing soon, so watch for a potential breakout or breakdown at the obvious levels of support and resistance:

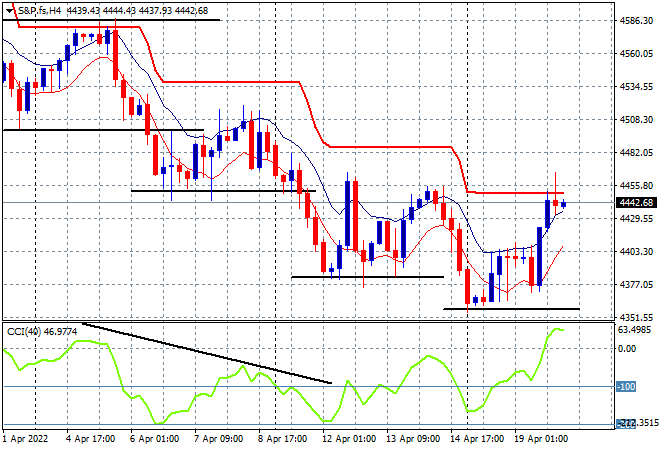

Wall Street remains volatile and proved so again, this time properly breaking out as the NASDAQ jumped more than 2% while the S&P500 lifted 1.5% to close above the 4400 point level at 4462 points. Price action on the four hourly chart is continuing to show a series of steps down as the BTFD crowd try to step in and shore up support and short term price action is not yet indicative that the buying is enough with ATR resistance overhead still not cleared and four hourly momentum not yet overbought:

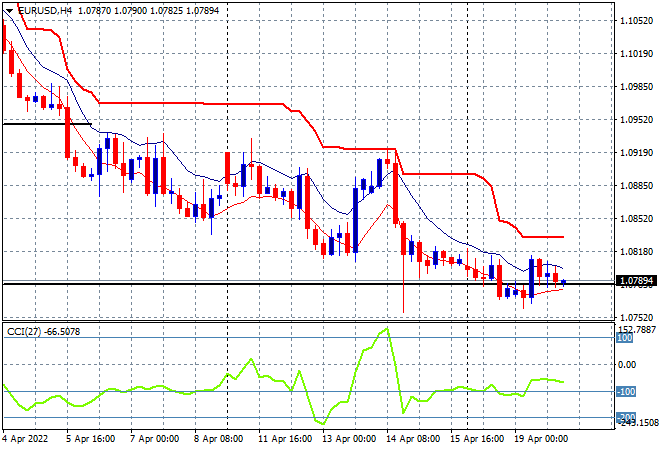

Currency markets continue to see a stronger USD with Euro rolling back below the 1.08 level after a failed oscillation to get back above a price of control since the start of the week. This keeps price action in line with its longer term downtrend, as short term momentum remains oversold and trailing ATR resistance continues to ratchet down – parity may well be on the radar:

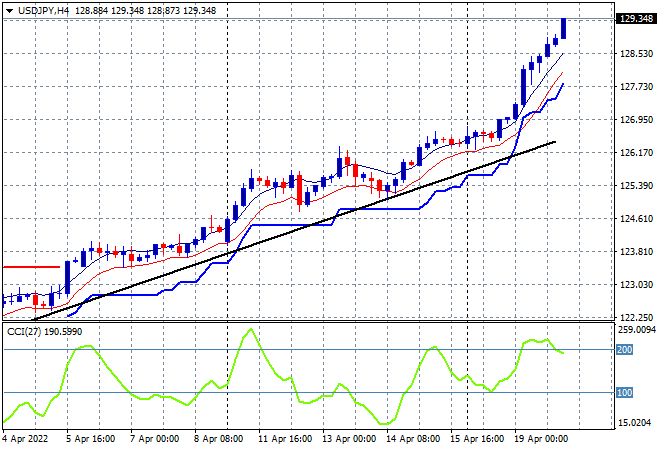

The USDJPY pair is literally on one of the biggest rolls ever, going back more than 40 years with a huge surge again overnight to get through the 129 level, now up over 300 pips since the start of the week! This keeps price action at new decade highs with no stopping apart from the occasional pause as Yen is dumped everywhere. Watch for momentum to potentially revert here from extremely overbought levels, but that trendline looks solid:

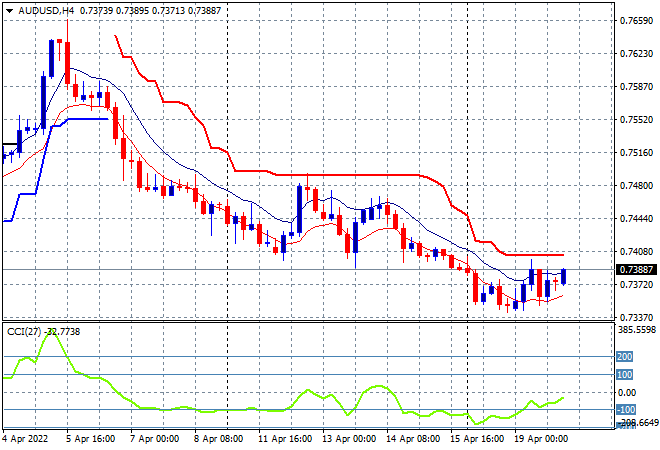

The Australian dollar continues to lose its way with a tight trading session that sees its remain below the 74 handle after the release of the latest RBA minutes yesterday. Price has broken below weekly support which does not bode well for any medium term uptrend potential if the RBA raises rates before the election (unlikely), but short term momentum is suggesting a possible swing play is building, so watch overhead ATR trailing resistance for a breakout:

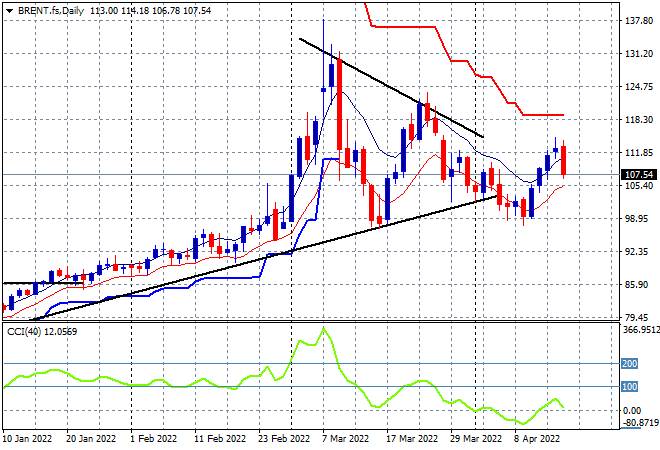

Oil markets sold off sharply later in the session overnight with Brent pulling back below the $110USD per barrel level, finishing around 5% lower at the $107 level. Again, daily momentum is not yet providing enough of an indicator to suggest this blip higher has potential, with a drawback to the key $100 level possible given this bearish candle:

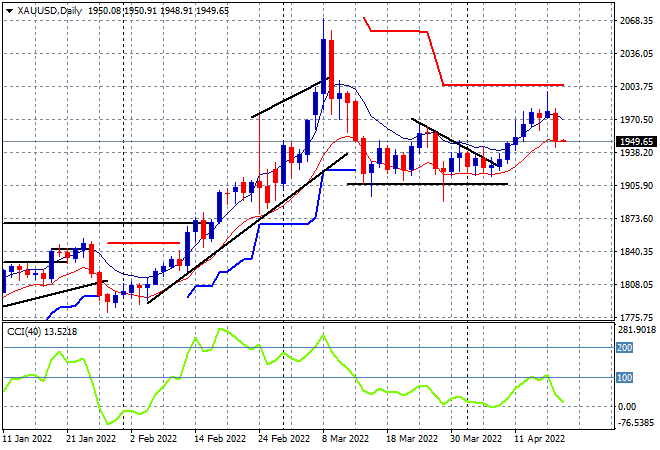

Gold failed to make good on its recent stretch to climb back above the $2000USD per ounce level overnight, instead retracing to the $1950 level instead as profit taking continued. Price action was looking good here for more upside potential having successfully defended the psychologically important $1900USD per ounce level, but as I warned yesterday, daily momentum was not yet overbought. The low moving average must be defended here or we could see a swift return to $1900:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!wrong on your position, so cry uncle and get out!