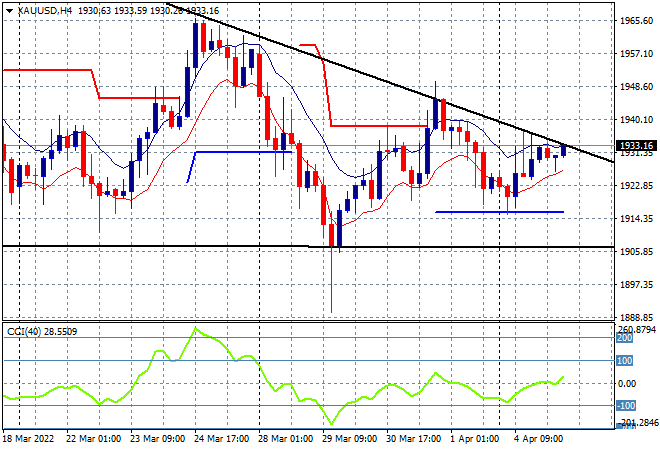

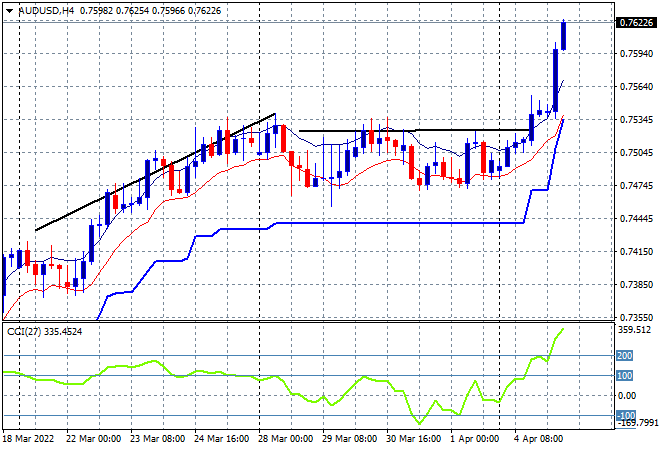

Asian stock markets were relatively quite today, given the holidays in China, with sentiment still somewhat mixed for macro and domestic reasons, as the RBA meeting lead to yet another hold but a substantive change in language with “patience” on rate rises thrown out the window. This sent the Australian dollar soaring while the USD remains strong against the other major currency pairs. Oil prices are jumping higher again on expectations on more sanctions, following more Russian war crimes in Ukraine, with gold trying to breakfree again, almost meeting its previous weekly high and ready to break above its weekly downtrend line at the $1940USD per ounce level:

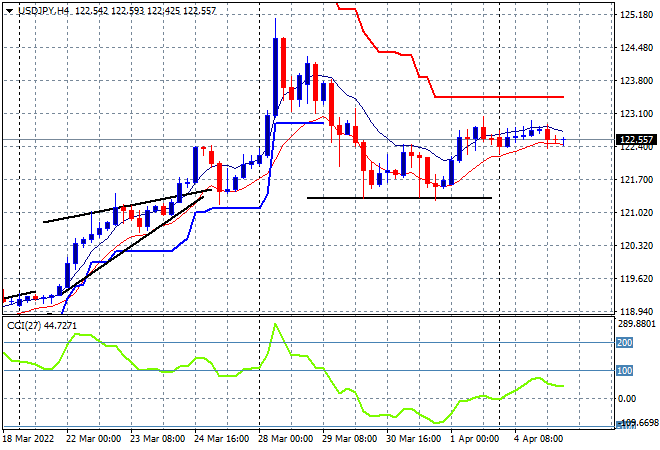

Mainland Chinese share markets remain closed for a holiday with Japanese stock markets ticking over without much of a result. The Nikkei 225 lifted just 0.2% to 27787 points while the USDJPY pair is maintaining its Friday night close position, drifting lower to be below the 123 handle:

Australian stocks had a similar result, unexpectedly not following through on the positive lead from Wall Street lead overnight with the ASX200 closing 0.2% higher to remain above the 7500 point level. It was mainly due to the RBA meeting and the big surge in the Australian dollar which had already broken out beforehand, but jumped right through the 76 handle as it tosses aside monthly resistance on expectation of faster rate rises:

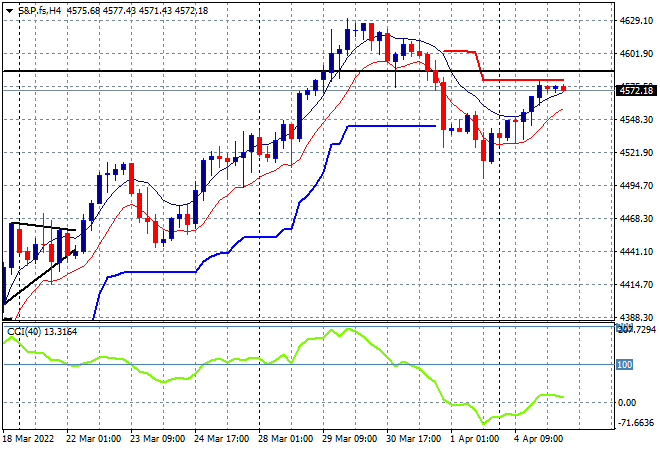

Eurostoxx and Wall Street futures are again drifting sideways as we head into the London session, with the S&P500 four hourly chart showing price wanting to break above trailing ATR resistance and the psychological 4600 point level but lacking proper momentum so far:

The economic calendar is US centric tonight with the latest balance of trade figures and then more importantly, the US ISM non-manufacturing PMI print.